Wealthy family meeting with estate planning advisors in a modern office

Advanced Estate Planning Strategies for High Net Worth Families

Content

Content

Wealthy families watch millions evaporate through poor planning decisions. Estate taxes, creditor claims, and family disputes drain fortunes that took decades to build. The difference? Families who implement strategic wealth transfer techniques before problems arise versus those who scramble to react after it's too late.

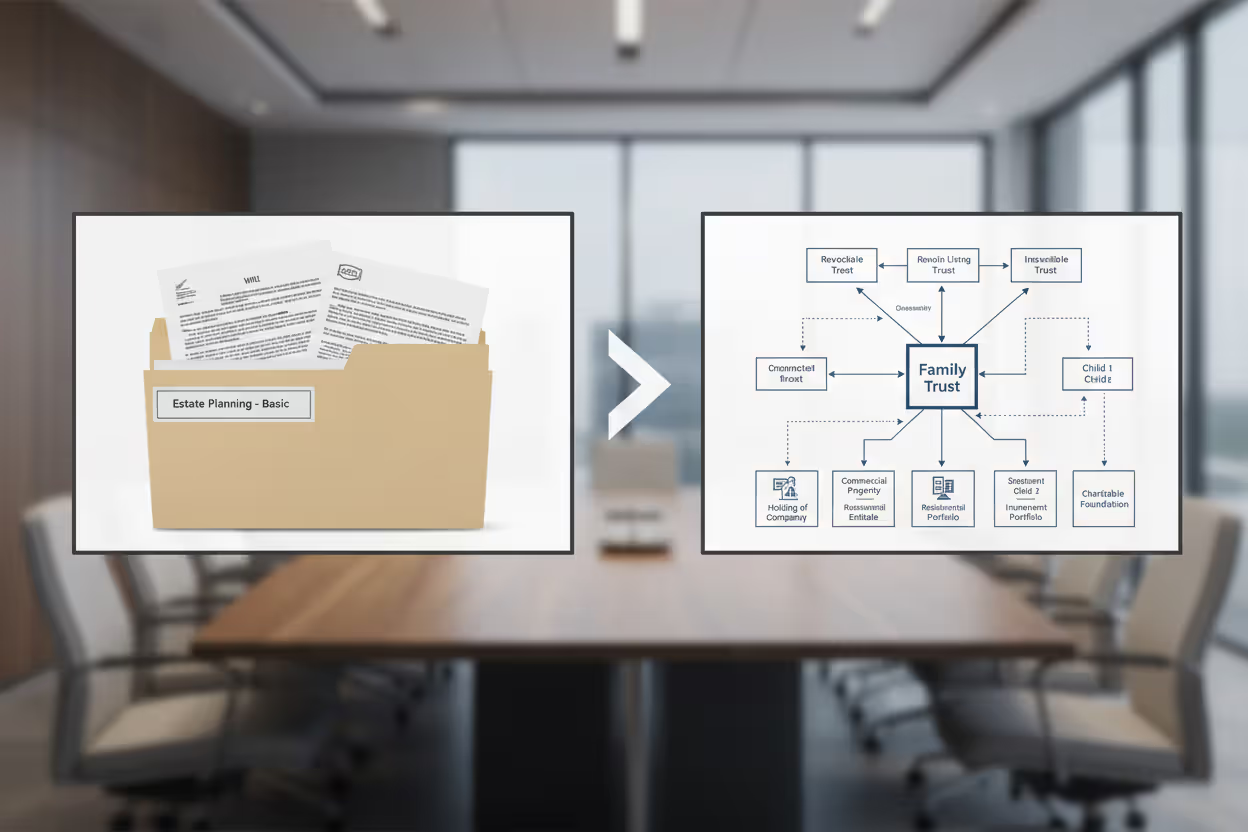

Basic documents—a will, simple trust, power of attorney—work fine for most people. But once your situation crosses certain thresholds of complexity, you need different tools entirely.

What Makes Estate Planning "Advanced"

Let's be direct: you probably need sophisticated strategies if any of these apply to your situation.

First scenario: your estate value approaches or exceeds current exemption limits. For 2026, federal exemptions sit at $13.99 million per person. Married? You're looking at roughly $28 million combined. Cross that line and the IRS takes 40% of everything above it. But here's what catches people off guard—certain states jump in way earlier. Massachusetts starts taxing estates above $2 million. Oregon kicks in at $1 million. If you live in one of these states, "high net worth" means something very different.

Author: Jonathan Whitmore;

Source: harbormall.net

Second scenario: you own a business worth seven figures or more. Consider a third-generation printing company valued at $12 million. The founder's estate falls below federal exemption levels, so no problem, right? Wrong. The business represents 85% of the total estate value but generates minimal liquid cash. Where does the family find $2 million for state estate taxes without selling the company their grandfather built? This exact situation destroys family businesses every single year.

Third scenario: you own property across state lines. Your primary home in Connecticut, a ski condo in Colorado, rental properties in Texas, and a beach house in South Carolina. Each property gets probated separately under different state laws. Your Connecticut estate plan might conflict with Texas property law. You're looking at four separate probate proceedings, four sets of legal fees, and potential conflicts between different state regulations.

Fourth scenario: complicated family structures. You married twice. Your current spouse is 15 years younger. You have adult children from your first marriage, teenagers from your second, and a son with autism who receives Medicaid. How do you provide for your disabled child without disqualifying him from government benefits? How do you ensure your older children receive their inheritance while protecting your younger spouse who could live another 40 years?

Professional practice ownership creates its own planning nightmare. Three orthopedic surgeons, each owning a third of their practice, each worth $4 million. Dr. Johnson dies unexpectedly. His widow now owns a third of a medical practice—but she's a high school teacher with zero medical training and no interest in running an orthopedic clinic. The surviving partners can't force her to sell, and she can't practice medicine to earn her ownership share. Without a proper buy-sell agreement funded with life insurance, everyone loses.

Tax Mitigation Techniques in Sophisticated Estate Planning

Grantor Retained Annuity Trusts let you move appreciating assets to heirs while paying minimal gift tax. Here's how it works in practice: You transfer $5 million in Tesla stock into an irrevocable trust. You keep receiving payments for three years (the annuity). Whatever the stock gains above the IRS's assumed interest rate—currently 5.6%—passes to your kids tax-free.

Let's say Tesla jumps 60% during those three years. Your original $5 million becomes $8 million. You got back your $5 million through annuity payments. That $3 million in growth? It belongs to your beneficiaries without touching your lifetime gift exemption. The catch: you must survive the trust term. Die during year two and everything collapses back into your taxable estate.

Qualified Personal Residence Trusts work similarly but specifically for homes. You transfer your $4 million beach house into an irrevocable trust, retain the right to live there for 10 years, then ownership passes to your children. The gift tax value gets calculated based on the remainder interest after your 10-year term—maybe $2.3 million instead of the full $4 million. After 10 years? You can keep living there by paying your kids fair market rent, which further reduces your taxable estate while transferring more wealth to them.

Author: Jonathan Whitmore;

Source: harbormall.net

An Irrevocable Life Insurance Trust removes life insurance proceeds from estate tax calculation. Without this trust structure, that $5 million policy death benefit gets added to your estate—potentially triggering $2 million in estate taxes. Properly structured? The trust owns the policy, receives the death benefit, pays zero estate tax, and distributes proceeds according to your wishes. You make annual gifts to the trust covering premium payments, using Crummey withdrawal rights to keep gifts under the annual exclusion ($18,000 per beneficiary in 2026).

Family Limited Partnerships and LLCs create legitimate valuation discounts on transferred assets. Example: You place $10 million in commercial real estate into an FLP. You keep a 5% general partnership interest giving you management control. You gift 20% limited partnership interests to each of your three children over several years.

Here's where it gets interesting. Those limited partnership interests can't vote on partnership decisions. Limited partners can't easily sell their interests to outsiders. An independent appraiser values a 20% limited interest at perhaps $1.3 million instead of $2 million—a 35% combined discount for lack of control and lack of marketability. You just transferred $6 million in actual value while only using $3.9 million of your gift exemption.

The IRS watches FLP arrangements closely now. You need legitimate business purposes beyond tax avoidance. You need to respect formalities—regular meetings, proper documentation, legitimate business activity. Sloppy FLP administration gets challenged and loses.

Charitable Remainder Trusts solve a specific problem beautifully. You bought Amazon stock in 2010 for $50,000. It's now worth $2 million. You want income but selling triggers $488,000 in capital gains tax (20% federal plus 3.8% net investment income tax).

Transfer that stock to a Charitable Remainder Trust instead. The trust sells the stock, pays zero capital gains tax, invests the full $2 million, and pays you 6% annually ($120,000) for life. You get an immediate income tax deduction for the present value of the remainder interest going to charity—maybe $600,000. Your charity receives whatever remains after you die. You avoided capital gains tax, got an income tax deduction, secured lifetime income, and supported a cause you care about.

Generation-skipping strategies require understanding a separate tax system most people don't know exists. The generation-skipping transfer tax (GST tax) hits transfers to grandchildren at 40%. But you get a $13.99 million GST exemption (2026) separate from your gift and estate exemption. Allocate this exemption properly to dynasty trusts, and you create multi-generational wealth that avoids estate tax at each death for centuries. Dynasty trusts established in South Dakota, Delaware, or Nevada can continue for 360 years or indefinitely. A $10 million dynasty trust growing 6% annually reaches $320 million in 60 years—all without estate tax erosion at each generation.

Author: Jonathan Whitmore;

Source: harbormall.net

Asset Protection and Creditor Shielding Strategies

Surgeons, business owners, real estate developers, and high-profile individuals share a common vulnerability: lawsuits. Basic estate planning offers zero protection from creditors. You need specialized structures implemented before claims arise.

Domestic Asset Protection Trusts represent the strongest protection available while keeping assets in the U.S. Seventeen states now permit these trusts where you can be a discretionary beneficiary of your own irrevocable trust while shielding assets from future creditors.

Real example: An orthopedic surgeon in California faces constant malpractice exposure despite insurance. He establishes a Nevada DAPT, transfers $4 million in investment accounts, and names himself as a discretionary beneficiary. The independent Nevada trustee can distribute to him when appropriate, but future malpractice creditors generally cannot reach these assets. Current creditors at the time of transfer maintain their claims—you cannot defraud existing creditors. Nevada requires four years between funding and full protection. Alaska offers immediate protection but has other trade-offs.

Author: Jonathan Whitmore;

Source: harbormall.net

Offshore trusts provide stronger protection but dramatically higher costs and complexity. Cook Islands and Nevis trusts operate under legal systems that refuse to recognize U.S. court judgments. A creditor with a U.S. judgment must start completely over, re-litigating the entire case under Cook Islands law. Few creditors pursue this, making these trusts highly effective.

But offshore structures cost $50,000-75,000 to establish and $15,000-20,000 annually to maintain. You need regular reporting to the IRS and FinCEN. The juice is worth the squeeze only with significant assets ($3+ million) and extraordinary risks.

LLC structuring protects real estate portfolios and business assets. Hold each rental property in a separate single-member LLC. A tenant slips on ice at Property A and sues. They can potentially recover the equity in Property A—but not Property B, C, or D held in separate LLCs, and not your personal residence or retirement accounts.

Multi-member LLCs add charging order protection. Your judgment creditor gets only a charging order—the right to receive distributions if and when made, but no right to force distributions or access LLC assets. Wyoming and Delaware provide the strongest charging order protection statutes. Smart asset protection uses Wyoming or Delaware LLCs even if your properties sit in other states.

Prenuptial agreements protect family wealth through marriage transitions. A family with a $30 million manufacturing business sees their son marry. Without a prenup, that daughter-in-law might claim a marital interest in the business during divorce. A properly drafted prenuptial agreement clarifies that the business remains separate property, specifies how business appreciation during marriage is treated, and can waive estate rights. This protects both the family business and creates clear expectations reducing future conflict.

Equity stripping replaces vulnerable equity with protected cash. A real estate investor owns five commercial buildings worth $8 million with no debt. A creditor eyeing these properties sees $8 million in vulnerable equity. The investor places mortgages on the properties, extracts $6 million in cash, and moves that cash to a Nevada DAPT. Now creditors find heavily mortgaged properties with minimal equity, while the cash sits protected. This technique requires careful timing and documentation to avoid fraudulent transfer claims.

Business Succession in Complex Estate Planning Strategies

Statistics tell a brutal story: 70% of family businesses fail transitioning to the second generation. 90% fail reaching the third generation. Failed succession planning, not failed businesses, causes most of these failures.

Buy-sell agreements establish exactly how business interests transfer at death, disability, retirement, or divorce. Three partners each own a third of a $12 million engineering firm. Partner A dies unexpectedly. His widow now owns a third of the business—but she's a school administrator who knows nothing about engineering and has zero interest in running a firm. Partners B and C don't want an unwilling partner, and the widow doesn't want her inheritance tied up in a business she can't access.

A properly funded buy-sell agreement solves this. Each partner carries $4 million in life insurance on the other partners. Partner A dies. The $4 million death benefit purchases his interest from his widow at the predetermined valuation. She receives $4 million in liquid cash. Partners B and C own the entire business. Everyone wins.

Author: Jonathan Whitmore;

Source: harbormall.net

Cross-purchase agreements have each owner buy insurance on the others. Entity-purchase agreements have the business itself own the policies. Hybrid agreements combine both approaches depending on tax consequences and number of owners.

Valuation formulas in buy-sell agreements prevent disputes and IRS challenges. Fixed prices become outdated within two years. Book value dramatically undervalues service businesses with minimal tangible assets. Multiple-of-revenue approaches work better for established businesses with predictable cash flow. The most sophisticated agreements require professional appraisals every two to three years, with the most recent appraisal controlling. A properly structured agreement's valuation typically establishes estate tax value, preventing IRS challenges.

Voting versus non-voting shares allow founders to transfer wealth while retaining control. A distribution company recapitalizes into 10% voting Class A shares and 90% non-voting Class B shares. The founder keeps all Class A shares (10% of economic value) while gifting Class B shares (90% of economic value) to his three children over several years. The founder maintains complete decision-making authority while removing 90% of the business value from his taxable estate.

The IRS scrutinizes these arrangements intensely. You need legitimate business reasons beyond tax avoidance. You must respect corporate formalities—separate meetings for different share classes, documented business decisions, arms-length transactions. Courts have disregarded voting/non-voting structures that exist only on paper.

Management transition addresses the human challenges succession planning often ignores. You have four children. Your oldest daughter has worked in the business for 15 years and understands every aspect. Your son is a software engineer in Seattle. Your younger daughters are a teacher and a physician. How do you treat them equitably without forcing your business-involved daughter to share control with siblings who have zero interest or experience?

Many successful plans give the active child controlling interest in the business while equalizing overall inheritance through life insurance or other assets. Some use phantom stock or deferred compensation rewarding key non-family employees who ensure business continuity. Outside board members provide accountability and mediate family conflicts.

Intentionally Defective Grantor Trusts offer remarkable business succession advantages. You sell your $5 million business interest to an irrevocable trust in exchange for a promissory note. The sale freezes your estate tax value at $5 million while moving all future appreciation to the trust for your beneficiaries. Over 15 years, the business grows to $22 million. You've transferred $17 million in appreciation without estate or gift tax.

The trust is "defective" for income tax purposes, meaning you personally pay income taxes on trust earnings. This further reduces your taxable estate without gift tax consequences—you're essentially making tax-free gifts equal to the tax you pay on trust income.

Multi-Generational Wealth Transfer Planning

Families building lasting legacies think beyond their children to grandchildren, great-grandchildren, and descendants they'll never meet.

Dynasty trusts in perpetuity-friendly jurisdictions continue for centuries. A $10 million dynasty trust growing 6% annually becomes $100 million in 40 years, $339 million in 60 years, and over $1 billion in 80 years—with zero estate tax at each generation. Delaware, South Dakota, and Nevada permit perpetual trusts without time limits. Most states restrict trusts to 90 years or "lives in being plus 21 years."

GST exemption allocation requires careful attention. Each person gets a $13.99 million generation-skipping transfer exemption (2026) protecting transfers to grandchildren or dynasty trusts from the 40% GST tax. Automatic allocation rules don't always produce optimal results, particularly with indirect gifts to trusts or complex ownership structures. Manual allocation on your gift tax return ensures the exemption gets applied where it provides maximum benefit.

Education trusts provide for multiple generations while maintaining family control. Unlike 529 plans with limited investment options and strict usage rules, education trusts can hold any asset and include provisions reflecting family values. Some families require beneficiaries to maintain minimum GPAs. Others restrict distributions to accredited institutions or prohibit certain fields of study. One family's education trust provides full funding for any degree in STEM fields but only 50% funding for liberal arts degrees, reflecting the patriarch's engineering background and values.

Incentive provisions encourage desired behaviors without excessive control. Common approaches include matching earned income (the trust distributes one dollar for every dollar the beneficiary earns from employment), requiring undergraduate degrees before receiving principal distributions, or providing bonuses for specific achievements—graduate degrees, starting businesses, or performing public service.

Poorly drafted incentive provisions backfire spectacularly. One trust penalized beneficiaries who didn't earn at least $100,000 annually—inadvertently discouraging a grandchild from becoming a social worker, which aligned perfectly with the family's stated values. Another trust required beneficiaries to work for the family business, creating resentment and forcing an artistically talented grandchild into a career she hated.

Spendthrift protections prevent beneficiaries from pledging trust assets or creditors from seizing trust funds. A beneficiary with gambling addictions, multiple divorces, or poor financial judgment receives distributions at the trustee's discretion rather than lump-sum inheritance. Discretionary distribution standards—"health, education, maintenance, and support"—provide flexibility while maintaining protection. The trustee might deny distribution requests for a luxury car but approve distributions for medical expenses, housing, or starting a business.

The 529 plan superfunding technique allows grandparents to accelerate five years of annual exclusion gifts ($18,000 per beneficiary in 2026) into a single year without gift tax. A couple with five grandchildren can move $450,000 out of their taxable estate immediately while maintaining control over education funding. Recent legislation permits rolling unused 529 funds to Roth IRAs (subject to certain conditions), adding flexibility for over-funded accounts when grandchildren receive scholarships or don't attend college.

Author: Jonathan Whitmore;

Source: harbormall.net

Common Mistakes in Comprehensive Estate Planning

Even sophisticated plans fail through implementation oversights and maintenance neglect.

Beneficiary designation conflicts undermine entire estate plans. Your carefully drafted trust provides creditor protection, controls distributions, and minimizes taxes. But your $9 million in retirement accounts and $4 million life insurance policy pass via beneficiary designation, not through your trust. You named your spouse as primary beneficiary and children as contingent beneficiaries—completely bypassing your trust structure.

Retirement accounts should name trusts as beneficiaries when asset protection or distribution control matters more than maximum stretch distributions. Accumulation trusts provide creditor protection but compress required minimum distributions. Conduit trusts provide longer stretch periods but force immediate distributions to beneficiaries. The optimal choice depends on your priorities and beneficiaries' situations.

State law conflicts create nightmares for multi-state families. Community property states (California, Texas, Arizona, Idaho, Louisiana, Nevada, New Mexico, Washington, Wisconsin) treat marital assets fundamentally differently than common law property states. A couple married in California who retires to Florida discovers their trust no longer functions as intended. Assets they believed were separate property might be community property under California law, affecting how those assets transfer at death.

Some states recognize domestic asset protection trusts; others don't. If you establish a Nevada DAPT but remain living in California, will California courts honor Nevada's asset protection provisions? The case law remains unsettled, creating risk.

Homestead protections vary wildly. Florida provides unlimited homestead protection—your $15 million Miami mansion is fully protected from creditors. New York caps homestead exemption at $170,000. Your asset protection strategy must account for these variations.

Inadequate liquidity forces fire sales of family businesses and real estate. A $35 million estate consists of a $28 million family business, $4 million in real estate, and $3 million in other assets. Federal estate tax approaches $8 million. The family has nine months to pay. Without life insurance or liquid reserves, they must sell the business quickly—typically at a 20-30% discount—to meet the deadline. Section 6166 allows deferring estate tax payments over 14 years for closely-held businesses, but you must meet strict requirements and pay interest.

DIY complex structures fail with mathematical certainty. Online legal services handle simple wills adequately but cannot navigate sophisticated planning nuances. A self-drafted GRAT with an incorrectly calculated annuity payment or missing required provisions provides zero tax benefit while creating a complicated mess requiring expensive cleanup. The IRS successfully challenges improperly drafted family limited partnerships, disallowing valuation discounts and imposing penalties exceeding 40% of the tax deficiency.

Tax law change failures waste opportunities. The estate tax exemption has fluctuated dramatically—$1 million in 2002, $5 million in 2011, $11.58 million in 2020, $13.99 million in 2026. Trusts drafted with formula clauses based on outdated exemptions distribute assets in ways the grantor never intended. The 2025 sunset reverting exemptions to approximately $7 million requires immediate planning adjustments for families with $10-25 million estates.

State income tax consequences cost hundreds of thousands unnecessarily. Trusts pay income tax based on trustee residency and administration location. A trust administered in California pays California's 13.3% top rate on accumulated income. Moving administration to Nevada, Texas, or Florida eliminates state income tax on trust earnings—potentially saving $130,000 annually on $1 million in trust income, or $3.25 million over 25 years.

When to Work with Specialized Estate Planning Professionals

The biggest mistake I see is families waiting until it's too late.You need years for sophisticated techniques to work properly. GRATs require surviving the trust term. Business succession needs gradual transition. Families who wait until a health crisis or imminent business sale lose the most valuable planning opportunities and often pay millions more in unnecessary taxes

— Jennifer Martinez

Complex planning demands a team with defined expertise in complementary areas.

Estate planning attorneys draft legal documents ensuring technical tax law compliance. Look for attorneys with LL.M. (Master of Laws) degrees specifically in taxation or estate planning—not general practitioners who occasionally draft wills between personal injury cases. Some state bars offer board certification in estate planning, indicating advanced specialization. Expect investment of $8,000-20,000 for moderately complex planning involving multiple trusts and business succession. Sophisticated multi-generational wealth transfer with dynasty trusts, GRATs, and asset protection structures runs $35,000-100,000 in legal fees.

Financial planners model scenarios and coordinate asset positioning. A CFP® with additional estate planning credentials can illustrate how different strategies affect long-term wealth transfer—comparing GRAT versus IDGT versus outright gifting. But planners cannot draft legal documents. Fee-only compensation avoids conflicts inherent in commission-based arrangements where the planner profits from selling products.

CPAs handle tax compliance and calculate income tax consequences of planning strategies. Your estate planning attorney designs an elegant life insurance trust, but your CPA ensures premium payment gifts don't trigger unexpected gift tax returns. The CPA ensures trust accounting complies with grantor trust rules under IRC Sections 671-679. The CPA calculates whether a Roth conversion makes sense within your dynasty trust structure.

Wealth managers implement investment strategies within trust structures, balancing tax efficiency against distribution requirements. A dynasty trust requiring 5% annual distributions needs different asset allocation than an accumulation trust holding everything for 30 years. Capital gains realizations affect trust income tax differently than individual taxation. Trust investments must coordinate with distribution provisions and beneficiary needs.

Corporate trustees provide professional management for multi-generational trusts. While your brother-in-law can handle your simple revocable living trust, a dynasty trust continuing for a century needs institutional expertise. Corporate trustees charge 0.50-1.25% of assets annually but provide investment management, tax compliance, impartial distribution decisions, and perpetual existence. Northern Trust, Bessemer Trust, and other institutional trustees survive individual family members.

Red flags signaling inadequate expertise include attorneys asking few questions about family dynamics before recommending strategies, planners pushing specific products before understanding needs, or any professional claiming one-size-fits-all approaches work. Be wary of advisors who cannot clearly explain how strategies work or who dismiss questions about downsides and risks. Run from anyone guaranteeing specific tax results or claiming their strategies are "IRS-proof."

Start planning 5-10 years before anticipated need. Business owners should begin succession planning a decade before intended retirement. Waiting until terminal diagnosis or family crisis forces rushed decisions under pressure. GRATs need years to work. Business transitions require gradual responsibility transfer. Sophisticated strategies require time to implement correctly.

Comparison of Common Advanced Planning Techniques

| Technique | What It Does | Tax Advantage | Difficulty Level | Works Best For | Can You Change It? |

| GRAT | Moves asset appreciation to heirs while you receive payments | Removes growth above IRS rate from estate without using gift exemption | Moderate | Stock portfolios, business interests expected to appreciate significantly | No—irrevocable |

| QPRT | Transfers your home at reduced value while you keep living there | Reduces gift tax value through retained residence term | Moderate | Primary residence or vacation home | No—irrevocable |

| ILIT | Takes life insurance proceeds out of taxable estate | Death benefit avoids estate tax completely | Low to Moderate | Policies over $1 million where estate tax applies | No—irrevocable |

| FLP/LLC | Creates valuation discounts on business/investment transfers | 25-40% discounts reduce gift tax on transfers | High | Real estate portfolios, investment accounts, business interests | No—irrevocable |

| CRT | Provides lifetime income plus tax deduction with charity receiving remainder | Avoids capital gains, gets income deduction, removes assets from estate | Moderate to High | Highly appreciated stock or real estate | No—irrevocable |

Frequently Asked Questions

Sophisticated wealth transfer separates families who successfully pass fortunes across generations from those losing millions to avoidable taxes, creditor claims, and family conflicts. The techniques discussed—grantor retained annuity trusts, dynasty trusts, business succession planning, asset protection structures—demand upfront investment in professional guidance and ongoing maintenance. But for families with significant assets or complicated situations, returns dwarf the costs.

Your most critical decision is starting before crisis forces rushed, suboptimal choices. Business owners should begin succession planning a decade before intended retirement. Families approaching estate tax thresholds should implement strategies while healthy and mentally sharp. Anyone facing creditor risks must establish protection before claims materialize—after-the-fact asset protection rarely survives legal scrutiny.

No single strategy fits every family. Your specific situation—asset types, family relationships, business interests, risk tolerance, and long-term objectives—determines optimal approaches. The comprehensive plan working brilliantly for one family might be completely inappropriate for another with identical net worth but different goals.

Work with qualified specialists who invest time understanding your unique situation, explain strategies in understandable terms, and implement plans that will function correctly for decades. The investment in proper planning today protects wealth you spent a lifetime building and creates the legacy you envision for generations you'll never meet.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.