Estate planning documents organized on a desk with laptop and paperwork

Simple Estate Planning Worksheet Guide

Getting your estate in order starts with knowing what you actually own. You don't need expensive software or a law degree—just a clear system for tracking your assets, debts, and wishes. Most people avoid this task because it seems overwhelming, but breaking it into manageable pieces makes the whole process surprisingly straightforward.

What Is an Estate Planning Worksheet?

Picture a roadmap that shows everything you own, everything you owe, and everyone who matters in your financial life. That's essentially what this worksheet does.

It's your personal financial snapshot—a collection point for asset details, account numbers, insurance policies, and all those passwords you've stored in seventeen different places. Unlike your will or trust documents, this worksheet doesn't carry any legal weight. You can't just write "cousin Mike gets the beach house" on a worksheet and call it done.

What it does do is give your estate attorney the information they need without playing twenty questions during expensive consultations. One client recently told me she saved $800 in legal fees because she showed up to her first meeting with every account number, property deed, and beneficiary designation already documented.

Here's the practical benefit: when you pass away, your executor isn't frantically searching through desk drawers, old emails, and safe deposit boxes trying to piece together your financial life. They'll have a blueprint. Some families spend six months just tracking down all the accounts—yours won't.

The worksheet evolves with your life. Bought a rental property? Add it. Paid off your mortgage? Update it. Got divorced? Definitely change it. Think of it less like a document and more like your financial diary that someone else will need to read someday.

Author: Jonathan Whitmore;

Source: harbormall.net

What to Include in Your Estate Planning Worksheet

Personal Information and Family Details

You'll want full legal names here—not nicknames or what everyone calls Uncle Bob. Include Social Security numbers, birth dates, and current addresses for yourself, your spouse, and your kids (biological, adopted, step—anyone who factors into your estate).

Your parents and siblings should make the list even if they won't inherit anything. Your executor might need to notify them or ask questions about family history. Same goes for an ex-spouse if you share children or have ongoing financial ties.

Write down contact information for your CPA, financial advisor, insurance agent, and attorney. These professionals hold pieces of your financial puzzle, and your executor will need to reach them. I've seen executors waste weeks trying to find out who handled someone's taxes or where they bought life insurance.

Asset Inventory and Property Lists

Start with real property—your house, that cabin up north, the duplex you rent out, or the undeveloped land you bought as an investment. For each one, document the street address, what you think it's worth, what you still owe on it, and how the title reads. Is it just your name? Joint with your spouse? Held in a trust?

Your financial accounts need their own detailed section. Every checking account, savings account, brokerage account, 401(k), IRA, Roth IRA, pension, and health savings account should appear here. Write down where it's held, the full account number, and roughly how much sits in it. Don't forget those online-only banks that never send paper statements.

Valuable personal items deserve attention too—cars, boats, jewelry worth more than a few thousand dollars, art collections, antiques, guns, musical instruments. You're not inventorying your silverware drawer, just things that matter financially or might cause family arguments. One family nearly came to blows over a $300 quilt that had sentimental value, while nobody cared about the $15,000 coin collection because they didn't know it existed.

If you own part of a business, document your ownership percentage and locate any partnership agreements or buy-sell agreements. These contracts often dictate what happens to your share when you die, sometimes overriding what your will says.

Author: Jonathan Whitmore;

Source: harbormall.net

Debts, Liabilities, and Financial Obligations

What you owe matters as much as what you own. Your mortgage, car payments, credit cards, student loans, and personal loans all get settled from your estate before anyone inherits a dime.

Include debts that might not be obvious—that $5,000 you borrowed from your brother to fix the roof, the medical bills you're paying off monthly, or your parent's assisted living expenses you've been covering. These informal obligations often slip through the cracks but can create serious family tension if forgotten.

Did you co-sign a loan for anyone? That's a potential liability. Guarantees on business loans or leases? Those too. Your estate could be on the hook even after you're gone.

Beneficiary Designations and Distribution Wishes

Here's where people discover problems they didn't know existed. Life insurance, retirement accounts, and payable-on-death bank accounts transfer directly to named beneficiaries—your will doesn't control them.

Pull out those beneficiary designation forms and actually look at them. Is your ex-husband still listed on that old 401(k)? Is your deceased mother the beneficiary on your life insurance? I've seen both situations play out badly. The designation form always wins against your will, so an outdated beneficiary gets the money even if you meant it for someone else.

Write down who you'd like to receive specific items. Maybe your daughter collects cookbooks and should get Grandma's recipe collection. Perhaps your son who helped you through surgery deserves a larger portion. These notes help your attorney draft documents that actually reflect your thinking.

Important Documents and Their Locations

Your executor can't use documents they can't locate. Note exactly where someone would find your original will, trust papers, powers of attorney, healthcare directive, and living will. "In the filing cabinet" isn't specific enough—which filing cabinet, which drawer, which folder?

Digital assets create new challenges. Your email accounts, social media, photo storage, cryptocurrency wallets, online businesses, and subscription services all need documentation. Some people keep this section separate for security reasons—maybe stored in a password manager with emergency access granted to their executor.

Property titles, insurance policies, the last seven years of tax returns, military discharge papers if you served—track down where physical copies live. Marriage licenses, divorce decrees, prenuptial agreements, and birth certificates matter for estate settlement too.

How to Fill Out an Estate Planning Worksheet

Begin with information already in your head: everyone's names, birthdates, your address. Easy stuff builds confidence before tackling harder sections.

Next, collect recent statements from banks, brokerages, and retirement accounts. January year-end summaries work perfectly because they show balances and list beneficiaries. Missing statements? Request them now—you need current information anyway for attorney meetings.

Set aside an afternoon. Three or four hours gives you enough time to make real progress without burning out. You won't finish everything today, and that's fine. Mark sections "need to research" and circle back after tracking down missing details.

Don't write vague descriptions. "Checking account" doesn't help anyone. "Chase Bank checking account #123456789" actually works. Round values to the nearest thousand—$47,832 can be $48,000. Precision doesn't matter since you'll update these numbers regularly.

Photograph valuable personal property. Which diamond ring? Which antique desk? Pictures eliminate confusion when you own multiples.

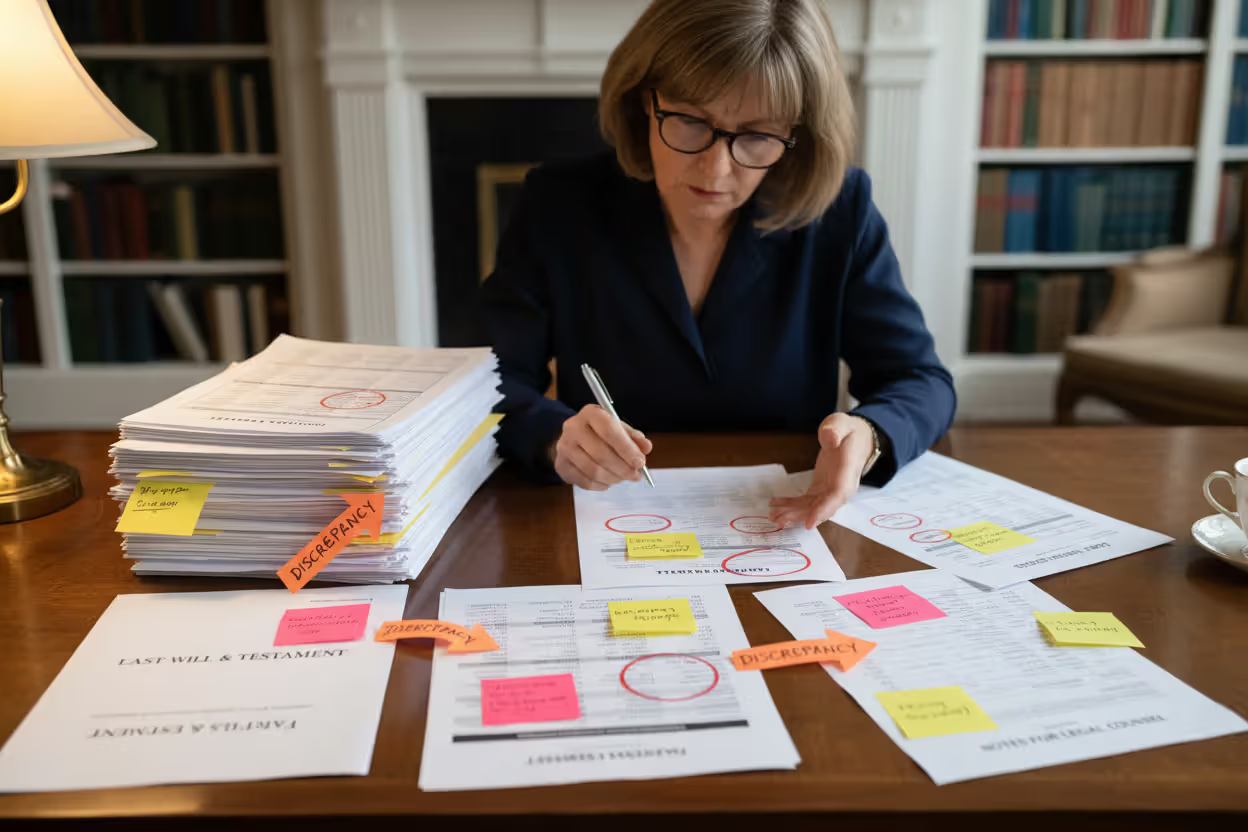

If you have existing estate documents, read them while completing your worksheet. You might discover your will mentions the beach condo you sold five years ago or still uses your maiden name. Flag these inconsistencies for your attorney.

Author: Jonathan Whitmore;

Source: harbormall.net

Free Estate Planning Worksheet Templates

PDF versions work beautifully if you prefer printing and handwriting, then filing the physical pages with other important papers. Many PDFs include helpful examples and prompts for each section.

Spreadsheet templates—Excel or Google Sheets—suit people with lots of accounts or complicated finances. You can add rows easily, calculate totals automatically, and sort by category. Updates happen without rewriting everything. Change an account balance or beneficiary designation in seconds.

Printable templates split the difference: handwrite your initial draft while thinking through decisions, then type a clean version later.

Look for templates covering all major categories without drowning you in questions about dynasty trusts and charitable remainder annuities unless you actually need that complexity. Simple beats comprehensive if comprehensive means you'll never finish.

Estate planning attorneys often offer free worksheet downloads on their websites. These align with information they need for consultations, streamlining the eventual document preparation process.

Your state bar association might provide worksheets addressing local laws. While most asset information stays consistent everywhere, community property states (like California, Texas, and Arizona) handle marital assets differently than common law states.

Author: Jonathan Whitmore;

Source: harbormall.net

When to Update Your Estate Planning Worksheets

Marriage changes everything—beneficiaries, asset ownership, the works. So does divorce. Update immediately after either.

A new baby or adopted child requires updating distribution plans and guardian designations. Death of someone named as beneficiary, executor, or trustee means choosing replacements.

Big financial shifts matter: inherited money, sold your business, bought investment property, paid off major debt. When your net worth jumps significantly, basic strategies might not protect you adequately anymore.

Review annually even when life stays stable. Account balances shift, you open new accounts and forget to document them, or you change your mind about who gets what. Set a phone reminder for the same date yearly—maybe your birthday or January 1st.

Every three to five years, audit thoroughly by comparing your worksheet against actual statements. This deeper dive catches things quick reviews miss. Takes longer but ensures accuracy.

Common Mistakes When Using Estate Planning Worksheets

Most people underestimate how much time their loved ones will spend searching for accounts and documents after they're gone. A well-maintained asset inventory isn't just about organization—it's an act of love that spares your family unnecessary stress during an already difficult time

— Patricia Chen

Insufficient detail tops the list. "Checking account at First National Bank" doesn't help when you have four accounts there. Account numbers matter. Enough specifics that a stranger could locate each asset—that's the goal.

Documenting updated beneficiaries on your worksheet while forgetting to actually change them with the financial institution creates disasters. Your worksheet might say "cousin Sarah gets my IRA" but if the IRA still lists your ex-wife, she's getting that money. The institution's records override everything else.

Digital assets get skipped constantly. Cryptocurrency, online businesses, domain names, valuable social media accounts might represent serious money but go undocumented. Your executor won't know to look for things they don't know exist.

Not telling your executor where you keep this information makes the whole exercise pointless. Finished worksheet hidden in a safe nobody knows about? Useless. Tell them where to look and how to access any password protection.

Treating this as a one-time project guarantees obsolete information. Complete a thorough worksheet, then ignore it for ten years? Half that information will be wrong.

Some folks think completing the worksheet means they're done with estate planning. Wrong. This organizes information—you still need properly executed legal documents like wills, trusts, and powers of attorney to implement your plan.

Estate Planning Worksheet Components Comparison

| Component | Basic Version | Comprehensive Version | Who Needs It |

| Personal Information | Immediate family names, birthdates, Social Security numbers | Extended relatives, all professional advisors, medical providers, ex-spouses | Basic: Single people with straightforward families; Comprehensive: Blended families or complex relationships |

| Real Estate | Home address and estimated value | All properties including purchase dates, original cost, mortgage information, rental income details | Basic: Own one house; Comprehensive: Multiple properties or investment real estate |

| Financial Accounts | Institution names and account types | Full account numbers, current beneficiaries, original contribution amounts, transaction history | Basic: Few accounts, modest balances; Comprehensive: Substantial wealth across many institutions |

| Business Interests | Company name and your ownership stake | Operating agreements, succession planning documents, recent valuation reports, buy-sell terms | Basic: Own shares passively; Comprehensive: Actively run a business or hold significant equity |

| Personal Property | Items worth over $5,000 | Complete inventory with photographs, professional appraisals, specific recipient wishes | Basic: Typical household belongings; Comprehensive: Valuable collections, heirlooms, or specialty items |

| Digital Assets | Email and major online accounts | Cryptocurrency holdings, domain portfolios, digital businesses, content with residual income | Basic: Average internet user; Comprehensive: Digital entrepreneurs or cryptocurrency investors |

| Debts | Mortgages and major loans | Every obligation including co-signed loans, tax liens, business guarantees, informal debts | Basic: Straightforward debt; Comprehensive: Complex obligations or multiple creditors |

Frequently Asked Questions About Estate Planning Worksheets

Getting your estate planning worksheet finished is the critical first step toward protecting what you've built and making things easier for the people you love. Yes, it requires focused time and attention to details. But the clarity and peace of mind you'll gain makes every minute worthwhile.

Download a template that matches your situation this week. Simple finances? Basic template. Multiple properties or business ownership? Comprehensive version. Block out a few hours to complete sections you can handle immediately, then schedule time to gather missing information.

This worksheet serves your family, not some abstract ideal of perfection. Pick a format you'll actually keep current rather than the most elaborate option available. A simple worksheet you update regularly beats an incredibly detailed version you complete once and abandon.

Tell your designated executor where you've stored the completed worksheet and sit down together to walk through it. Yes, that conversation feels awkward. Do it anyway. It prevents confusion and arguments when your family needs clarity most urgently.

Your worksheet works alongside professional legal advice—it doesn't substitute for it. Once you've organized everything, schedule a consultation with an estate planning attorney to create the legal documents that will implement your wishes. You'll find the process smoother, quicker, and less expensive when you show up prepared with a finished worksheet.

The perfect time to organize your estate information was five years ago. The next best time? Today. Right now. This afternoon works.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.