Young single adult reviewing legal estate planning documents at a modern apartment desk with warm lighting

Estate Planning for Singles Guide

Think estate planning only kicks in once you've got a wedding ring and kids? Here's the reality check: single adults actually face bigger risks when they skip this step. Your closest friend from college—the one who knows your Netflix password and has a key to your apartment? Legally, they're invisible when it comes to your estate. That charity you donate to every year? They won't see a dime unless you specifically arrange it.

Here's what actually happens: if you pass away without proper documents, your state decides everything. Relatives you barely remember from childhood reunions might end up with your house, your savings, and even your dog. The process drags on for months while lawyers rack up fees and family members argue about who gets what. And every single detail becomes public record that anyone can look up online.

The good news? Fixing this takes less time than planning a vacation.

Why Single Adults Need Estate Planning

Most people think estate planning belongs on the "someday after I settle down" list. That's backward thinking that leaves single adults uniquely exposed.

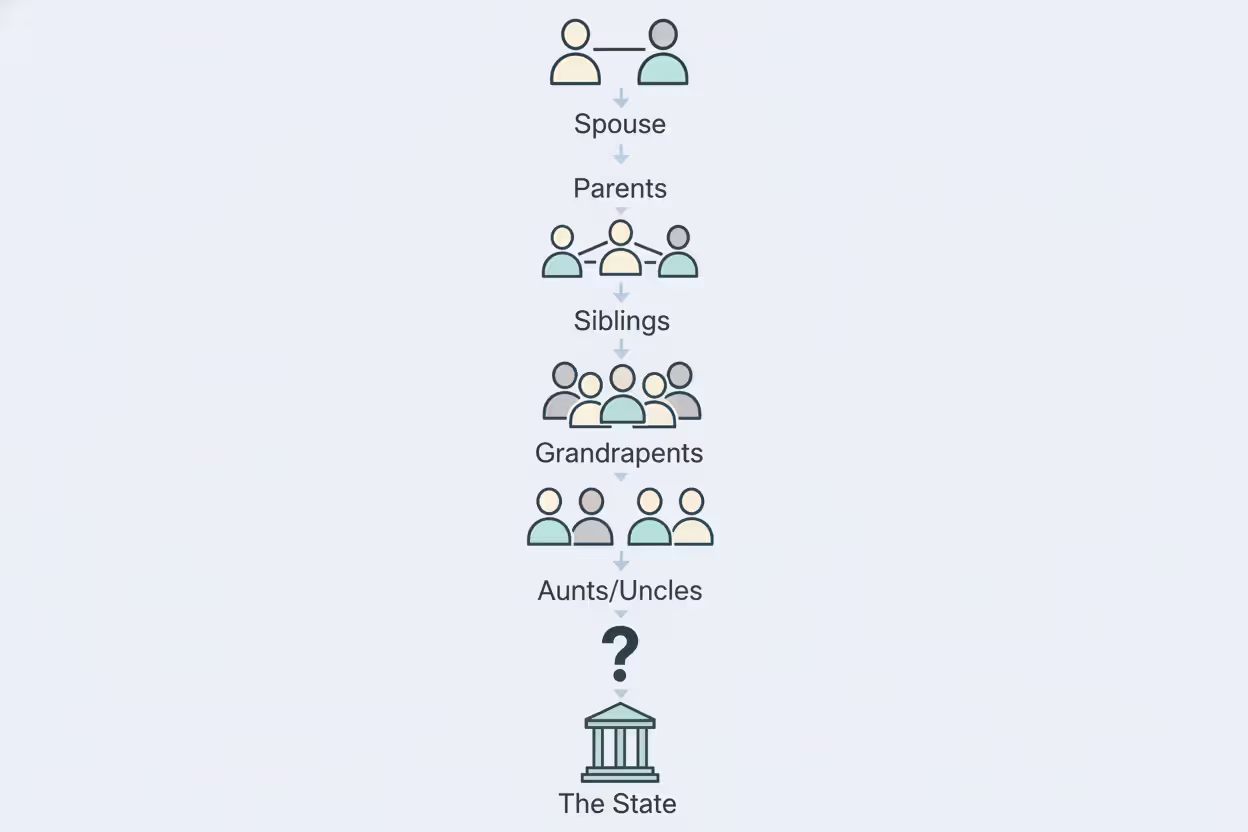

State intestacy rules kick in whenever someone dies without a will. These rules operate like an assembly line—zero flexibility, zero personalization. First in line: your spouse and kids. Don't have those? Next up: your parents get everything. Both parents gone? Your siblings split it all.

Let's look at California's approach. Say you're single, both parents are living, and you die without a will. They split everything 50/50. Lost one parent already? The surviving parent shares your estate with your siblings—even siblings you haven't talked to in years. What if both parents have passed? Your estate moves to grandparents. No grandparents? Aunts and uncles. Still nobody? Cousins start looking pretty good to the state. Run out of findable relatives? Congratulations—the state government becomes your sole heir.

Author: Jonathan Whitmore;

Source: harbormall.net

Here's the part that surprises most singles: the medical decision problem. Married folks automatically have someone with legal authority to make healthcare choices if they're unconscious or incapacitated. You're on your own unless you've signed the right documents. Hospitals will track down your next of kin by law—typically parents or siblings. What if your family holds religious views that clash with yours? What if they'd keep you on machines indefinitely when you'd want comfort care? Without paperwork saying otherwise, their preferences override yours.

The financial squeeze hits differently too. Imagine you're in a serious car accident and spend two months in a coma. Who pays your mortgage while you're unconscious? Who handles your credit card bills, your investment accounts, your business obligations? Your best friend might have the best intentions, but banks won't talk to them. Family members need to file for conservatorship—a court process that takes months, costs thousands, and exposes your financial life to public scrutiny.

Key Documents in a Single Person Estate Plan

Building a solid estate plan means assembling several documents that work together. Miss one piece and you've left a dangerous gap.

Will and Testament

Your will names an executor—the person who'll inventory your property, pay final bills, file tax returns, and distribute assets according to your instructions. For singles, executor selection demands extra thought since you can't fall back on naming your spouse. Pick someone detail-oriented and responsible, not just whoever seems like the obvious family choice.

Wills also settle the question of who gets your stuff—the things that matter emotionally rather than financially. Your vintage concert poster collection, your grandmother's engagement ring, the pottery you made in that class last summer. These items spark more family fights than bank accounts because everyone attaches different memories and meaning to them. Spell out exactly who gets what to head off arguments later.

Revocable Living Trust

Trusts aren't reserved for millionaires anymore. If you own property, maintain substantial investment accounts, or value your privacy, trusts deliver concrete advantages. Assets titled in a trust skip the probate court entirely. That means faster access for beneficiaries, lower administrative costs, and—crucially—no public filing that lists everything you owned.

Privacy carries extra weight for single adults who've built wealth. Probate creates permanent court records accessible to anyone with internet access. Nosy neighbors, estranged relatives, con artists—they can all look up what you owned and who got it. For singles with significant assets, this transparency can expose beneficiaries to unwanted attention or scams.

Trusts shine during incapacity too. The successor trustee you've named can step in immediately to manage trust assets if you're unable to handle things yourself. Contrast that with individually-owned assets, which freeze until someone goes through court proceedings to get authority over them.

Healthcare Directives and Power of Attorney

A healthcare directive (some states call it a living will or advance directive) documents your preferences for end-of-life medical treatment. Should doctors attempt aggressive interventions or focus on keeping you comfortable? Would you want feeding tubes? Ventilators? For how long? These aren't pleasant questions, but leaving them unanswered forces grieving family members to guess what you'd want.

The healthcare power of attorney designates your medical decision-maker—someone authorized to direct your care when you can't speak for yourself. Solo estate planning requires choosing an agent who genuinely knows your values, keeps their cool during crises, and lives close enough to reach you quickly in emergencies. Always name backup agents. Your first pick might be traveling, sick, or otherwise unavailable exactly when you need them.

Author: Jonathan Whitmore;

Source: harbormall.net

Financial Power of Attorney

This paperwork gives someone authority over your money and financial decisions during incapacity. Your designated agent gains the ability to handle bill payments, manage your portfolio, complete tax filings, and conduct banking transactions. Skip this document and your finances lock up until a court assigns a conservator.

Singles should weigh whether this power of attorney takes effect right away or only after you become incapacitated (called a "springing" provision). Immediate effectiveness offers convenience—your agent can help with routine tasks even while you're fine. But it requires complete confidence in their integrity. Springing provisions protect you better but can cause friction if banks demand extensive proof that you're actually incapacitated.

Who Should Single People Name as Beneficiaries

Estate planning without children opens up beneficiary possibilities that traditional families rarely explore. You're free to distribute assets based on your actual relationships rather than following conventional family hierarchies.

Siblings make intuitive beneficiaries when you're close and they're financially stable. But "equal shares for all siblings" isn't mandatory. Maybe one sibling helped you through a rough patch while another barely stayed in touch. Perhaps one sibling shares your environmental values and would use inherited land responsibly while another would sell to the first developer who called. Your estate, your rules.

Friends absolutely qualify as beneficiaries—the law doesn't mandate blood relations. If your closest friend has been your emergency contact for a decade, joined you on major trips, and listened to you process every career decision, they might deserve an inheritance more than cousins you see at weddings. Just be crystal clear in your documents since family members sometimes challenge bequests to non-relatives.

Charitable giving lets you cement the values you lived by. Many singles direct major portions of their estates toward causes they supported throughout life. You can structure charitable bequests as fixed dollar amounts, percentages of your total estate, or residuary gifts (whatever remains after other distributions). Bonus: for larger estates, charitable contributions reduce estate tax exposure.

Nieces and nephews occupy an interesting space—family connection without parenting responsibilities. Plenty of single adults enjoy mentoring younger relatives and want to fund their education or early career. Think about trusts that release funds at milestone ages—say 25, 30, and 35—rather than dumping a massive inheritance on a 21-year-old who's never managed serious money.

Your parents might still be around when you draft your estate plan. If they're financially comfortable, directing assets elsewhere might make more sense. But if they'll potentially need expensive care later, reserving funds for their benefit shows foresight. A trust that supports parents during their remaining years, then passes leftover assets to your other chosen beneficiaries, accomplishes multiple goals simultaneously.

The real question isn't "who does society expect me to choose" but "who reflects my actual values and relationships." Family pressure and social conventions shouldn't override your authentic wishes.

Author: Jonathan Whitmore;

Source: harbormall.net

Common Estate Planning Mistakes Singles Make

Single adults encounter specific traps in estate planning. These errors show up repeatedly and can demolish even well-intentioned plans.

Assuming family automatically inherits according to your unspoken wishes tops the mistake list. State intestacy laws operate on rigid formulas that completely ignore personal relationships. Your favorite cousin gets zero if you have living siblings. Your partner of ten years receives nothing if you never married. Only properly documented estate planning overrides these legal defaults.

Ignoring beneficiary designations creates chaos and potential lawsuits. Retirement accounts, life insurance policies, and payable-on-death bank accounts transfer directly to whoever's listed as beneficiary—your will has zero impact on these assets. Maybe you listed your college boyfriend as beneficiary twelve years ago and forgot about it. He'll inherit that retirement account regardless of your will's instructions. Mark your calendar to review every beneficiary designation annually and immediately after relationship changes.

Overlooking digital assets leaves executors stuck. Your executor needs email access to notify contacts and track down recurring charges. They need your photo cloud passwords to preserve and share memories with family. They need cryptocurrency wallet information to access digital holdings. Create a separate inventory of digital assets with account names and password location hints (stored securely separate from the list itself).

Skipping incapacity planning assumes you'll be either healthy or dead—nothing in between. Real life includes scenarios where you're alive but unable to communicate or make decisions. Comas, strokes, dementia, traumatic injuries. Without healthcare and financial powers of attorney, courts determine who controls your medical care and money. That court process is public, expensive, and agonizingly slow.

Selecting the wrong fiduciaries sabotages everything else. Your executor, trustee, and power of attorney agents need specific capabilities: organizational skills, financial literacy, emotional steadiness, and actual availability. Don't choose someone purely because they're family or because you worry about hurting feelings. Choose people genuinely capable of handling these responsibilities.

Keeping your plans secret guarantees confusion and hurt. You don't need to broadcast every detail, but your executor and agents should know you've designated them and where your documents are stored. Making surprising choices—leaving your entire estate to a charity or excluding a family member—warrants some explanation. Consider writing a personal letter (kept separate from legal documents) explaining your reasoning to reduce the chances of costly legal challenges.

How Much Does Estate Planning Cost for Single Adults

Cost concerns delay estate planning, but available options fit virtually any budget. Understanding what you're buying helps you choose the right service tier.

| Service Type | Typical Cost | What's Included | Who It Fits |

| DIY Software | $100–$300 | Basic will, simple powers of attorney, healthcare directive | Minimal assets, straightforward wishes, comfortable with technology, simple family situation |

| Online Legal Services | $300–$800 | Will, revocable living trust, both powers of attorney, healthcare directive | Moderate complexity, some property ownership, clearly defined beneficiaries |

| Flat-Fee Attorney Package | $1,200–$2,500 | Complete document suite plus professional consultation | Most single adults, anyone wanting expert review, moderate to complex assets |

| Full-Service Estate Attorney | $2,500–$5,000+ | Comprehensive planning, multiple meetings, annual reviews available | High net worth, complicated assets, business ownership, tax planning considerations |

DIY software handles straightforward situations: modest assets, obvious beneficiary choices, uncomplicated family relationships. The software walks you through questionnaires and produces legally recognized documents. The danger? You don't know what you don't know. You might miss planning opportunities or make technical errors that only surface after you've died.

Online legal services split the difference. Companies like LegalZoom or Nolo provide more structure than pure DIY software, sometimes including brief attorney reviews. These services manage routine estate planning adequately but might miss unique issues specific to your circumstances.

Flat-fee attorney packages deliver optimal value for most single adults. You receive professionally customized documents tailored to your situation, plus the chance to ask questions and understand your options. Attorneys catch problems you'd never spot—outdated beneficiary forms, the need for specific trust language based on your state's laws, or gaps between what you think you've accomplished and what your documents actually say.

Full-service estate attorneys justify their cost when you're dealing with business ownership, extensive property holdings, complicated family situations, or estates approaching federal estate tax thresholds ($12.92 million for 2023). Higher fees buy ongoing professional relationships, sophisticated tax strategies, and comprehensive confidence that your plan addresses every angle.

Factor in additional expenses: notarization typically runs $10–$50, recording fees if you're filing deeds vary by county, and safe deposit boxes for storing original documents cost $30–$150 yearly.

The priciest option? Doing nothing. Probate costs for estates without proper planning typically consume 3–7% of total estate value, plus months or years of delays. Spending $3,000 on proper planning can save a $300,000 estate somewhere between $9,000 and $21,000 just in probate costs.

When to Update Your Solo Estate Plan

Author: Jonathan Whitmore;

Source: harbormall.net

Estate plans need maintenance—they're not one-and-done documents. Life changes require corresponding updates to keep your plan aligned with current reality.

Major asset shifts trigger review requirements. Purchased a house since creating your plan? Received an inheritance? Built up substantial retirement savings? Check whether your existing documents still reflect your intentions. A will directing "equal distribution to my siblings" might have seemed reasonable when your estate totaled $50,000. At $500,000, you might want more sophisticated provisions.

Relationship changes—new connections or broken ones—demand immediate attention. Fresh romantic relationships, deepening friendships, or estrangements from family members all reshape who you want making decisions and inheriting assets. If you've grown distant from the friend you named executor five years back, update that designation before an emergency forces them into an awkward position they don't want.

Relocating to another state requires legal review. Estate planning laws differ substantially across states. Your New York will remains technically valid after you move to Texas, but Texas law governs how it's interpreted and executed. Some states recognize common law marriage; others don't. Community property states treat asset ownership differently than common law property states. Healthcare directive requirements vary. Get an attorney in your new state to review everything within a year of moving.

Aging parents reshape your planning considerations. If your parents have entered their eighties or nineties, account for the possibility they'll die before you do. Revise contingent beneficiaries to reflect who should inherit if your primary choices aren't around. Consider whether you want to reserve funds to help siblings who might shoulder parent caregiving responsibilities.

Fresh additions to the family—nieces, nephews, godchildren—expand your circle. You might want educational provisions or trusts that distribute at milestone ages. Even if they're not major beneficiaries, small bequests or meaningful personal items can forge lasting connections.

Changes in your fiduciaries' circumstances matter too. Maybe your named executor relocated across the country, developed serious health issues, or went through a messy divorce. They might no longer suit the role. If your backup agent has passed away, designate a new one—backup provisions prevent court involvement if your first choice can't serve.

Tax law changes occasionally demand planning adjustments. Federal estate tax exemptions shift over time, and some states maintain their own estate or inheritance taxes with lower thresholds. Significant tax legislation might create fresh planning opportunities or eliminate strategies your current plan relies on.

General guideline: review your estate plan every three to five years minimum even when nothing dramatic has changed, and immediately following significant life events.

Single adults often have the most flexibility in estate planning because they're not constrained by spousal or parental obligations.But that flexibility only matters if you actually create a plan. I've seen too many single clients assume they have plenty of time, then face a health crisis without proper documents in place. The peace of mind that comes from having your affairs in order is worth far more than the time and money it takes to create a plan

— Jennifer Martinez

Frequently Asked Questions About Estate Planning Without Children

Estate planning for singles isn't preparing for death—it's taking control while you're living. It's ensuring your healthcare preferences get respected if you're in an accident next week. It's guaranteeing your assets reach people and causes you genuinely care about. It's sparing people you love from legal complications during an already painful time.

The process doesn't require complexity or massive expense. Start with fundamentals: a will, powers of attorney, and healthcare directives. You can layer in trusts and more sophisticated strategies later as your assets grow or circumstances change. What matters is establishing something now rather than leaving everything to state default provisions.

Your estate plan reflects your values, relationships, and priorities. Invest time thinking through who you trust, what matters most to you, and what legacy you want to create. Then document it through properly executed legal instruments. Your future self—and the people you care about—will be grateful you did.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.