Elegant wooden desk with legal estate planning documents, premium pen, glasses, and small bronze family figurine against a blurred city skyline window background

Estate Planning Tax Strategies to Reduce Your Tax Burden

You've worked decades to build wealth—why hand over 40% to the IRS when your kids could inherit it instead? Without proper planning, estates exceeding certain dollar amounts trigger massive federal and state tax bills that can devastate generational wealth transfers. But here's what most people don't realize: dozens of legal techniques exist to slash these taxes, sometimes eliminating them entirely.

The difference between paying millions in estate taxes versus paying zero often comes down to actions you take today. We're talking about specific moves with your assets, strategic use of trusts, and timing decisions that compound over years. Some strategies sound complex but become straightforward once you understand the mechanics.

Let's break down exactly how high-net-worth families protect their legacies from excessive taxation—techniques you can implement regardless of whether your estate is $5 million or $50 million.

Understanding Estate Taxes and When They Apply

When you die, the federal government takes inventory of everything you owned and calculates what you owe. That 2026 threshold? Roughly $13.99 million for one person. Anything under that number flies under the radar—no federal tax bill.

Cross that line, though, and the government claims 40 cents on every dollar above the exemption. Own $20 million in assets? That's about $2.4 million going to Uncle Sam instead of your children.

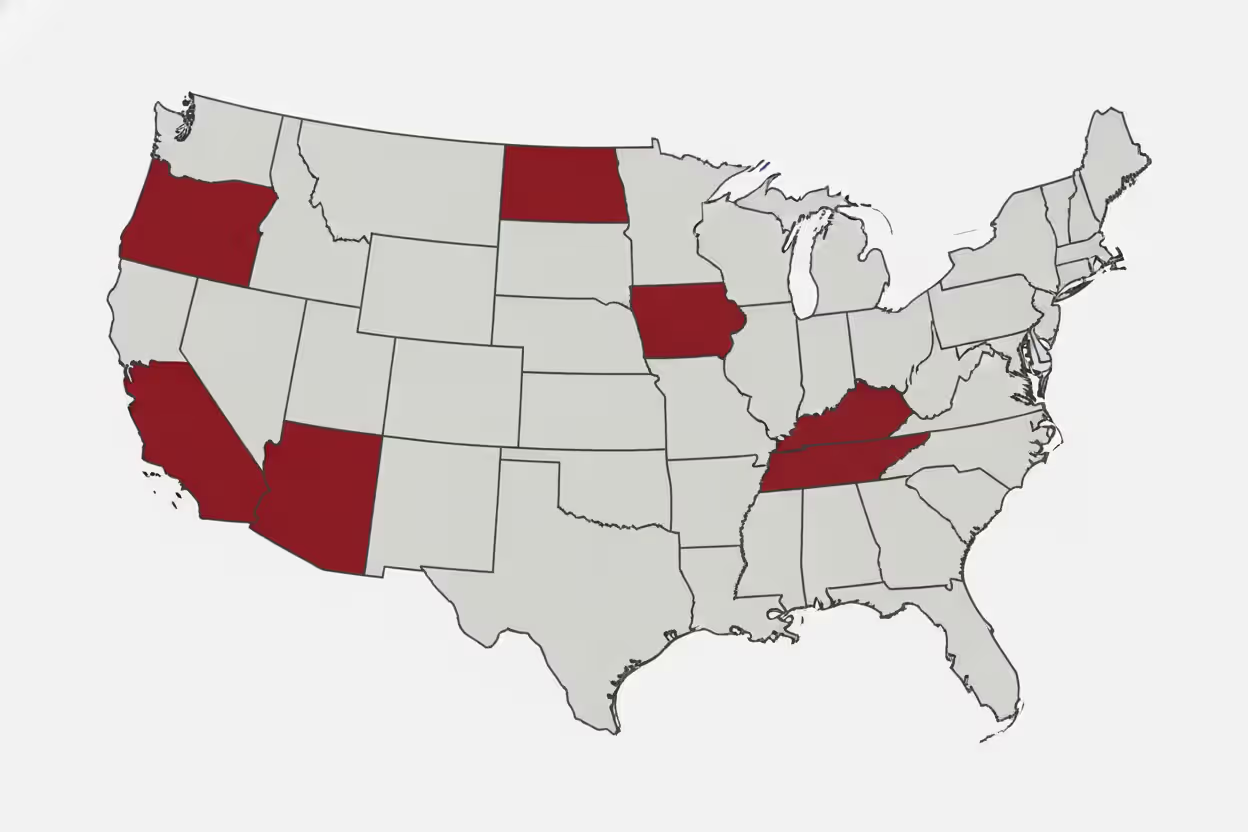

But federal taxes tell only part of the story. A dozen states—plus Washington D.C.—run their own estate tax systems completely separate from federal rules. Oregon hits estates at just $1 million. Massachusetts does the same. If you live in these states, you're facing tax bills even though your estate wouldn't trigger a penny of federal liability.

Here's what counts toward your total: every property deed in your name, each brokerage account, your business ownership stake, retirement accounts like 401(k)s and IRAs, and yes—life insurance death benefits if you control the policy. The IRS demands current market values as of your death date, though executors can choose a valuation six months later if values have dropped.

Who actually pays these taxes in practice? Single folks with estates pushing $14 million. Married couples approaching $28 million combined. Business owners often get surprised here—a company appraised at $8 million might not generate anywhere near that in cash, yet it still counts toward the taxable total. And anyone living in Massachusetts, Oregon, or another low-threshold state needs to plan even with modest wealth.

Author: Rebecca Langford;

Source: harbormall.net

Gifting Strategies That Lower Your Taxable Estate

Here's something powerful: assets you give away during life disappear from your taxable estate. The IRS actually encourages this through several exemptions designed for wealth transfer.

Annual Gift Tax Exclusion

Every single year, you can hand $19,000 to as many people as you want—no paperwork, no tax consequences. Married? You and your spouse together can give $38,000 per person. Do the math with a large family. Three kids, eight grandchildren—that's $418,000 leaving your estate annually if you're married.

The real magic happens with appreciating assets. Say you gift your daughter stock worth $19,000 today. Ten years later, it's worth $95,000. That entire $76,000 of growth occurred outside your estate. You'll never pay estate tax on that appreciation because you don't own it anymore. She does inherit your original cost basis (a tax consideration for her later), but compared to having $95,000 taxed at 40% in your estate, she comes out way ahead.

One more thing people miss: you can pay unlimited amounts directly to schools for tuition or to hospitals for medical bills without touching your $19,000 annual limit. Your grandson's $60,000 Stanford tuition? Write the check straight to the university—doesn't count as a gift. But send $60,000 to your grandson to pay tuition himself, and you've just used up your annual exclusion plus $41,000 of your lifetime exemption.

Lifetime Gift Tax Exemption

Beyond the annual $19,000 per person, you've got a massive lifetime bucket—that same $13.99 million exemption. You can give away that entire amount while alive without paying a dime in gift tax. Yes, it reduces what's available as an estate tax exemption later, but you're trading future appreciation for a known exemption amount today.

Real-world example: You transfer a $4 million commercial building into an irrevocable trust for your kids. That uses $4 million of your lifetime exemption. But the building doubles to $8 million before you die. Result? You've removed $8 million from your taxable estate while only "spending" $4 million of exemption. The $4 million appreciation never gets taxed because it happened after the gift.

This strategy becomes critical when exemptions might drop. Congress keeps changing these numbers. We saw exemptions jump to current levels in 2018, extended through 2028, but proposals to cut them back surface regularly. Lock in gifts at today's high exemption amounts, and you're protected even if future laws reduce the threshold to $7 million or $5 million.

Direct Payment of Medical and Education Expenses

Grandparents funding private school, college, grad school—this provision gets used constantly by wealthy families. The education payment only covers tuition itself, not housing or meal plans or books. For medical expenses, they must qualify as tax-deductible medical costs under IRS rules. Health insurance premiums usually don't qualify unless the person is unemployed.

But when it works, it's phenomenal. You're moving substantial money out of your estate (a $70,000 medical procedure, a $50,000 annual tuition bill) while keeping your $19,000 annual exclusions and your $13.99 million lifetime exemption completely intact for other gifts.

Using Trusts to Minimize Estate Tax Exposure

Trusts sound intimidating, but they're just legal containers that hold assets under specific rules. The right trust removes assets from your estate while letting you maintain some benefits or control—you can't do that with simple gifts.

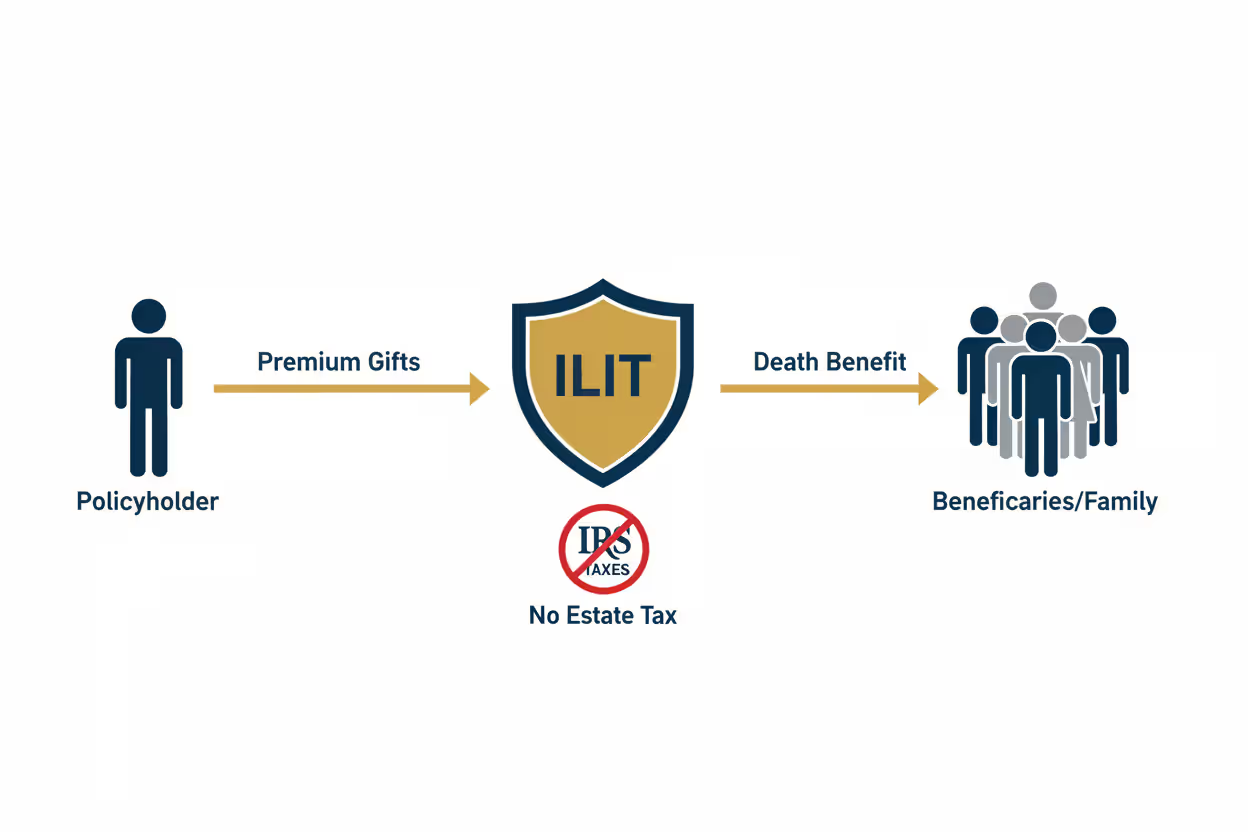

Irrevocable Life Insurance Trusts (ILITs)

Most people don't realize life insurance counts toward your taxable estate. Own a $5 million policy when you die? That's $5 million added to your estate valuation, potentially triggering $2 million in estate taxes.

An ILIT solves this by owning the policy instead of you. You gift money into the trust (using annual exclusions), the trust pays premiums, and when you die, proceeds land in the trust—completely bypassing your taxable estate. Your beneficiaries receive annual notices of their right to withdraw contributions (called Crummey notices, after the court case), which qualifies your contributions as present-interest gifts eligible for the annual exclusion.

Consider someone with a $12 million estate and a $10 million life insurance policy. Without an ILIT, the combined $22 million estate generates roughly $3.2 million in federal estate tax. With an ILIT properly structured, the insurance proceeds stay outside the estate calculation entirely, potentially eliminating the tax bill.

The trust can even loan money back to your estate if cash is needed for taxes or expenses, or purchase assets from your estate. You've got flexibility despite the irrevocable nature.

Author: Rebecca Langford;

Source: harbormall.net

Grantor Retained Annuity Trusts (GRATs)

Want to transfer assets but nervous about gift taxes? GRATs let you move appreciating property to heirs with minimal gift tax impact—sometimes zero.

Here's the mechanism: You fund the trust with assets, and it pays you a fixed annuity for a set period (typically 2-10 years). When the term ends, whatever remains goes to your beneficiaries. The taxable gift equals only the remainder value, calculated using IRS interest rate assumptions.

If your assets grow faster than the IRS assumed rate (currently hovering around 5.6%), the excess passes to beneficiaries tax-free. Put $2 million of stock in a two-year GRAT structured to return your $2 million through annuity payments. The stock jumps to $3.2 million. Your taxable gift? Nearly zero. Your kids receive? $1.2 million tax-free.

Short-term GRATs with volatile assets minimize risk. If the stock tanks instead of rising, you simply get back the depreciated asset—no harm done. Wealthy families run multiple short-term GRATs continuously, capturing appreciation when it happens.

Qualified Personal Residence Trusts (QPRTs)

Your primary home or vacation property can transfer to children at massively discounted gift values through a QPRT. You move the house into the trust but keep the right to live there rent-free for, say, 15 years. After that period, your kids own it.

The gift value gets discounted because your kids don't receive the property immediately—they're waiting 15 years. A 58-year-old transferring a $4 million beach house with a 12-year retained interest might only make a $1.5 million taxable gift. The property appreciates to $6.5 million over those years? The $5 million difference escaped estate taxation entirely.

The downside: die during the term, and the house bounces back into your taxable estate as if the QPRT never existed. After the term expires, you'll need to pay market-rate rent to keep living there, or the tax benefits unravel. Still, for healthy individuals with valuable homes and long time horizons, QPRTs deliver enormous tax savings.

Charitable Remainder Trusts

These trusts feed you income while you're alive, then deliver remaining assets to charity at death. You get an immediate income tax deduction based on the calculated remainder going to charity, assets leave your taxable estate, and you receive annual payments for life or a term of years.

A charitable remainder unitrust (CRUT) recalculates annually, paying a percentage of the trust's value each year. Strong investment performance means higher income. This works well for younger beneficiaries expecting 20-30 year payout periods.

Charitable remainder annuity trusts (CRATs) pay fixed dollar amounts regardless of investment performance. Retirees wanting predictable income prefer this structure, though inflation erodes purchasing power over decades.

Charitable Giving as an Estate Tax Reduction Tool

Every dollar left to qualified charities reduces your taxable estate by a dollar—no cap, no limits. The unlimited charitable deduction means you can leave $50 million to charity with zero estate tax on those funds.

Simple bequests work fine: "I leave $500,000 to the American Cancer Society." Done. But more sophisticated approaches add flexibility and benefits.

Donor-advised funds (DAFs) let you make a charitable contribution now, claim the deduction, then recommend grants to specific charities over time. Fund a $3 million DAF through your estate, and those assets vanish from estate tax calculations while your children or grandchildren advise on grant distributions for years. Many families use DAFs to teach younger generations about philanthropy—kids see the impact of charitable giving firsthand while managing real money.

Charitable lead trusts flip the remainder trust concept: charity receives income payments for a period (say, 15 years), then assets transfer to your heirs. You want to benefit charity immediately but ultimately pass wealth to family. The estate tax deduction equals the present value of all those income payments to charity.

Private foundations offer maximum control—you and your family serve as trustees, hire staff, and build a multi-generational philanthropic institution. The administrative burden and regulatory compliance are substantial, but for families serious about lasting charitable impact, foundations justify the complexity. The estate tax deduction equals the full value of assets contributed.

Marital Deduction and Portability Strategies for Couples

Unlimited marital deduction means you can leave your entire estate to your U.S. citizen spouse without triggering any estate tax. Sounds perfect, right? It just delays the problem—when your spouse dies, their estate includes everything, potentially creating a massive tax bill.

Portability changes the game for married couples. When the first spouse dies, the survivor can claim any unused portion of the deceased spouse's exemption—but only if the executor files an estate tax return (Form 706) and elects portability, even when no tax is owed.

Author: Rebecca Langford;

Source: harbormall.net

Walk through an example: Husband dies in 2026 with a $6 million estate and the $13.99 million exemption. The executor files Form 706 electing portability. Wife now has her own $13.99 million exemption plus husband's unused $7.99 million, totaling $21.98 million she can pass tax-free. Skip the portability election? She's stuck with only her $13.99 million exemption, potentially leaving millions exposed to taxation.

Portability has limits, though. It doesn't apply to the generation-skipping transfer tax exemption. Remarriage erases the previous spouse's unused exemption, replaced by the new spouse's. And portability offers zero protection from creditors or claims by a new spouse—assets in the surviving spouse's name remain vulnerable.

Traditional AB trust structures (bypass trusts or credit shelter trusts) provide more robust protection. At the first death, assets up to the exemption amount fund the B trust (bypass trust), with remaining assets passing to the A trust (marital trust) for the surviving spouse. The B trust assets and all future appreciation stay permanently outside the surviving spouse's taxable estate.

Modern planning often combines both approaches: elect portability for flexibility, but include trust provisions allowing the survivor to disclaim assets into a bypass trust if circumstances warrant. This gives options based on tax law changes and family situations when the first spouse dies.

Common Estate Planning Tax Mistakes to Avoid

Even expensive, professionally drafted plans fail when families make these errors.

Outdated beneficiary forms destroy carefully laid plans. Retirement accounts, 401(k)s, IRAs, and life insurance transfer according to beneficiary designation forms—your will and trust don't control them. An ex-spouse listed on a 401(k) from 15 years ago gets the money, regardless of what your will says. Minor children named directly create guardianship nightmares. Deceased individuals as beneficiaries force assets through probate. Review these forms every two to three years and immediately after divorce, remarriage, births, or deaths.

Unused annual exclusions vanish forever. That $19,000 per person gift exclusion doesn't roll over. Fail to use it in 2026? It's gone. You can't make it up in 2027. A married couple with four children who never make annual exclusion gifts lose $152,000 in tax-free transfers every single year that never comes back.

Empty trusts provide zero benefits. Creating a beautiful revocable living trust or irrevocable life insurance trust means nothing if you never fund it. Real estate requires new deeds transferring property into the trust. Investment accounts need retitling. Life insurance needs beneficiary designation changes to the trust. I've seen $8 million estates with carefully drafted trusts that owned exactly zero dollars in assets—complete waste because the attorney drafted documents but nobody handled the funding.

State estate taxes ambush people focused only on federal planning. Your $10 million estate faces no federal estate tax, but Massachusetts or Oregon will still send a bill because their thresholds sit at $1 million. Residents of low-exemption states need layered strategies: aggressive gifting programs, irrevocable trusts, or even relocating to states like Florida or Texas with no state estate tax.

Waiting until you're sick eliminates your best options. Many strategies need years to deliver maximum value. GRATs require time for assets to appreciate. Annual gifting programs compound over decades. Once you're incapacitated, you can't create or fund irrevocable trusts. Transfers made within three years of death get pulled back into your estate for certain assets like life insurance. Plus, nobody wants to discuss wealth transfer strategy while battling cancer or recovering from a stroke—do this while you're healthy and clear-headed.

DIY estate planning for large estates courts disaster. TurboTax works for simple tax returns. LegalZoom handles basic wills. Tax-efficient estate planning for multi-million dollar estates requires coordination between estate planning attorneys, CPAs experienced in gift and estate tax, and financial advisors who understand trust investments. The $25,000 you spend on proper professional guidance looks trivial compared to the $3 million estate tax bill that results from mistakes.

The biggest mistake I see is families treating estate planning as a one-time event rather than an ongoing process. Tax laws change, family circumstances evolve, and asset values fluctuate. A plan created ten years ago may be completely ineffective today—or worse, create unintended consequences. Regular reviews, ideally every two to three years, ensure your strategies remain aligned with current law and your goals

— Patricia Soldano

Frequently Asked Questions About Estate Tax Planning

Massive estate tax bills aren't inevitable—they're optional for families who plan strategically. The federal government offers a generous exemption protecting most estates, but cross that threshold or live in a low-exemption state, and you're facing tax rates that can consume 40% or more of your wealth.

The techniques we've covered range from straightforward (annual gifting, direct tuition payments) to sophisticated (GRATs, ILITs, charitable trusts). Start with simple approaches matching your current situation, then layer in complex strategies as your estate grows. Someone with a $6 million estate might focus on annual gifting and proper beneficiary designations. Hit $15 million, and irrevocable trusts become essential.

Timing determines success more than you'd expect. Strategies deployed a decade before death deliver maximum benefit. Last-minute planning—drafting documents when you're already sick—offers limited options and often fails completely if you become incapacitated. Legislative changes add urgency; today's high exemptions might get slashed by future Congresses, making current action more valuable than waiting.

Don't attempt this alone. Estate attorneys, CPAs specializing in gift and estate tax, and financial advisors who understand trust taxation need to coordinate your plan. Professional fees seem expensive until you compare them to the millions saved through proper implementation.

Your strategy should balance tax efficiency against practical realities. The most effective plans reflect your actual values and family dynamics, not just maximum tax reduction. Sometimes paying modest taxes while maintaining flexibility serves you better than eliminating every dollar of tax through rigid irrevocable structures. Create a legacy supporting your family and chosen causes across generations—that's the real goal, with tax efficiency as the tool making it happen.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.