Estate planning documents and beneficiary designation form on a desk

Estate Planning Beneficiaries Guide

Trillions of dollars transfer through beneficiary designations each year, yet most people spend more time planning a vacation than reviewing these critical forms. These designations determine who receives your retirement accounts, life insurance proceeds, and certain bank accounts—completely outside of probate court. They're among your most powerful planning tools, but outdated or conflicting designations create costly problems that tear families apart.

What Are Beneficiaries in Estate Planning

When you name a beneficiary, you're creating a legally binding instruction for who receives specific assets after your death. Financial institutions use these designation forms as contracts—they must pay the people you name, regardless of what family members think should happen or what circumstances have changed.

Most people encounter beneficiary forms when opening a 401(k), buying life insurance, or setting up certain investment accounts. The forms seem simple, but the decisions you make have lasting consequences.

The law recognizes two beneficiary categories:

Primary beneficiaries stand first in line to inherit. You decide how to split assets among them using percentages that must total 100%. Three children named as equal primaries? Each receives one-third of that specific account's value.

Contingent beneficiaries receive assets only when every primary beneficiary has died before you or legally refuses their inheritance. These backup designations prevent assets from flowing into your estate (and probate court) when your first-choice recipients aren't available to inherit.

People often confuse beneficiaries with heirs, but they're completely different. Heirs are relatives defined by your state's family law who inherit when you die without a will. Beneficiaries are people or entities you specifically choose, regardless of their relationship to you. Your beneficiaries might include a lifelong friend, domestic partner, favorite charity, or a trust—none of whom might qualify as legal heirs.

You'll need beneficiary designations for:

- All retirement plans: 401(k)s, 403(b)s, traditional and Roth IRAs, pensions

- Life insurance policies and annuity contracts

- Bank accounts with payable-on-death provisions

- Investment accounts with transfer-on-death registrations

- In certain states, real property with transfer-on-death deeds

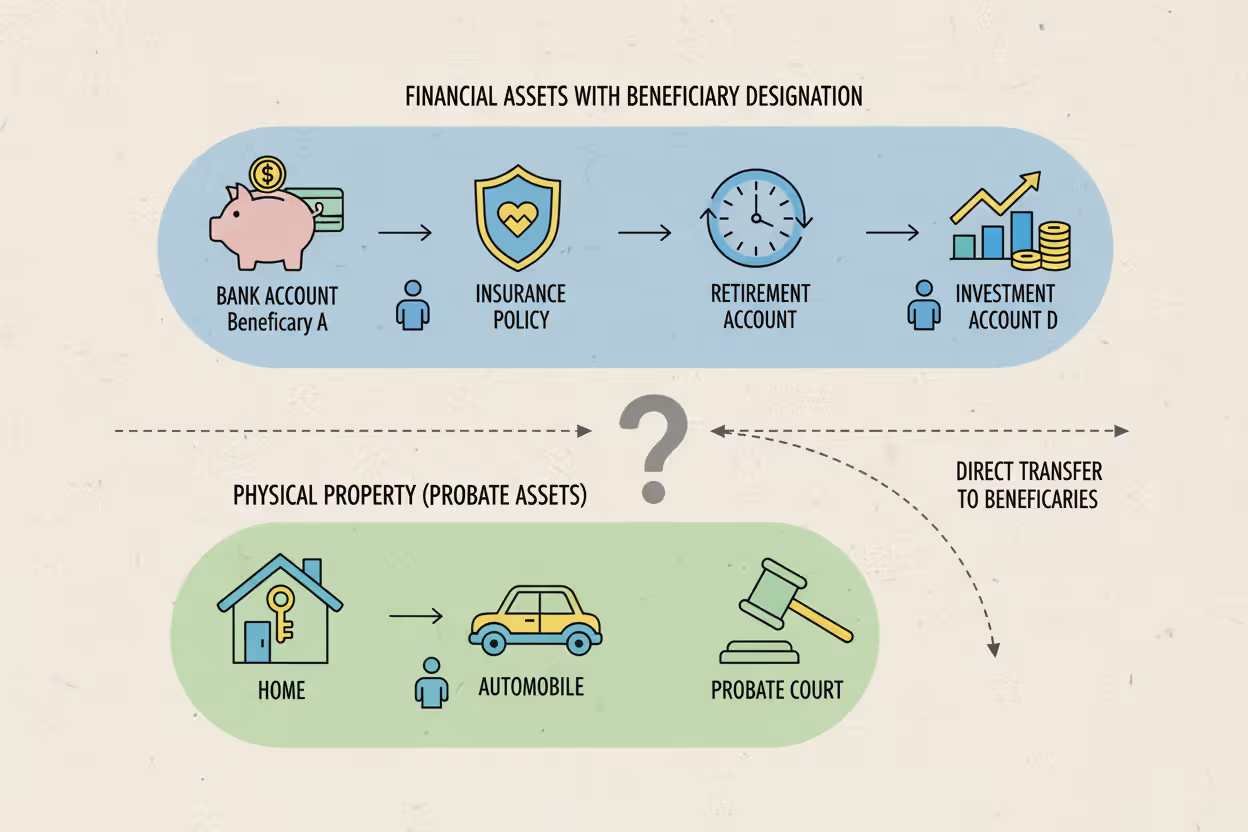

Your home, car, jewelry, and other physical property generally cannot use beneficiary designations. These assets pass through your will or, without one, through your state's intestacy statutes.

Author: Jonathan Whitmore;

Source: harbormall.net

Types of Beneficiary Designations You Need to Know

Each asset type uses specialized beneficiary mechanisms with distinct rules and consequences. Knowing the differences helps you build a coordinated estate strategy.

Payable on Death (POD) Accounts

Banks offer payable on death registrations for checking accounts, savings accounts, money market deposits, and CDs. During your lifetime, you have absolute control—spending, saving, and managing the money however you choose. The beneficiaries you name have zero access or rights while you're alive.

After you die, your POD beneficiaries simply present your death certificate to the bank. Within a few business days, they receive the funds directly. Your executor never touches this money, and your creditors generally cannot reach it to satisfy estate debts. The transfer happens outside probate entirely.

Transfer on Death (TOD) Accounts

Transfer on death works like POD but applies to securities and investment accounts. Your brokerage account, individual stocks, bonds, and mutual fund holdings can all carry TOD designations.

Several states now permit transfer-on-death deeds for homes and land. You record a deed naming someone to inherit your property automatically upon your death, avoiding probate. You keep full ownership rights while alive—you can sell the property, refinance it, or even revoke the TOD deed entirely. Currently, about 30 states authorize this option, though each state's requirements differ substantially.

Retirement Account Beneficiaries

Every retirement account—traditional IRA, Roth IRA, 401(k), 403(b)—requires a beneficiary designation. Who you name dramatically affects how much tax your beneficiaries will pay.

Surviving spouses enjoy unique advantages. They can move inherited retirement money into their own IRA through a spousal rollover, treating the funds as if they'd contributed them personally. This strategy maximizes tax deferral and delays required withdrawals.

Everyone else faces tighter constraints. The SECURE Act rules enforced in 2026 require most non-spouse beneficiaries to empty inherited retirement accounts within ten years of the owner's death. A few categories escape this rule: minor children until age 18-21, chronically ill or disabled individuals, and beneficiaries born less than ten years after the account owner.

Life Insurance Beneficiaries

Insurance companies pay death benefits directly to whoever you named as beneficiary, typically without any income tax. The money bypasses probate and usually arrives within 30 days of the insurance company receiving your death certificate and a completed claim form.

Life insurance offers flexible beneficiary structures. Per capita arrangements divide benefits equally among all living named beneficiaries. Per stirpes (sometimes called "by representation") arrangements protect your family tree—if one of your named children dies before you, that child's portion flows to their own children instead of being redistributed among your surviving children.

Here's how these options compare:

| Account Type | Transfer Mechanism | Passes Through Probate? | Tax Treatment | Ideal Uses |

| POD (Bank Deposits) | Beneficiary shows death certificate to bank | No | No income tax; counts in estate value | Quick cash access, paying final expenses |

| TOD (Investments) | Automatic securities transfer to beneficiary | No | Stepped-up cost basis for capital gains | Brokerage accounts, individual securities |

| Retirement Plans | Transfer with mandatory distribution schedules | No | Taxable income to beneficiary; 10-year withdrawal rule | Long-term savings, substantial wealth transfers |

| Life Insurance | Direct death benefit payment | No | No income tax on proceeds; potential estate tax | Replacing lost income, estate liquidity |

How to Choose the Right Beneficiaries for Your Estate

Selecting beneficiaries involves more strategic thinking than just listing your closest relatives. Multiple factors should influence your choices:

Consider each person's financial capability. Someone who's terrible with money or struggles with addiction might burn through a six-figure inheritance in months. For beneficiaries who need protection from themselves, naming a trust as beneficiary—with an independent trustee controlling distributions—offers better protection than handing over a lump sum.

Factor in age and life stage. The law prohibits minors from directly owning substantial assets. If a 10-year-old inherits your $300,000 IRA, a court must appoint a conservator to manage the money until your child legally becomes an adult—a process that costs thousands in legal fees. Better approaches include establishing a trust to receive the funds or using your state's Uniform Transfers to Minors Act provision, which lets a custodian manage money until your child reaches age 21 or 25, depending on your state.

Make your math precise. When you name several primary beneficiaries, your percentages must equal exactly 100%. Unequal splits are perfectly acceptable—maybe you want one child to receive 60% and two others to each receive 20%—but verify your arithmetic works.

Watch out for these frequent errors:

Listing your estate as the beneficiary. This approach defeats the primary purpose of beneficiary designations by routing assets through probate court. Your estate's creditors can then claim those funds, and settlement costs will reduce what your heirs receive. Name your estate as beneficiary only when you deliberately want those assets governed by your will's distribution scheme.

Assuming divorce terminates your ex-spouse's beneficiary status. Most states don't automatically remove former spouses from beneficiary forms when your divorce becomes final. A handful of states have laws voiding these designations post-divorce, but many states—and federal law governing workplace retirement plans—don't. You must file new paperwork removing your ex-spouse's name.

Thinking your will overrides beneficiary forms. It doesn't. If your will leaves everything equally to all your children, but your largest asset—a $600,000 IRA—names only your oldest son, he inherits that entire account. Your will only controls assets without beneficiary designations.

Blended families face particularly complex choices. You might want your current spouse financially secure while guaranteeing your children from your first marriage eventually inherit. A QTIP trust accomplishes this balance—your spouse receives trust income for life, then your children inherit the remaining principal after your spouse passes away.

Using trusts as beneficiaries provides control and asset protection in several scenarios:

- Beneficiaries receiving government disability benefits who'd lose eligibility with direct inheritance

- Children or young adults not ready to manage large sums

- Beneficiaries facing lawsuits, bankruptcy, or divorce

- Situations requiring staged distributions over time rather than lump-sum payments

Charitable organizations make excellent beneficiaries, especially for retirement accounts. Charities pay no income tax on IRA distributions. Your children would pay income tax on every dollar withdrawn from an inherited IRA. Leaving retirement money to charity while giving other assets to family often produces superior tax results overall.

Author: Jonathan Whitmore;

Source: harbormall.net

Estate Planning for Beneficiaries With Special Needs

Naming a disabled family member directly as your beneficiary usually destroys their access to essential government support. Programs like Supplemental Security Income and Medicaid impose strict asset ceilings. SSI recipients in 2026 cannot possess more than $2,000 in countable resources. An inheritance exceeding this limit terminates their benefits until they've spent nearly everything.

This creates a devastating trap: the inherited money pays for care that government programs previously provided for free, potentially depleting the inheritance within a few years, after which your beneficiary must reapply for benefits from scratch.

Special needs trusts prevent this nightmare scenario. These trusts (also called supplemental needs trusts) hold assets for a disabled person's benefit without counting against benefit eligibility limits. Trust funds pay for quality-of-life expenses beyond what government benefits cover—specialized therapies, recreational activities, electronic devices, education programs, companion care, and travel—while preserving SSI and Medicaid access.

Two varieties exist with different rules:

First-party special needs trusts contain assets that belong to the disabled person themselves—perhaps from a lawsuit settlement or an inheritance they mistakenly received outright. These must include payback provisions requiring any remaining trust assets to reimburse the state's Medicaid program after the beneficiary dies.

Third-party special needs trusts hold money you're contributing for a disabled relative's benefit. These don't require state payback, so remaining assets can pass to other family members you designate.

When implementing estate planning for disabled beneficiaries, always name the special needs trust—never the disabled person—as beneficiary of your life insurance, retirement accounts, and other assets intended for their benefit. Even modest direct inheritances can disrupt benefits eligibility.

ABLE accounts work for smaller inheritances. These tax-advantaged accounts allow disabled individuals to save up to $18,000 annually (2026 contribution limit) without jeopardizing benefit eligibility. Account balances can grow beyond $100,000 for SSI purposes, though amounts exceeding $100,000 may affect eligibility. ABLE accounts work well for limited funds, but substantial estates still require special needs trusts.

When and How to Update Your Beneficiary Designations

Beneficiary forms aren't documents you complete once and ignore forever. Major life transitions require updates to align designations with your current intentions.

Update beneficiaries immediately following:

Getting married. You'll probably want your new spouse as primary beneficiary on most accounts. Federal ERISA law actually mandates that married 401(k) owners designate their spouse as primary beneficiary—naming someone else requires your spouse's notarized written consent.

Finalizing a divorce. Remove your ex-spouse and designate new beneficiaries right away. Your divorce decree almost certainly doesn't handle this automatically, despite what you might assume.

Welcoming a child through birth or adoption. Add your new child as a beneficiary and recalculate percentages to reflect your wishes for all your children.

Losing a beneficiary to death. When someone you've named dies, promptly update forms to reflect your current backup plan.

Experiencing major financial changes. As account values grow substantially, reassess whether your beneficiary structure still achieves your tax planning and family goals.

Relocating to another state. Community property rules and beneficiary designation laws vary significantly between states.

The typical client completes beneficiary forms when opening an account and then completely forgets they exist. I regularly encounter situations where someone's first spouse from decades ago receives everything because nobody ever updated the paperwork. Set a calendar reminder to review all your beneficiaries every three years minimum, and definitely after marriage, divorce, or having children

— Margaret Chen

Follow this process to update your designations:

- Contact every financial institution separately. Each account needs its own update. Changing your IRA beneficiary has zero effect on your 401(k), life insurance, or bank accounts.

- Obtain current beneficiary change forms. Many institutions offer online forms, though some still require paper documents.

- Complete forms with precision. Provide complete legal names, birth dates, and Social Security numbers. State exact percentages. Always include contingent beneficiaries.

- Follow submission procedures exactly. Some companies accept digital submissions; others demand original wet signatures.

- Obtain confirmation in writing. File these confirmations with your estate planning documents.

- Create a master beneficiary list. Maintain a comprehensive record showing every account and its current beneficiaries. Store this list where your executor can find it so nothing gets overlooked.

What happens when you never update? The old designation controls, regardless of how unfair the outcome seems. Courts enforce beneficiary forms exactly as written, even in obviously unjust situations. Your ex-spouse collects your life insurance death benefit. Your estranged brother inherits your IRA. Your will cannot change these results.

Dying without any beneficiary designation triggers default rules, which vary by account type. Retirement accounts typically make your estate the beneficiary, forcing the money through probate. Life insurance policies generally do the same. These defaults create unnecessary expenses and lengthy delays.

Author: Jonathan Whitmore;

Source: harbormall.net

Common Beneficiary Designation Mistakes That Cost Families

Even sophisticated planners commit beneficiary designation blunders that burden their families with problems.

Skipping contingent beneficiaries ranks among the most damaging oversights. When your sole primary beneficiary dies first and you've named no backups, the asset defaults to your estate, triggering probate proceedings. Name multiple layers of contingent beneficiaries to prevent this.

Creating conflicts between your will and beneficiary forms generates family confusion and sometimes litigation. Your will might direct equal division among your three children, but if your most valuable asset—a $500,000 retirement account—names only one child, that designation controls. The named child receives the full retirement account; your other children divide whatever remains. Coordinate all beneficiary designations with your comprehensive estate strategy.

Keeping ex-spouses as beneficiaries after divorce produces catastrophic outcomes. Many assume their divorce judgment automatically removes their former spouse from all accounts. In reality, most states require separate beneficiary change forms. Federal ERISA law governing workplace retirement and insurance plans overrides state divorce laws—the beneficiary form controls regardless of your divorce decree.

A few states enacted laws voiding ex-spouse designations upon divorce finalization, but these state laws typically don't affect federally-regulated ERISA accounts. The U.S. Supreme Court consistently holds that valid beneficiary designation forms control, regardless of subsequent divorce or contradictory will provisions.

Making beneficiary choices that trigger unnecessary taxes wastes tens or hundreds of thousands of dollars. For instance, naming a trust as IRA beneficiary can work beautifully, but only when the trust satisfies specific IRS requirements. A non-qualifying trust might accelerate required distributions and generate higher tax bills.

Similarly, making your estate the life insurance beneficiary can subject proceeds to estate taxation when proper planning would have avoided it. Leaving taxable investment accounts to charity while naming individuals as retirement account beneficiaries reverses the optimal tax sequence.

Writing vague descriptions rather than specific identifying information creates disputes. Designations reading "my children" appear straightforward until questions emerge. Does this include stepchildren? Adopted children? Kids born after you signed the form? Provide full legal names and clarifying language when necessary, such as "all children born to or adopted by me, whenever born or adopted."

Botching the percentage calculations occurs surprisingly often. Three beneficiaries at 33% each leaves 1% unaccounted for. Rounding creates arguments. Always verify your percentages total precisely 100%, using decimals where needed (33.33%, 33.33%, 33.34%).

Naming minor children as direct beneficiaries requires court intervention. Courts appoint guardians to control assets for minors, consuming thousands in legal costs and requiring ongoing court supervision. Additionally, when your child reaches 18 or 21 (depending on your state), they receive the entire balance immediately with zero restrictions. Most 18-year-olds lack the judgment to manage substantial inheritances responsibly.

Frequently Asked Questions About Estate Planning Beneficiaries

Beneficiary designations rank among estate planning's most effective tools. They accomplish fast asset transfers, eliminate probate delays and expenses, and offer flexibility impossible to achieve through wills alone. But this same power becomes dangerous when designations remain outdated, incomplete, or inconsistent with your broader estate goals.

Review your beneficiary designations today. Gather statements from all retirement accounts, insurance policies, and bank accounts. Verify the names shown match your current intentions. Confirm percentages add to exactly 100%. Check that you've designated contingent beneficiaries. Look for accounts still listing an ex-spouse, deceased individual, or minor child as direct recipient.

Fix any problems immediately. Contact each institution, obtain current change forms, and submit corrected designations. This straightforward task—updating a handful of forms—prevents enormous problems for your loved ones and ensures your assets actually reach your intended recipients.

For complicated situations involving disabled beneficiaries, blended families, or significant assets, consult an estate planning attorney to coordinate beneficiary designations with trusts, wills, and tax reduction strategies. Professional guidance costs far less than the expensive mistakes and family conflicts it prevents.

Your beneficiary designations will ultimately control where hundreds of thousands or millions of dollars flow. Give them the careful attention they deserve.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.