Top-down view of a desk with an open folder of financial documents, pen, glasses, and papers with asset growth charts, laptop in the background, warm office lighting

How to Coordinate Retirement Planning and Estate Planning

Content

Content

Retirement accounts often represent the largest financial asset most Americans own. Yet many people treat retirement planning and estate planning as separate exercises, creating gaps that can cost families thousands in taxes, trigger legal disputes, or derail legacy goals. When a 401(k) beneficiary form contradicts a will, the beneficiary form wins—regardless of what you intended. When retirement distributions and estate plans don't align, heirs may face compressed tax timelines or lose assets to probate that could have passed directly.

Coordinating these two planning areas protects your wealth, simplifies transfers, and ensures your retirement savings support the legacy you envision. This guide walks through the mechanics of aligning retirement accounts with estate goals, common pitfalls, and strategies that work in 2026.

Why Retirement and Estate Plans Need to Work Together

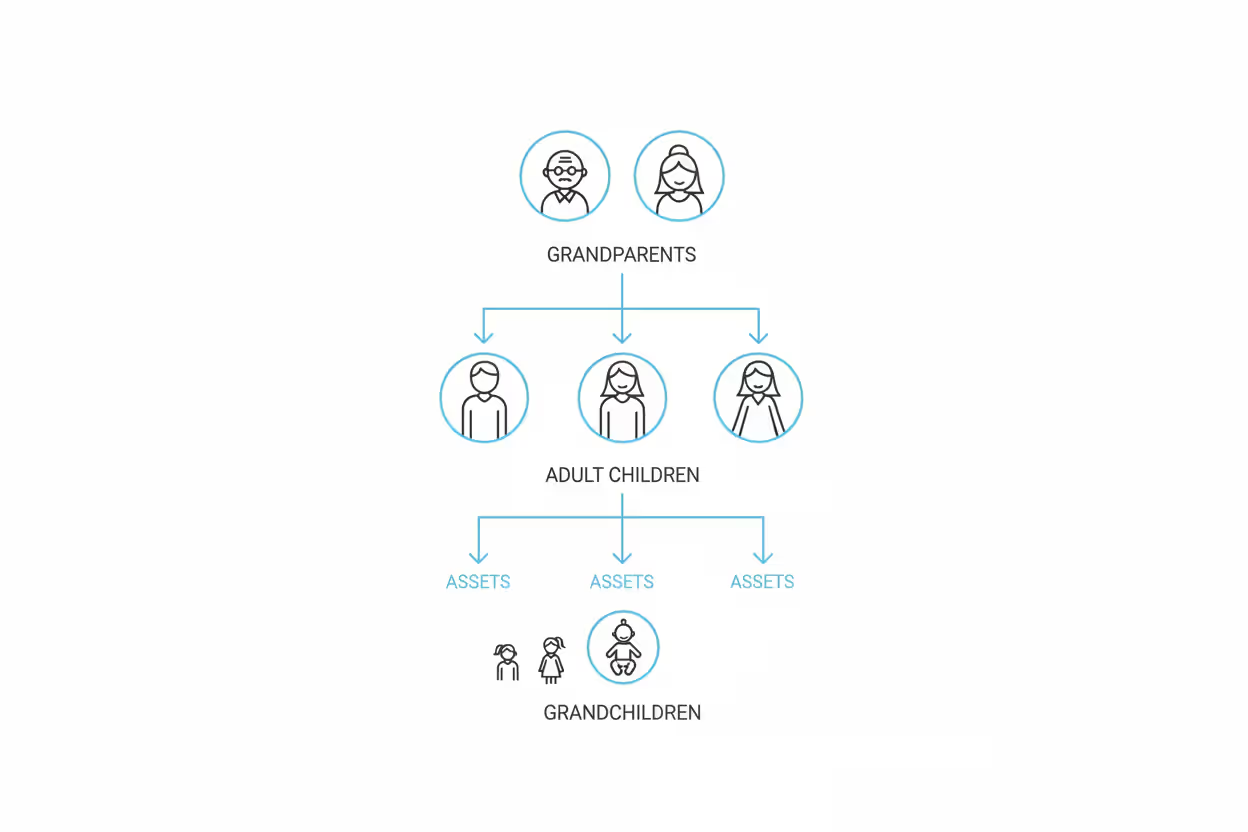

Estate and retirement planning intersect at a critical point: the transfer of wealth. Retirement accounts—IRAs, 401(k)s, 403(b)s, pensions—pass to heirs through beneficiary designations, not through your will or trust. This creates a dual-track system where one set of documents governs most assets while another set controls retirement money.

Author: Rebecca Langford;

Source: harbormall.net

Misalignment between these tracks causes predictable problems. A divorced person who remarries but never updates their 401(k) beneficiary form may inadvertently leave their largest asset to an ex-spouse. Parents who name their estate as IRA beneficiary force the account through probate, delaying distribution and potentially accelerating tax bills. Siblings who inherit an IRA without understanding the ten-year distribution rule under the SECURE Act may face surprise tax bombs.

Tax inefficiencies multiply when plans don't coordinate. Retirement accounts carry embedded income tax liability—every dollar withdrawn triggers ordinary income tax. Without coordination, high-tax-bracket heirs might inherit tax-deferred accounts while low-bracket heirs receive tax-free assets, wasting opportunities to minimize the family's overall tax burden. Estate taxes add another layer: in 2026, federal estate tax exemptions remain historically high, but some states impose estate or inheritance taxes at much lower thresholds.

Retirement estate plan coordination also matters for control and protection. Leaving an IRA outright to a young adult or someone with creditor issues offers no safeguarding. Naming a properly drafted trust as beneficiary can provide asset protection, manage distributions, and preserve eligibility for needs-based benefits—but only if the trust and beneficiary designation work in tandem.

How Retirement Accounts Affect Your Estate Plan

Retirement accounts sit outside your will. When you die, the IRA custodian or 401(k) plan administrator looks only at the beneficiary designation form on file. If that form names your sister, your sister gets the account—even if your will says everything goes to your spouse.

This beneficiary-driven transfer applies to traditional IRAs, Roth IRAs, 401(k)s, 403(b)s, SEP-IRAs, SIMPLE IRAs, and most pension plans. Annuities follow similar rules if they have a named beneficiary. These accounts bypass probate entirely when beneficiaries are properly designated, which speeds transfer and reduces administrative costs.

Common mistakes undermine this efficiency. Outdated beneficiaries top the list: people who divorced years ago, remarried, had children, or lost a named beneficiary to death but never filed updated forms. Employers and custodians don't track your life changes—you must initiate updates.

Failing to name contingent beneficiaries creates another trap. If your primary beneficiary predeceases you and no contingent is listed, the account typically passes according to the plan's default provisions—often to your estate, triggering probate and unfavorable tax treatment. Some plans default to a surviving spouse, others to children, and some to the estate regardless of family structure.

Naming your estate as beneficiary, whether intentionally or by default, forces the retirement account into probate. Probate delays access, adds legal fees, and subjects the account to creditor claims that direct beneficiary transfers would avoid. For inherited IRAs, estate beneficiaries face the least favorable distribution rules, often requiring faster withdrawals and higher taxes.

Minor children present special challenges. Most custodians won't distribute directly to minors, requiring court-appointed guardianship or custodianship. Without planning, a judge may control how and when your child accesses the money until age 18 or 21, depending on state law.

Key Steps for Integrating Retirement and Estate Planning

Start by inventorying every retirement account and confirming current beneficiaries. Request beneficiary designation forms from each custodian or plan administrator—don't rely on memory. Compare what's on file with your current intentions and estate plan documents.

Update beneficiary forms to match your estate goals. If your will creates a trust for minor children, consider whether your IRA should name that trust as beneficiary (more on trust beneficiaries below). If you've remarried, ensure forms reflect your current spouse unless you have a specific reason and proper waivers in place. For 401(k)s, federal law requires spousal consent if you name anyone other than your spouse as primary beneficiary.

Author: Rebecca Langford;

Source: harbormall.net

Review this alignment annually and after major life events: marriage, divorce, births, deaths, moves to new states, and significant wealth changes. Set a calendar reminder each January or tie the review to tax filing season.

Coordinate with estate documents. If your will or trust includes specific bequests or distribution formulas, consider how retirement accounts fit that plan. A parent who wants to divide assets equally among three children but has $1 million in IRAs and $500,000 in other assets might name the IRA to go 2/3 to children and 1/3 to other heirs, then use the will to balance the remainder.

Consider tax implications throughout. Retirement accounts and estate plans interact with multiple tax systems: income tax on distributions, estate tax on large estates, and state-level taxes that vary widely. A tax-efficient strategy might leave tax-deferred IRAs to charity (avoiding income tax entirely) while passing taxable brokerage accounts to heirs who get a step-up in basis.

Work with both financial and legal advisors. Financial planners model distribution strategies and tax outcomes; estate attorneys draft compliant documents and navigate state law. Integrating retirement and estate planning requires both skill sets. Bring your advisor team together periodically—a joint meeting every few years ensures everyone works from the same playbook.

Plan for incapacity, not just death. Durable powers of attorney allow someone to manage retirement accounts if you become incapacitated. Health care directives and living wills address medical decisions. These documents prevent court guardianship proceedings and ensure your retirement assets can be managed according to your wishes if you can't act yourself.

Retirement Account Beneficiary Strategies for Estate Goals

Choosing beneficiaries involves more than listing names. Different beneficiary types offer distinct advantages depending on your goals.

Spousal beneficiaries receive the most flexible treatment. A surviving spouse can roll an inherited IRA into their own IRA, delaying required minimum distributions until their own required beginning date. This "spousal rollover" preserves tax deferral longer than any other option. Spouses can also remain as beneficiaries of the inherited account and take distributions based on their life expectancy, though the SECURE Act's ten-year rule doesn't apply to surviving spouses.

Non-spousal beneficiaries—adult children, siblings, friends—must generally empty inherited retirement accounts within ten years under rules that took effect in 2020 and were clarified through 2025. No annual required distributions apply for most beneficiaries, but the entire balance must be withdrawn by December 31 of the tenth year following death. This compressed timeline accelerates income tax and eliminates the old "stretch IRA" strategy that allowed distributions over a beneficiary's lifetime.

Exceptions exist for "eligible designated beneficiaries": minor children (until they reach majority), disabled individuals, chronically ill individuals, and beneficiaries less than ten years younger than the account owner. These beneficiaries can stretch distributions over their life expectancy, though minor children shift to the ten-year rule once they reach adulthood.

Author: Rebecca Langford;

Source: harbormall.net

Trusts as beneficiaries add control and protection but require careful drafting. A "conduit trust" passes all required distributions directly to trust beneficiaries, maintaining the ten-year or stretch timeline while offering some creditor protection and controlled distributions. An "accumulation trust" can hold distributions within the trust, providing maximum protection but potentially facing higher trust tax rates.

Trusts make sense when beneficiaries are minors, have special needs, struggle with money management, face creditor risks, or receive government benefits. A special needs trust can receive retirement assets without disqualifying a disabled beneficiary from Medicaid or Supplemental Security Income. A spendthrift trust protects funds from a beneficiary's creditors or poor financial decisions.

Trust beneficiaries require specific trust language to qualify as "see-through" trusts under IRS rules. The trust must be valid under state law, irrevocable at death, have identifiable beneficiaries, and provide required documentation to the plan administrator. Work with an attorney experienced in retirement benefit trusts—generic trusts often fail these requirements.

Charitable beneficiaries offer tax advantages for philanthropically inclined account owners. Charities pay no income tax on inherited retirement accounts, making tax-deferred accounts ideal charitable gifts. You avoid income tax, your estate may receive an estate tax deduction, and the charity receives the full value. Pairing this strategy with leaving low-tax-basis appreciated securities to heirs (who get a step-up in basis) maximizes family wealth.

Charitable remainder trusts provide a hybrid approach: the trust pays income to individual beneficiaries for a term of years or life, then distributes the remainder to charity. Naming such a trust as IRA beneficiary can provide income to family while ultimately benefiting charity and generating estate tax deductions.

Minor children and special needs planning demand extra attention. For minor children, consider a trust rather than direct distribution, UTMA/UGMA accounts (which offer minimal control), or Section 529 education accounts funded from the inheritance. For special needs beneficiaries, a properly drafted special needs trust preserves government benefits while supplementing quality of life.

Tax Considerations When Coordinating Plans

Retirement accounts carry unique tax burdens that estate planning must address. Understanding these taxes shapes beneficiary decisions and distribution strategies.

Author: Rebecca Langford;

Source: harbormall.net

Income tax hits every dollar withdrawn from traditional retirement accounts. Beneficiaries pay ordinary income tax at their marginal rate—potentially 37% federal plus state tax. Roth accounts escape income tax if the account was held at least five years, making Roth conversions during life a powerful estate planning tool for 2026.

The SECURE Act's ten-year distribution rule compresses this tax hit. If a beneficiary inherits a $500,000 IRA and withdraws it evenly over ten years, they add $50,000 annually to taxable income. A high earner might lose 40% or more to taxes. Strategic timing—withdrawing more in low-income years, less in high-income years—reduces the bite.

Estate tax affects fewer families in 2026 but remains significant for large estates. The federal estate tax exemption sits above $13 million per person (adjusted for inflation from the 2024 base). Married couples can combine exemptions through portability, sheltering over $26 million. Estates above these thresholds pay 40% federal estate tax.

Retirement accounts count toward the estate tax calculation at full value, even though heirs will later pay income tax on distributions. This "double tax" hits large IRAs hard. For estates near or above exemption thresholds, leaving retirement accounts to charity or using disclaimer planning can reduce estate tax while preserving wealth for heirs through other assets.

State estate and inheritance taxes vary dramatically. Some states impose estate tax at thresholds as low as $1 million. Others charge inheritance tax based on the heir's relationship to the deceased—closer relatives pay less or nothing, distant relatives or friends pay more. A few states have both. Retirement accounts face these state-level taxes the same as other assets, making state tax planning essential for retirement estate plan coordination.

Roth versus traditional account treatment creates planning opportunities. Roth accounts escape income tax for heirs but still count toward estate tax. Traditional accounts face both. For large estates, paying income tax now through Roth conversions removes future growth from the estate and shifts the tax burden from heirs to the account owner—often advantageous if the owner is in a lower bracket than heirs will be.

Required minimum distributions (RMDs) continue during life, starting at age 73 in 2026 (gradually increasing to 75 in future years under recent law changes). Failing to take RMDs triggers a 25% penalty on the amount not withdrawn. Coordinating RMDs with overall retirement income and estate planning ensures you don't over-distribute (losing tax deferral) or under-distribute (triggering penalties).

Common Mistakes in Retirement Estate Plan Coordination

The biggest mistake I see is treating retirement accounts as separate from the overall estate plan.A client will spend thousands on a sophisticated trust structure, then leave their largest asset—a $2 million IRA—directly to beneficiaries with no coordination. The IRA bypasses all those carefully crafted protections. Effective planning requires your attorney, financial advisor, and tax professional to work together, ensuring beneficiary forms, trusts, and distribution strategies align with your goals and current tax law

— Jennifer Martinez

Even careful planners stumble over predictable errors. Recognizing these mistakes helps you avoid them.

Forgetting to name beneficiaries leaves accounts to default provisions—usually your estate. This forces probate, accelerates taxes, and may distribute assets contrary to your wishes. Review every account and confirm beneficiaries are on file.

Ignoring the SECURE Act's impact leads to poor planning. The ten-year rule eliminated stretch IRAs for most beneficiaries starting in 2020. Strategies built around lifetime distributions no longer work. Plans created before 2020 need updating to reflect current law.

Failing to update after major life events creates obvious problems. Divorced people leaving accounts to ex-spouses, parents omitting new children, or plans naming deceased beneficiaries all stem from not updating forms. Make beneficiary review part of every major life transition.

Not considering state law differences causes trouble for people who move or own property in multiple states. Some states recognize common-law marriage, affecting spousal rights. Community property states treat retirement accounts earned during marriage differently than separate property states. State estate tax thresholds vary. Coordinate your plan with the laws of your current state of residence.

Naming trusts without proper drafting backfires when the trust doesn't meet see-through trust requirements. The IRA then treats the estate as beneficiary, forcing the least favorable distribution rules. Use attorneys experienced in retirement benefit trusts.

Overlooking creditor protection differences between retirement accounts and inherited accounts causes loss. ERISA-qualified plans like 401(k)s enjoy strong federal creditor protection during your life. Inherited IRAs lost bankruptcy protection in a 2014 Supreme Court case. Rolling 401(k)s to IRAs before death may expose funds to creditors that plan assets would have avoided.

Mixing up primary and contingent beneficiaries creates confusion. Primary beneficiaries inherit first; contingents receive the account only if all primaries predecease you. Listing "per stirpes" or "per capita" designations affects how shares divide if a beneficiary dies before you. Understand these terms and use them intentionally.

Retirement Account Beneficiary Comparison

| Beneficiary Type | Tax Treatment | Pros | Cons | Best For |

| Spouse | Can roll to own IRA; delays RMDs; most flexible | Maximum tax deferral; simplest administration; spousal rollover option | May not align with blended family goals; no protection from spouse's creditors or remarriage | Primary beneficiary in first marriages; maximizing deferral |

| Adult Children | 10-year distribution rule; ordinary income tax on withdrawals | Direct transfer; avoids probate; relatively simple | Compressed tax timeline; no creditor protection; no control over distributions | Responsible adult children; estates below tax thresholds |

| Trust | Depends on trust type; conduit trusts pass through distributions | Control over distributions; creditor protection; special needs planning; minor beneficiary management | Complex and costly to establish; requires specialized drafting; potential for higher trust tax rates | Minor children; special needs beneficiaries; asset protection needs; beneficiaries with poor money management |

| Charity | No income tax; estate tax deduction | Eliminates income tax; supports causes; reduces estate tax | Nothing passes to family | Philanthropic goals; large IRAs in taxable estates; when heirs have other assets |

| Estate | 10-year rule; forced through probate | None—generally disadvantageous | Probate delays and costs; creditor exposure; unfavorable tax rules; no stretch | Should be avoided in most cases |

FAQ: Retirement Legacy Planning

Retirement accounts and estate plans must work as an integrated system. When beneficiary forms contradict wills, when tax planning ignores distribution rules, or when life changes go unrecorded, families pay the price in lost wealth, legal conflicts, and missed legacy goals.

Effective retirement legacy planning starts with understanding how retirement accounts pass outside your will, recognizing the tax implications of different beneficiary choices, and coordinating these decisions with your broader estate plan. Update beneficiary designations regularly, consider trusts when protection or control matters, and align your strategy with current law—particularly the SECURE Act's ten-year distribution rule.

The intersection of retirement planning and estate planning grows more complex as accounts grow larger and families become more diverse. Blended families, special needs beneficiaries, charitable goals, and large estates all require customized approaches. Working with experienced financial and legal advisors ensures your retirement assets support your legacy vision rather than undermining it.

Take action now: pull beneficiary forms for every retirement account, compare them with your estate plan, identify gaps or outdated information, and make needed updates. The few hours invested today prevent years of problems for the people you're trying to protect.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.