Aerial view of a residential neighborhood with several houses and legal documents with a pen on a wooden desk in the foreground

Estate Planning for Real Estate Investors Guide

Real estate portfolios require fundamentally different estate planning approaches than stock certificates or bank accounts. A single rental property generates ongoing tenant relationships, maintenance obligations, and cash flow that must continue seamlessly—even after you're gone. Multiply that complexity across multiple properties in different states, and the stakes become clear: without proper planning, your heirs may face probate in multiple jurisdictions, tax bills that force property sales, and operational chaos that destroys the value you spent years building.

Why Real Estate Investors Need Specialized Estate Planning

Traditional estate planning assumes liquid, easily divisible assets. Real estate defies these assumptions at every turn.

Properties cannot be split like mutual fund shares. If you own three rental houses and have four children, someone gets left out—or worse, siblings become unwilling co-owners locked in disputes about whether to sell or hold. Meanwhile, tenants need to know where to send rent checks, contractors require authorization for emergency repairs, and property managers must answer to someone with legal authority.

Multi-state property ownership creates particularly thorny problems. Each state where you own real estate can require separate probate proceedings. A Florida resident who owns rental properties in Ohio and Arizona might subject their heirs to three simultaneous probate processes, each governed by different state laws and timelines. Probate typically takes 9-18 months per state and consumes 3-7% of property value in legal fees and court costs.

The tax landscape adds another layer of complexity. Real estate investors often carry significant depreciation recapture liability—taxes owed on the depreciation deductions claimed over years of ownership. Without planning, this tax bomb detonates precisely when heirs are least prepared to handle it. Properties held in the wrong ownership structure may lose the stepped-up basis benefit that could eliminate capital gains taxes entirely.

Operational continuity matters more than most investors realize. When a landlord dies unexpectedly, bank accounts freeze, preventing payment of mortgages, insurance, and utilities. Property management agreements may terminate automatically. Tenants withhold rent, unsure who has legal authority to collect it. A portfolio generating $15,000 monthly can hemorrhage value within weeks if succession planning fails.

Author: Caroline Ellsworth;

Source: harbormall.net

Common Estate Planning Structures for Investment Properties

The right ownership structure serves dual purposes: managing properties during your lifetime and transferring them efficiently at death. Each vehicle offers distinct trade-offs between control, tax benefits, asset protection, and complexity.

Revocable vs. Irrevocable Trusts for Real Estate

Revocable living trusts function as the workhorse of real estate estate planning. You transfer property titles into the trust, name yourself as trustee during your lifetime, and designate successor trustees to take over seamlessly when you die or become incapacitated. The trust agreement specifies exactly how properties should be managed and distributed, bypassing probate entirely.

The revocable structure preserves complete flexibility—you can sell properties, refinance mortgages, or dissolve the trust whenever you choose. For tax purposes, the IRS ignores revocable trusts completely; you report all income and deductions on your personal return as if you still owned properties directly. This simplicity comes with a drawback: revocable trusts offer zero asset protection from lawsuits or creditors.

Irrevocable trusts sacrifice control for protection and tax benefits. Once you transfer property into an irrevocable trust, you cannot reclaim it or modify terms without beneficiary consent. This permanence removes assets from your taxable estate, potentially saving millions in estate taxes for portfolios exceeding the federal exemption threshold (currently $13.99 million per individual in 2026). Irrevocable trusts also shield properties from personal liability—a slip-and-fall lawsuit related to your primary residence cannot touch rental properties held in a properly structured irrevocable trust.

The tax treatment differs substantially. Irrevocable trusts file separate tax returns and may pay tax at compressed trust rates, which hit the highest bracket at relatively low income levels. Sophisticated planning often combines irrevocable trusts with other structures to optimize both tax efficiency and asset protection.

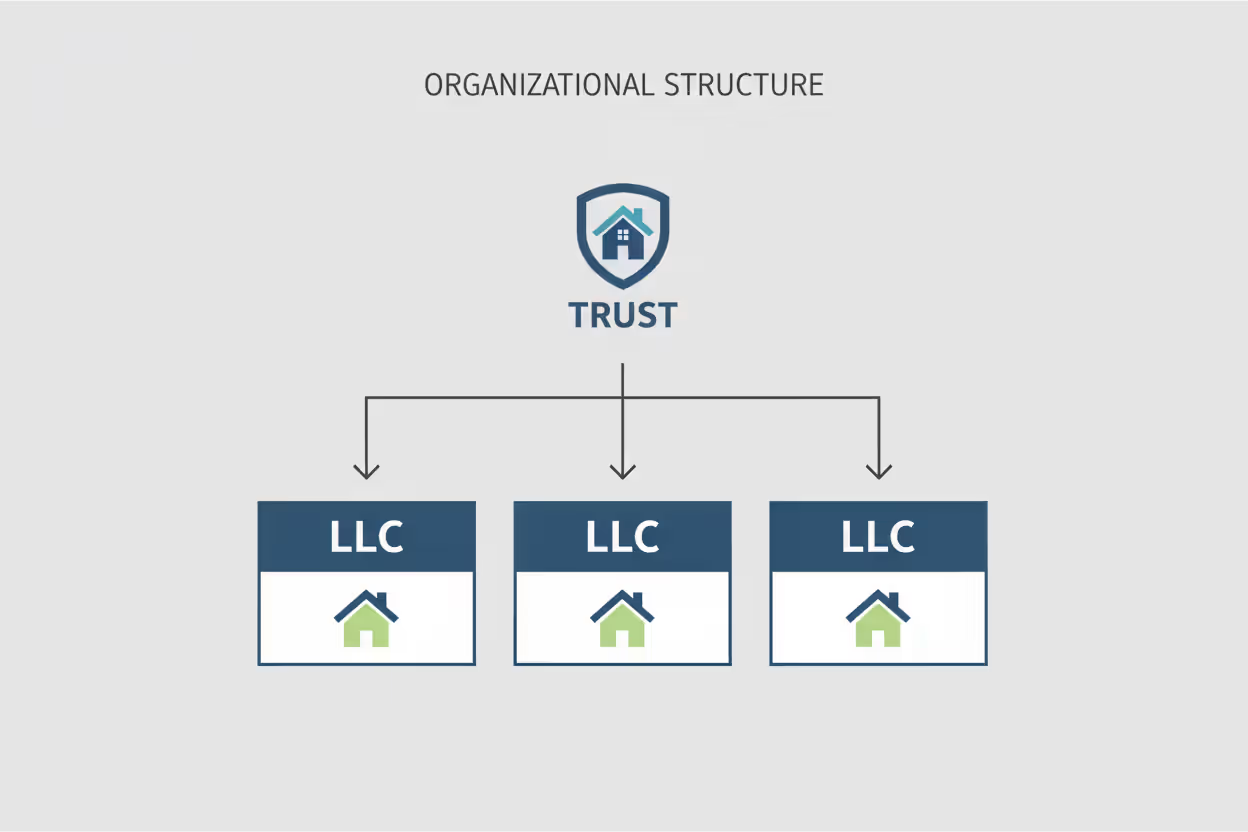

Using LLCs in Your Estate Plan

Limited liability companies provide liability protection that trusts alone cannot match. Each LLC creates a legal barrier between property-level risks (tenant injuries, environmental claims, construction defects) and your personal assets. A tenant who sues over mold exposure can only reach assets inside that specific LLC, not your other properties or personal wealth.

From an estate planning perspective, LLCs offer remarkable flexibility. You can gift LLC membership interests to children gradually over time, taking advantage of annual gift tax exclusions ($19,000 per recipient in 2026). Gifting 10% of an LLC annually to each of three children transfers the entire company over roughly three years without triggering gift taxes or consuming your lifetime exemption.

LLCs also facilitate unequal distributions while maintaining operational control. You might transfer 60% ownership to your daughter who will manage the properties while giving 20% each to two sons who prefer passive income. As the manager, your daughter controls all decisions regardless of ownership percentages. This structure prevents the deadlock that plagues joint property ownership.

The combination of LLC and trust creates powerful synergy. Form an LLC to hold properties and provide liability protection, then transfer LLC membership interests into a revocable trust to avoid probate. Your trust becomes the LLC member, gaining both probate avoidance and asset protection.

Family limited partnerships operate similarly to LLCs but offer additional valuation discount opportunities. When you gift limited partnership interests to heirs, appraisers typically apply 25-40% discounts reflecting the lack of control and marketability. These discounts let you transfer more value within gift tax limits, though the IRS scrutinizes aggressive discounting.

Author: Caroline Ellsworth;

Source: harbormall.net

Tax Planning Strategies to Preserve Your Real Estate Wealth

Tax planning for real estate investors intersects estate planning in ways that can save or cost heirs hundreds of thousands of dollars.

Stepped-up basis represents the single most valuable tax benefit in real estate estate planning. When you die owning property, your heirs receive a new tax basis equal to the fair market value on your date of death. If you purchased a rental house for $200,000 that's worth $800,000 when you die, your heirs can sell immediately and owe zero capital gains tax on the $600,000 appreciation. All accumulated depreciation recapture vanishes as well.

This benefit disappears if you gift property during your lifetime. Children who receive property as a gift inherit your original cost basis, meaning they'll pay capital gains tax on all appreciation when they eventually sell. The stepped-up basis rule creates a powerful argument for holding appreciated real estate until death rather than gifting it prematurely.

However, estate tax considerations may override capital gains planning for larger portfolios. The federal estate tax exemption stands at $13.99 million per person in 2026, but this historically high threshold may drop significantly in coming years. Estates exceeding the exemption pay 40% tax on the excess. For portfolios approaching or exceeding exemption levels, gifting property during your lifetime removes future appreciation from your taxable estate, potentially saving more in estate taxes than the lost stepped-up basis costs in capital gains.

The 1031 like-kind exchange program lets investors defer capital gains by reinvesting sale proceeds into replacement property. From an estate planning perspective, 1031 exchanges serve as a tax-deferral bridge to the stepped-up basis finish line. You can exchange properties repeatedly throughout your lifetime, deferring all gains, then die owning the final replacement property. Your heirs receive stepped-up basis on that property, permanently eliminating the deferred gains.

Installment sales to intentionally defective grantor trusts represent an advanced strategy for large portfolios. You sell property to an irrevocable trust in exchange for a promissory note, removing future appreciation from your estate while retaining a stream of interest payments. The "defective" designation means you continue paying income taxes on trust earnings—essentially making tax-free gifts to beneficiaries by paying their tax liability.

Annual gift tax exclusions provide a simple way to begin transferring wealth. You can gift $19,000 per recipient annually (or $38,000 per couple) without filing gift tax returns or consuming lifetime exemption. Gifting fractional LLC interests representing rental properties lets you transfer real estate incrementally while maintaining control through manager designation.

Author: Caroline Ellsworth;

Source: harbormall.net

Property Transfer Methods and Their Consequences

The mechanism you choose for transferring property dramatically affects timing, tax consequences, and potential complications.

Transfer-on-death deeds (available in roughly 30 states) let you designate beneficiaries who automatically inherit property when you die, similar to how bank accounts pass via payable-on-death designations. These deeds avoid probate and preserve stepped-up basis, offering simplicity for single-property transfers. However, they provide no incapacity planning, no asset protection, and no ability to specify management terms. If you become incapacitated, no one can sell or refinance the property without court-ordered guardianship.

Joint tenancy with right of survivorship automatically transfers your ownership share to the surviving co-owner at death. While this avoids probate, it creates significant risks. Adding a child as joint tenant gives them immediate ownership rights—they can force a partition sale, their creditors can place liens on the property, and their divorce might entangle your investment in their marital dissolution. Joint tenancy also causes partial loss of stepped-up basis; only your portion receives basis adjustment at death.

Life estate deeds let you retain the right to use property for life while designating "remainder" beneficiaries who inherit automatically at your death. This structure avoids probate and may provide some Medicaid planning benefits, but creates inflexibility. You cannot sell or refinance without remainder beneficiaries' consent, and they receive your original tax basis rather than stepped-up basis in some circumstances.

Quitclaim deeds transfer whatever interest you own with no warranties or guarantees. While sometimes appropriate for transfers between family members or into trusts, quitclaim deeds offer no protection and may create title insurance problems. Many investors mistakenly use quitclaim deeds when warranty deeds would be more appropriate.

Trust transfers via warranty deed provide the most comprehensive solution for most investors. Deeding property into a properly drafted trust avoids probate, preserves stepped-up basis, allows detailed management instructions, and facilitates professional trustee succession if needed. The trust can hold property indefinitely, allowing children to inherit without forced sales or partition.

Planning Succession for Rental Property Management

Real estate succession planning must address both ownership transfer and operational continuity. A perfect estate plan that transfers properties efficiently means little if the portfolio collapses from mismanagement in the interim.

Designate and train successor managers well before they're needed. If your daughter will inherit and manage properties, involve her in operations now. Grant her property manager access, include her in tenant communications, and document systems for rent collection, maintenance coordination, and vendor relationships. Knowledge transfer cannot happen posthumously.

Property management agreements should survive your death or incapacity. Review contracts to confirm they bind your successors and permit assignment. Many agreements terminate automatically upon the owner's death, leaving properties unmanaged at the worst possible moment. Amend agreements to continue under successor ownership or trustee authority.

Document standard operating procedures for everything: preferred contractors, rent collection processes, lease renewal procedures, maintenance schedules, insurance policies, and accounting systems. A comprehensive operations manual lets successors maintain continuity even if they lack your experience. Include vendor contact information, property-specific quirks (the furnace in Unit 3 requires monthly filter changes), and historical context that prevents costly mistakes.

Income distribution planning prevents family conflict. If three children inherit your four rental properties but only one manages them, how much compensation does the manager receive? Specify management fees in your trust or operating agreement—typically 8-12% of gross rents for professional management. This prevents resentment when the managing child draws income while siblings receive only their ownership share.

Unequal property division requires careful handling. Real estate cannot be divided precisely, so equal value rarely means equal property count. Consider equalizing distributions through other assets (retirement accounts, life insurance proceeds) or granting some heirs the option to buy out others at predetermined formulas. Without clear mechanisms, heirs may face forced sales or years of litigation.

Establish lines of credit or cash reserves for transition periods. When you die, properties still need mortgage payments, insurance premiums, and maintenance funding. If your estate's cash is tied up in probate, successors need access to operating capital. A business line of credit in the LLC's name, with the successor trustee as authorized signatory, ensures properties remain funded through transition.

Mistakes Real Estate Investors Make in Estate Planning

Author: Caroline Ellsworth;

Source: harbormall.net

Even sophisticated investors who carefully structure property ownership often overlook critical estate planning elements.

Failing to update beneficiary designations after major life events creates unintended consequences. Your trust may specify that properties pass to your current spouse and children, but if individual properties still list your ex-spouse as transfer-on-death beneficiary, the deed controls. Review and update all beneficiary designations every 2-3 years and after divorces, remarriages, births, or deaths.

Ignoring out-of-state properties ranks among the costliest oversights. Investors who diligently place local properties in trusts sometimes forget that Arizona rental or the Tennessee cabin, subjecting heirs to ancillary probate in each state. Every property in every state must be properly titled in your trust or LLC to avoid probate.

Treating investment properties the same as personal residences creates missed opportunities. Your primary home might appropriately sit in a revocable trust for probate avoidance, but rental properties benefit from LLC liability protection. Commingling personal and investment properties in the same legal structure dilutes asset protection and complicates tax reporting.

Failing to plan for illiquidity forces fire sales. Real estate cannot be quickly converted to cash for estate taxes, final expenses, or equalization among heirs. Investors with $5 million in property but minimal liquid assets may force heirs to sell properties at distressed prices to pay estate taxes or buy out siblings. Life insurance, cash reserves, or irrevocable life insurance trusts can provide liquidity without forced sales.

Neglecting disability planning leaves a gap that many discover too late. Estate planning addresses death, but incapacity creates equally serious problems. Without durable power of attorney and healthcare directives, no one can manage your properties if you're alive but incapacitated. Courts must appoint guardians through expensive, public proceedings. Comprehensive planning addresses both death and disability scenarios.

Overlooking the mortgage due-on-sale clause occasionally creates problems when transferring financed properties into trusts or LLCs. Federal law (Garn-St. Germain Act) generally prohibits lenders from calling loans when you transfer property into a revocable trust where you remain beneficiary, but transfers to LLCs or irrevocable trusts may technically trigger the clause. While lenders rarely enforce it if payments continue, review loan documents and consider notifying lenders of planned transfers.

The biggest mistake I see real estate investors make is treating their properties like stocks—something you can just list on a beneficiary form and forget. Real estate requires operational succession planning. Your heirs need to know who collects the rent on the first of the month, and they need that authority legally established before they need it, not six months into probate

— Michael Chen

Frequently Asked Questions About Real Estate Estate Planning

Real estate wealth compounds across generations when properly structured. The difference between a portfolio that enriches your grandchildren and one that triggers family lawsuits often comes down to planning decisions you make today.

Start by inventorying every property you own and how it's currently titled. Identify gaps: properties held in your individual name that should move into trusts or LLCs, out-of-state holdings that will trigger multiple probates, or financed properties where due-on-sale clauses might complicate transfers.

Work with professionals who understand both real estate and estate planning. A general practice attorney may miss nuances like depreciation recapture, 1031 exchange preservation, or LLC-trust integration. Similarly, a real estate attorney without estate planning expertise might overlook probate implications or tax optimization strategies.

Document your operational knowledge before it's needed. The systems in your head—which contractors to call, how you handle difficult tenants, where property-specific quirks hide—represent irreplaceable value. Capture that knowledge in writing while you can still share it.

Review and update your plan every three years or after significant life changes. Estate planning is not a one-time transaction. Tax laws change, properties appreciate, family circumstances evolve, and structures that made sense a decade ago may no longer serve your goals.

Your real estate portfolio represents years of strategic acquisitions, careful management, and patient wealth building. Proper estate planning ensures that legacy transfers intact to the people you choose, on your terms, with minimal tax erosion and maximum family harmony. The time invested in planning now multiplies across generations of benefit.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.