Overhead view of a wooden desk with estate planning documents, folders, a pen, eyeglasses, a miniature house model, and a coffee cup in warm natural light

Estate Planning Tax Guide for Protecting Your Assets

Here's what nobody tells you about wealth transfer: the IRS and state tax collectors might claim 40% or more of what you've spent decades building. I've watched families lose the farm—literally—because they ignored estate planning taxation. One client's children had to sell their father's business for pennies on the dollar just to cover the tax bill. That business had been in the family for three generations.

You can prevent this outcome. Strategic planning protects your wealth while keeping everything completely legal.

What Are Estate Taxes and Who Pays Them

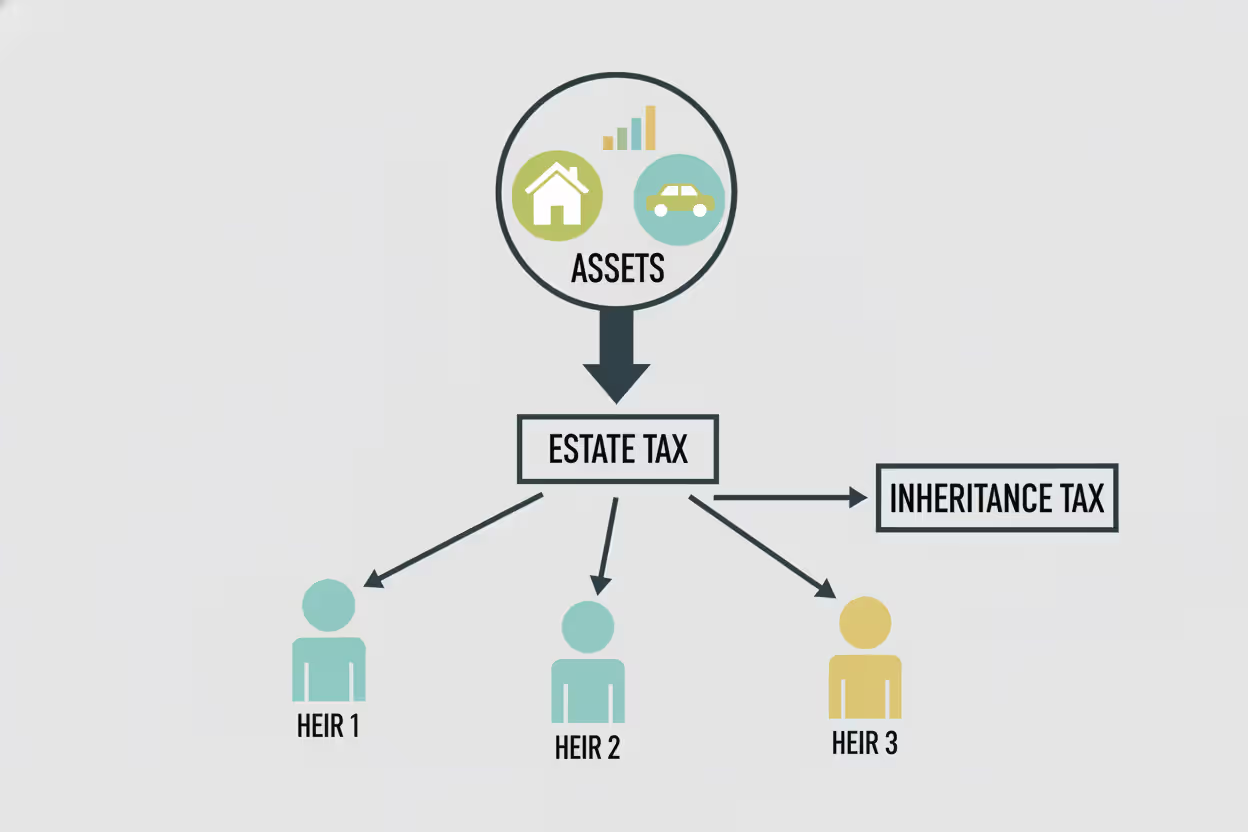

Think of estate tax as the government's final bill before your assets transfer to heirs. Here's how it works: After you die, the IRS adds up everything you own—your house, investment portfolio, that classic car collection, business interests, even your jewelry and art. They calculate the total fair market value of these assets.

For 2026, single filers get a $13.99 million exemption. Married couples? They can shield $27.98 million if they structure things correctly (that's called portability, and you'll need to file paperwork to claim it). Stay under these amounts and federal estate tax won't touch you. Cross that line, though? The tax rate starts at 18% and jumps quickly to 40% on the highest value estates.

But wait—there's more. And it's not good news.

Seventeen states (plus D.C.) run their own estate tax systems. These states set much lower exemption thresholds. Massachusetts and Oregon start taxing estates worth just $1 million. Live in a pricey neighborhood near Boston? You might have a $1.5 million home, a $500K retirement account, and suddenly you're facing state estate tax even though your net worth wouldn't impress most financial advisors.

Now here's where it gets confusing: estate tax versus inheritance tax. What's the difference?

Estate tax hits the total estate before anyone receives a penny. The estate executor pays it from estate funds. Six states impose inheritance tax instead—Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. This version taxes each beneficiary individually based on what they inherit. Maryland is particularly aggressive, collecting both types. Your estate pays estate tax, then your heirs pay inheritance tax on what's left. Double taxation at its finest.

Author: Jonathan Whitmore;

Source: harbormall.net

How Estate Planning Reduces Your Tax Burden

Smart planning can slash your tax bill—sometimes to zero. The strategies I'm about to describe aren't loopholes. Congress deliberately built these mechanisms into the tax code to encourage wealth transfer and charitable giving.

Start with annual gifting. You can give $19,000 to any person in 2026 without triggering gift tax or touching your lifetime exemption. No limit on recipients. Give to your three kids, eight grandchildren, favorite nephew, and your best friend since college—that's $247,000 leaving your taxable estate this year alone. Married? Double those numbers. You and your spouse can jointly gift $38,000 per person. Run this strategy for ten years and you've moved nearly $2.5 million out of your estate, plus whatever those gifts grow to.

Trusts offer more dramatic tax benefits, but you'll sacrifice control. Irrevocable trusts permanently remove assets from your estate—both the original value and all future appreciation. The IRS won't count these assets when calculating your estate tax. Revocable trusts? Zero estate tax benefit because you maintain complete control.

Charitable giving serves two masters. You support causes you care about while cutting estate taxes. Transfers to qualified charities receive unlimited estate tax deductions. Got stock that's appreciated significantly? Donate it directly. You avoid capital gains tax and remove it from your taxable estate.

Life insurance needs special attention. Death benefits aren't subject to income tax—your beneficiaries receive the full amount. But if you own the policy when you die, the IRS includes the death benefit in your taxable estate. A $2 million policy could generate an $800,000 estate tax at the top bracket. Transfer ownership to an irrevocable life insurance trust (more on this later) and that same $2 million passes tax-free to your heirs.

Common Estate Planning Tax Mistakes to Avoid

I've reviewed hundreds of estate plans over the years. The same mistakes appear repeatedly.

Outdated beneficiary designations top the list. Your will doesn't control retirement accounts, life insurance, or payable-on-death accounts. These assets flow directly to named beneficiaries. I once met a woman who received her ex-husband's $500K life insurance policy because he never updated the beneficiary form after their divorce. His current wife and kids got nothing from that policy. Check your beneficiary designations now—particularly if you've married, divorced, or experienced a death in the family since you originally completed those forms.

State tax blindness creates another problem. Maybe you're comfortably under the $13.99 million federal threshold with a $3 million estate. But you live in Massachusetts where estate tax kicks in at $1 million. You're looking at roughly $200K in state estate tax that proper planning could have prevented. Retirees who move from Texas (no estate tax) to Massachusetts often don't realize they've created a substantial new tax liability just by changing their address.

Defective trust construction wastes time and money. I've seen people establish "irrevocable" trusts while maintaining practical control—serving as sole trustee, keeping the power to change beneficiaries, or retaining the right to revoke it. The IRS isn't stupid. They'll include those trust assets in your taxable estate because you haven't truly given up ownership.

Ignoring annual gift exclusions represents opportunity lost. A couple with four kids and eight grandchildren can transfer $456,000 every single year through annual exclusion gifts. Over a decade? That's $4.56 million removed from their estate, plus whatever investment returns those gifts generate. Yet many wealthy families never make systematic gifts, leaving millions unnecessarily exposed to estate tax.

DIY estate planning looks tempting. Download a template, fill in the blanks, save $5,000 in legal fees. Except that $5,000 savings might cost your heirs $500,000 in unnecessary taxes. Generic documents ignore state-specific rules, miss valuable tax strategies, and often contain subtle errors that create massive problems. Tax issues in estate planning multiply when non-experts draft the documents.

Author: Jonathan Whitmore;

Source: harbormall.net

Estate Planning Tools That Minimize Taxation

Irrevocable Life Insurance Trusts (ILITs)

Want to remove life insurance from your taxable estate? An ILIT does exactly that. The trust owns your policy—not you. You fund the trust (typically through annual gifts that use your gift tax exclusion), the trust pays premiums, and when you die the trust receives the death benefit outside your taxable estate.

Let's run numbers. You personally own a $3 million policy. That's $3 million added to your taxable estate, potentially triggering $1.2 million in federal estate tax if you're in the top bracket. Transfer that identical policy to a properly structured ILIT? Your heirs receive the full $3 million tax-free.

Two critical requirements: You'll need an independent trustee (not you), and if you're transferring an existing policy you must survive three years after the transfer for the IRS to respect the ownership change. Die within three years and the IRS pulls the policy back into your estate.

Charitable Remainder Trusts

These vehicles convert appreciated assets into income streams while reducing estate taxes. Here's the structure: You contribute assets (typically appreciated stock or real estate) to the trust. The trust pays you (and optionally your spouse) regular income for life or a set number of years. When the trust term ends, remaining assets go to your chosen charity.

Tax benefits hit immediately. You get an income tax deduction based on the calculated present value of what the charity will eventually receive. That contributed asset also leaves your taxable estate. Better yet, the trust can sell appreciated assets without paying capital gains tax, then reinvest the full proceeds to generate your income.

Example: You funded a CRT with $2 million in stock that cost you $200,000 originally. The trust sells it, pays zero capital gains tax on the $1.8 million gain, and invests the full $2 million to produce your income stream. You receive an immediate income tax deduction (the exact amount depends on your age, trust terms, and IRS interest rates), and you've removed $2 million from your taxable estate.

Grantor Retained Annuity Trusts (GRATs)

GRATs work beautifully for transferring appreciating assets while minimizing gift tax. The mechanics: You contribute assets to the trust, which pays you fixed annuity payments for a term you specify (often 2-10 years). When the term expires, whatever remains passes to your beneficiaries.

The taxable gift equals the calculated present value of what beneficiaries will likely receive—not the full value of what you contributed. If assets appreciate faster than the IRS assumed rate (Section 7520 rate), excess appreciation transfers to heirs gift-tax-free.

Here's a real scenario: You establish a five-year GRAT with $5 million in stock. The IRS assumes 5.6% growth. Your stock actually grows 20% annually, reaching $12.44 million. The $7.44 million excess appreciation passes to your children consuming little or no lifetime exemption. You've effectively transferred significant wealth at a fraction of the gift tax cost.

Family Limited Partnerships

Author: Jonathan Whitmore;

Source: harbormall.net

Family limited partnerships (FLPs) or LLCs consolidate family assets—typically real estate or business interests—into one entity. You maintain control as general partner while gifting limited partnership interests to family members.

Tax savings come through valuation discounts. Limited partnership interests lack two crucial features: marketability (can't easily sell to outsiders) and control (limited partners can't direct management). Professional appraisers routinely apply 20-40% discounts when valuing these interests.

Translation? You transfer $1 million in actual real estate value by gifting limited partnership interests appraised at $600,000-$800,000. You've just maximized how much wealth moves to heirs within your available exemption.

State Estate Tax vs Federal Estate Tax

Understanding both systems prevents expensive surprises. Here's how they compare:

| Feature | Federal Estate Tax | State Estate Tax |

| Exemption Amount (2026) | $13.99 million individual / $27.98 million married couples | Varies wildly; Massachusetts and Oregon start at $1 million while Connecticut exempts up to $13.61 million |

| Tax Rates | Graduated from 18% climbing to 40% | Typically 10-20% depending on state, though some mirror federal rates |

| Portability Rules | Available—surviving spouses can claim deceased spouse's unused exemption with proper election | Generally unavailable; Hawaii and Maryland are exceptions |

| Filing Requirements | Required when gross estate exceeds exemption, even if no tax owed | State-specific; some states require filing regardless of tax owed |

| States Affected | Every US resident and citizen | Only these states: Connecticut, District of Columbia, Hawaii, Illinois, Massachusetts, Maryland, Maine, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington; separate inheritance taxes exist in Iowa, Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania |

Portability deserves explanation. The federal system lets surviving spouses use their deceased spouse's unused exemption—but most states don't offer this. Consider a New York couple with $20 million combined assets. They're fine federally (under the $27.98 million married couple threshold) but face significant New York estate tax because that state maintains lower exemptions and doesn't allow portability.

Multi-state property complicates everything. Your domicile state taxes your entire estate. Additional states where you own tangible property can impose separate estate taxes on those specific assets. A New York resident owning a Florida vacation home and Montana ranch deals with New York estate tax on everything, though fortunately neither Florida nor Montana currently impose estate taxes.

State laws change constantly. Some states are phasing out estate taxes or raising exemptions substantially. Others might lower exemptions or create new taxes. The scheduled 2026 reduction in federal exemptions (when temporary increases sunset) may trigger state-level changes too. Stay current or work with professionals who track these developments.

When to Hire an Estate Planning Tax Professional

Certain situations absolutely demand professional guidance.

First trigger: your estate approaches or exceeds exemption thresholds—federal or state. An experienced attorney who saves your family $500,000 in estate taxes easily justifies $15,000 in planning fees. This math is simple.

Business ownership adds layers of complexity requiring specialized knowledge. Closely held companies present valuation challenges, succession planning needs, and opportunities for sophisticated techniques like GRATs or intentionally defective grantor trusts. Business interests also create liquidity problems—your estate needs cash to pay taxes, but your wealth sits locked in an illiquid business.

Substantial real estate holdings generate similar challenges. Property appreciates significantly over time, often pushing estates beyond exemption limits. Properties in multiple states create multi-jurisdictional tax complications. Real estate also enables advanced strategies like qualified personal residence trusts or conservation easements that require expert implementation.

Blended families need particularly careful planning. Providing for your current spouse while ultimately directing assets to children from a prior marriage requires specifically designed trusts. Simple plans typically fail here, creating family conflict and avoidable tax liability.

Tax rules governing estate transfers change constantly. What works today may fail in five years. I've watched families lose millions because they created plans in 2010 and never looked at them again. Regular reviews with qualified professionals are essential for preserving wealth across generations

— Jennifer Morrison

Look for professionals with relevant credentials: estate planning attorneys, CPAs specializing in estate taxation, or chartered financial consultants. The team approach—attorney, CPA, and financial advisor working together—typically produces optimal results for complex estates.

Frequently Asked Questions About Estate Planning and Taxes

Estate planning taxation represents one of few areas where proactive steps can preserve hundreds of thousands or millions for your family. The strategies outlined here—systematic annual gifting, irrevocable trusts, charitable planning, and business succession techniques—provide concrete methods for reducing tax exposure while accomplishing your wealth transfer goals.

Timing matters enormously. Many tax-efficient strategies need extended timeframes to work properly. Irrevocable life insurance trusts require three years to successfully remove policies from your estate. Annual exclusion gifting programs compound their impact across decades. GRATs and similar vehicles work best when you have years for contributed assets to appreciate.

Don't let complexity freeze you into inaction. Start with accessible steps: implement annual exclusion gifting, verify your beneficiary designations are current, determine whether your estate faces state-level taxation. As your wealth grows or circumstances become more complex, engage qualified professionals who can deploy sophisticated strategies customized to your situation.

The taxes and estate planning environment will keep evolving. Exemption thresholds may contract, rates may shift, and new planning opportunities may emerge. Periodic reviews ensure your plan adapts to these changes while continuing to protect the wealth you've worked your entire career to build. Your beneficiaries will thank you.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.