Estate planning documents on a desk with house keys and a bank card

state Planning Forms Guide for US Residents

If you died tomorrow, who'd get your house? Your bank accounts? Who'd make medical decisions if you were in a coma? Without signed paperwork, judges and state formulas answer these questions—not your preferences.

Here's the reality: most people put this off. They think estate planning is for retirees with millions in the bank. Wrong. Got a car? A savings account? Kids? Strong opinions about being on life support? You need these documents. I'm talking about the paperwork that controls what happens when you can't speak for yourself.

The upside? Basic forms aren't complicated. You don't need a law degree. The downside? Mess up the signatures or use the wrong state's version, and your carefully written wishes become worthless paper. Let me walk you through what you actually need, where to get it, and how to avoid the mistakes that invalidate everything.

What Are Estate Planning Forms

Think of estate planning forms as your instruction manual for other people. When you're gone or incapacitated, these documents tell everyone—family, doctors, banks, courts—exactly what to do.

Author: Caroline Ellsworth;

Source: harbormall.net

You've probably heard of wills. That's just one piece. A complete set includes your will, maybe a trust if you want to skip probate, powers of attorney for financial stuff, healthcare directives for medical decisions, and HIPAA releases so your chosen person can actually talk to your doctors. Depending on your situation, you might add guardianship papers for young kids, special trusts for pets, or deeds that transfer property automatically.

Each document does something specific. Your will instructs the probate court on dividing your belongings. A financial power of attorney lets someone pay your mortgage if you're unconscious after a car accident. Healthcare directives tell ER doctors whether to intubate you. Beneficiary forms on your 401(k) send that money directly to whoever you named, bypassing everything else.

Here's what makes them legally binding: your state has rules. Two witnesses watching you sign? Required for wills in every state. Notary stamp? Mandatory for powers of attorney almost everywhere. Miss these requirements, and that document you spent hours completing becomes legally meaningless. Courts won't honor it. Banks won't accept it. Your family ends up in legal limbo while lawyers sort out the mess at $400 per hour.

A properly signed will stops your siblings from fighting in court over your stuff. Financial powers of attorney prevent utility companies from shutting off services while you recover from surgery. Skip these steps, and courts appoint random strangers as conservators to manage your money and make your medical choices.

Types of Estate Planning Document Forms You Need

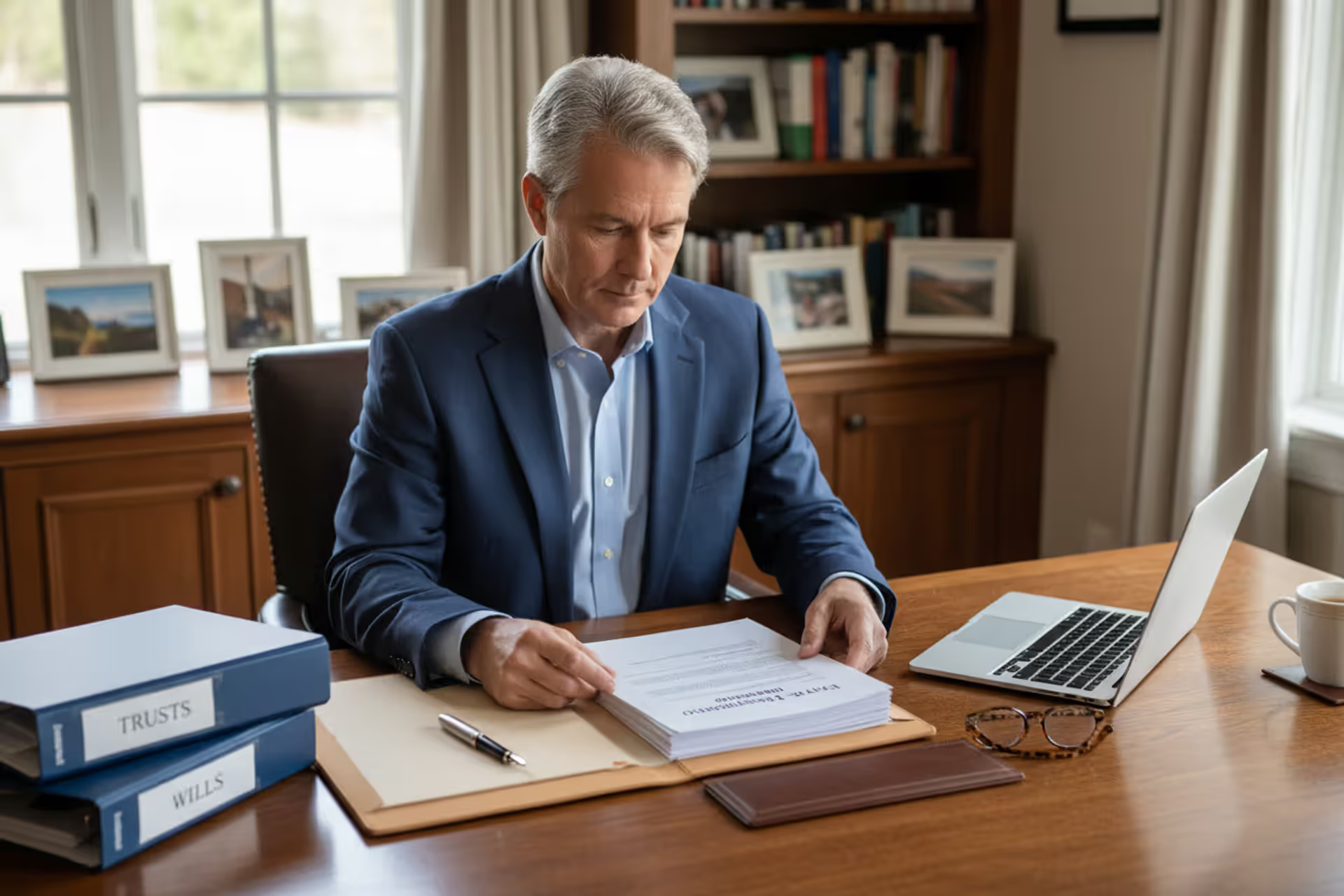

Wills and Trusts

Your last will and testament names three critical things: an executor to handle everything after you die, beneficiaries who inherit your assets, and guardians for any minor kids. Every will goes through probate—that's the court process where a judge validates your will and supervises distribution. For straightforward situations (married couple leaving everything to each other, then to adult children), a simple will does the job.

Author: Caroline Ellsworth;

Source: harbormall.net

Revocable living trusts let you avoid probate completely. Here's how they work: you create the trust, transfer your assets into it, run it yourself while you're alive, and name someone to take over when you die. Your successor trustee distributes everything according to your instructions without court involvement. Trusts cost more upfront—expect $2,000-$4,000 versus $500-$1,500 for a will—but they save time and money later. Plus they're private (wills become public court records), and you control exactly when beneficiaries get money.

Who needs trusts? Anyone owning property in multiple states definitely does—otherwise your family probates separate estates in each state. Blended families benefit because trusts let you provide for a current spouse while protecting inheritance for kids from your first marriage. Estates worth more than half a million usually justify the cost.

Testamentary trusts live inside your will and activate after death. They're perfect for leaving money to teenagers—you can specify they get 25% at age 25, another 25% at 30, and the rest at 35. Cheaper than living trusts but still go through probate.

Power of Attorney Documents

A financial power of attorney hands someone authority over your money and property when you can't handle it yourself. We're talking bank accounts, investment accounts, tax filings, bill payments, even selling your house if necessary. The "durable" version—and you definitely want durable—stays effective if you become incapacitated. That's literally the only time you need it.

Without this document, what happens? Your spouse or kids petition the court for conservatorship. That process takes months, costs several thousand dollars, and requires ongoing court supervision with annual accountings. Meanwhile, your mortgage goes unpaid and your credit tanks.

You can make these as broad or narrow as you want. Limited POAs work for specific situations—like authorizing your sister to close on selling your condo while you're deployed overseas. General POAs cover everything financial. Some people choose "springing" powers that don't activate until a doctor certifies you're incapacitated, but banks often hassle your agent demanding proof, which delays everything when speed matters. Most attorneys recommend POAs that take effect immediately, trusting your chosen person to only use them when needed.

Healthcare Directives

A healthcare power of attorney (some states call it a healthcare proxy or medical POA) designates your medical decision-maker. When you're unconscious or mentally incapable, this person talks to specialists, weighs treatment options, and chooses your care based on what you would've wanted. The form usually includes HIPAA authorization because otherwise, privacy laws prevent doctors from discussing your condition with anyone.

Living wills address end-of-life scenarios specifically: ventilators, feeding tubes, CPR, organ donation. Do you want extreme measures if you're in a permanent vegetative state? This document spells it out, removing impossible decisions from your family during traumatic moments. My grandmother didn't have one—watching my mom and uncles argue in a hospital hallway about withdrawing life support was brutal and could've been prevented with one simple form.

Some states combine healthcare POA and living wills into a single advance directive. Others separate them. Check what your state uses.

POLST forms (Physician Orders for Life-Sustaining Treatment) are different—they're signed medical orders, not just preferences. Your doctor completes them with you. They're bright pink or orange, designed to be visible in emergencies, and they travel with you between facilities. EMTs and ER staff follow POLST orders immediately. These are crucial for anyone with serious illness or in nursing homes.

Author: Caroline Ellsworth;

Source: harbormall.net

Beneficiary Designation Forms

This trips people up constantly. Your 401(k), IRA, life insurance, and payable-on-death accounts transfer according to beneficiary forms filed with those companies—NOT your will. Your will could say "everything goes to my daughter," but if your ex-husband is still named on your $500,000 life insurance policy, he gets that money. Beneficiary designations override wills, period.

I've seen this disaster play out: guy remarries, writes a new will leaving everything to his second wife, but never updates his retirement account beneficiary forms. Dies suddenly at 58. His first wife, who he divorced 15 years earlier, collects the entire $800,000 IRA. His widow was stuck with just the house.

Check these forms every two years minimum. After any marriage, divorce, birth, or death, update them immediately. Always name contingent (backup) beneficiaries in case your primary dies first. For large accounts, talk to an estate attorney about whether naming a trust as beneficiary makes sense for creditor protection or controlling distribution.

How to Get Estate Planning Forms Online

Start with your state bar association's website. Most offer free downloadable forms for basic wills, POAs, and healthcare directives that meet your state's current legal requirements. They include instructions written in actual English. County court websites sometimes have forms too, especially for probate-related documents.

Online legal services—LegalZoom, Rocket Lawyer, Nolo, Trust & Will—sell packages from $100 to $500. You answer interview questions, they generate customized documents. The better ones update their forms when laws change and offer attorney review add-ons for $200-$300 more. Quality varies wildly. Some provide excellent guidance and current forms. Others use outdated templates that miss recent law changes.

Free templates from random websites? Dangerous. I've reviewed forms people printed from generic legal sites that were seven years old, using language no longer valid under current statutes. One guy had a California POA form that lacked the required statutory warnings added in 2020—every bank rejected it. Another used a will template that didn't meet witness requirements in her state.

Location matters tremendously. California's will-signing rules differ from Texas's. Florida's POA statute requires specific language that Georgia doesn't. A New York healthcare proxy won't necessarily work in Arizona. Grab the wrong state's form, and you've wasted your time creating legally useless documents.

Middle-ground option: prepare documents using reputable online services, then pay an attorney $200-$400 for limited review. They'll check for errors, suggest improvements, and confirm everything meets legal requirements. Works great for straightforward situations where you're comfortable doing the work but want professional verification before signing.

Author: Caroline Ellsworth;

Source: harbormall.net

State Requirements for Estate Planning Forms

Estate planning documents must follow the laws where you live—and where you own property. Rules change significantly across state lines, especially regarding witnesses, notaries, and filing.

Every state requires witnesses for wills, but the number varies. Most want two witnesses who watch you sign, then add their own signatures. Vermont insists on three. Witnesses generally can't be people who inherit under your will—if they are, their gifts usually get voided. Many states allow "self-proving" wills with notarized affidavits from witnesses attached. These speed up probate years later because courts don't need to track down witnesses to verify signatures.

Powers of attorney have become more regulated recently. States now mandate specific statutory warnings, disclosures about agent duties, and sometimes separate signature pages where agents acknowledge their responsibilities. Notarization is legally required in most states, and even where it's technically optional, financial institutions refuse POAs without notary stamps.

Healthcare directives vary in format across the country. Some states use combined advance directive forms including both healthcare proxy and living will. Others keep them separate. Witness requirements differ—certain states allow relatives to witness, others prohibit it to prevent conflicts of interest. A handful require notarization instead of witnesses.

| State | Will Witnesses | Will Notary | POA Notary | Healthcare Directive Witnesses | Healthcare Directive Notary |

| California | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses OR notary | Acceptable alternative |

| Florida | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| Texas | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| New York | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| Illinois | 2 required | Optional for self-proving | Yes, mandatory | 1 witness required | No |

| Pennsylvania | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| Ohio | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses OR notary | Acceptable alternative |

| Georgia | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| North Carolina | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

| Michigan | 2 required | Optional for self-proving | Yes, mandatory | 2 witnesses required | No |

Filing requirements also differ. Most states don't make you file wills before death, though some courts accept them for safekeeping. POAs for real estate deals often need recording with your county recorder's office. Healthcare directives should go to your doctors and hospitals but aren't government-filed.

When to Use DIY Forms vs. Hiring an Attorney

DIY forms work fine for straightforward situations. Single person or married couple leaving everything to each other, then splitting equally among adult children? Total assets under $300,000? Property in just one state? No complicated family drama? Quality online forms probably handle it.

Several situations scream "get a lawyer":

Blended families get messy. You've got kids from your first marriage, your spouse has kids from theirs, and you have one together. Balancing everyone's interests while ensuring your spouse is provided for but your biological kids eventually inherit requires sophisticated planning.

Business owners need succession plans, buy-sell agreements, and tax strategies. Your $2 million company won't smoothly transition with a basic will.

Large estates face taxes. Federal estate tax hits estates exceeding $13.61 million in 2024 (dropping to about $7 million in 2026). Some states tax estates worth much less—Oregon starts at $1 million. Tax planning requires attorney expertise.

Special needs beneficiaries can't just inherit money outright—they'd lose SSI and Medicaid eligibility. Special needs trusts preserve government benefits while providing supplemental funds. Only attorneys familiar with this specialized area should draft them.

Multiple real estate properties across state lines create probate nightmares. One probate proceeding per state gets expensive fast. Trusts solve this, but they must be correctly drafted and funded.

Minor children receiving substantial inheritances need testamentary trusts with age-based distributions. Should your 16-year-old get $500,000 when you die? Probably not. A trust releasing 25% at age 25, 35, and 45 protects immature spending.

Expecting challenges? Maybe you're disinheriting a child or making unequal distributions. Attorney-prepared documents with detailed capacity assessments and videotaped signings withstand legal contests better than DIY forms.

Cost comparison: DIY packages run $100-$300. Attorney-prepared simple wills cost $500-$2,000 depending on your area. Complete estate plans with trusts, all POAs, and healthcare directives run $2,000-$5,000 from attorneys, versus $300-$800 online.

The calculation is risk versus expense. That $200 online will works perfectly until it doesn't—and problems only emerge after you're dead and can't fix them. Ambiguous language, missing signatures, or overlooked provisions cost your beneficiaries thousands in legal bills and months of delays. For estates under $100,000 with simple wishes, the risk is minimal. For $500,000+ or complicated families, attorney fees are insurance against expensive mistakes.

Hybrid approach: use online services for document preparation, pay an attorney for limited review. Total cost $500-$1,000. You save money on drafting while getting professional error-checking.

Author: Caroline Ellsworth;

Source: harbormall.net

Common Mistakes When Completing Estate Planning Forms

Improper execution kills otherwise perfect documents. Wills require witnesses physically present while you sign, who then add their signatures. Having witnesses sign in the kitchen while you sign in the bedroom? Invalid in most states. Witnesses signing Tuesday when you signed Monday? Nope. Using your daughter as a witness when she inherits under the will? She might forfeit her inheritance. Skipping notarization on your POA? Banks will refuse it.

Outdated forms create disasters. Estate planning laws change constantly. A 2015 POA form might lack statutory language your state added in 2019. Healthcare directives from 2018 may not address pandemic visitor restrictions. Tax laws affecting estate planning change every few years. Always verify you're using current-year forms from reliable sources.

Life changes, documents don't. This is incredibly common. Someone writes a will at 30, gets divorced at 35, remarries at 40, has two more kids by 45—and dies at 50 with that original will still naming their ex-spouse as executor. Or parents name their brother as POA agent, he moves to Australia, they never update it, and when Dad has a stroke, the Australian brother legally controls everything from 9,000 miles away.

Major events requiring updates: getting married, getting divorced, having kids, deaths of named beneficiaries or agents, moving to a different state, major asset changes (buying/selling real estate, starting businesses, receiving inheritances).

Trusts without assets are useless. People pay attorneys $3,000 for revocable living trusts, then never transfer their bank accounts, investment accounts, or house deeds into the trust name. The trust controls nothing because it owns nothing. Everything still goes through probate. Asset funding is the crucial second step most people skip.

Vague wording causes family fights. "Split my personal property fairly among my kids" sounds reasonable until your three children spend weeks arguing over who gets mom's engagement ring and dad's coin collection. Specific bequests prevent battles: "My diamond engagement ring goes to Sarah. My coin collection goes to Michael. My china goes to Jennifer." Then a residuary clause divides everything else.

Digital assets get forgotten. Passwords for email, social media, financial sites, cloud storage, cryptocurrency wallets—none of it is accessible after death unless you've documented it. Some states now allow digital asset instructions in POAs and wills.

Single points of failure are risky. Naming only your spouse as POA agent with no backup means if you're both in the same car accident, nobody can access your accounts. Always name successor agents for POAs and healthcare proxies. Wills need backup executors and alternate guardians.

The most expensive estate plan is the one you never complete. I've seen families spend tens of thousands fighting over estates in probate court that could've been settled with $500 worth of properly signed documents. Perfection isn't the goal—having something legally valid in place and keeping it updated as your life evolves is what actually protects people

— Michael Torres

Frequently Asked Questions About Estate Planning Forms

Estate planning forms protect everything you've worked for and guarantee your preferences are followed when you can't voice them anymore. The core documents—wills, powers of attorney, healthcare directives—are available to everyone, not just wealthy retirees. Starting with basic forms beats having nothing at all, even if your estate plan becomes more sophisticated later.

Success requires understanding which forms you actually need, finding legitimate state-specific versions, and executing them according to your state's rules. Straightforward estates often work fine with quality online forms. Complicated situations justify attorney guidance. Preparing documents yourself with limited attorney review for $500-$1,000 total splits the difference—you save money while getting professional oversight.

Common errors destroy planning: improper signature procedures, outdated templates, forgetting to update after marriages or divorces. These mistakes invalidate your documents and dump family members into legal chaos. Spending time to complete forms correctly, getting proper witnesses and notarization, and reviewing everything every few years prevents these problems.

The best estate plan is the one that's actually completed and kept current. Whether you use free bar association forms, online services, or hire an attorney, taking action now gives you control over your legacy and spares your loved ones unnecessary legal battles and expenses during already painful times.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.