Dark wood desk in a law office with open legal trust documents, an insurance policy with a seal, a gold fountain pen, and blurred bookshelves with leather-bound legal books in the background

ILIT Estate Planning Guide

Content

Content

Wealthy families often pour energy into crafting detailed wills and establishing basic trusts, yet many miss a strategic opportunity hiding in plain sight: life insurance held outside the taxable estate. An irrevocable life insurance trust (ILIT) transforms what might become a tax liability into a wealth preservation vehicle, but only when structured with precision and maintained with discipline.

The approach demands careful attention. Creating an ILIT means navigating IRS regulations that penalize missteps, committing to decades of consistent funding, and surrendering flexibility that most people instinctively want to preserve. Yet families staring down significant estate tax bills often find that few alternatives deliver comparable results: substantial wealth transferred tax-free, death benefits shielded from lawsuits, and distributions managed according to your values rather than a probate judge's timeline.

What Is an Irrevocable Life Insurance Trust?

An ILIT functions as a permanent legal structure that holds life insurance coverage completely separate from everything else you own. The defining characteristic—irrevocability—means you forfeit the ability to modify terms, dissolve the arrangement, or reclaim control once you sign the documents. Beneficiaries must approve any substantive changes. This rigidity isn't a design flaw; it's precisely what creates the estate tax benefits.

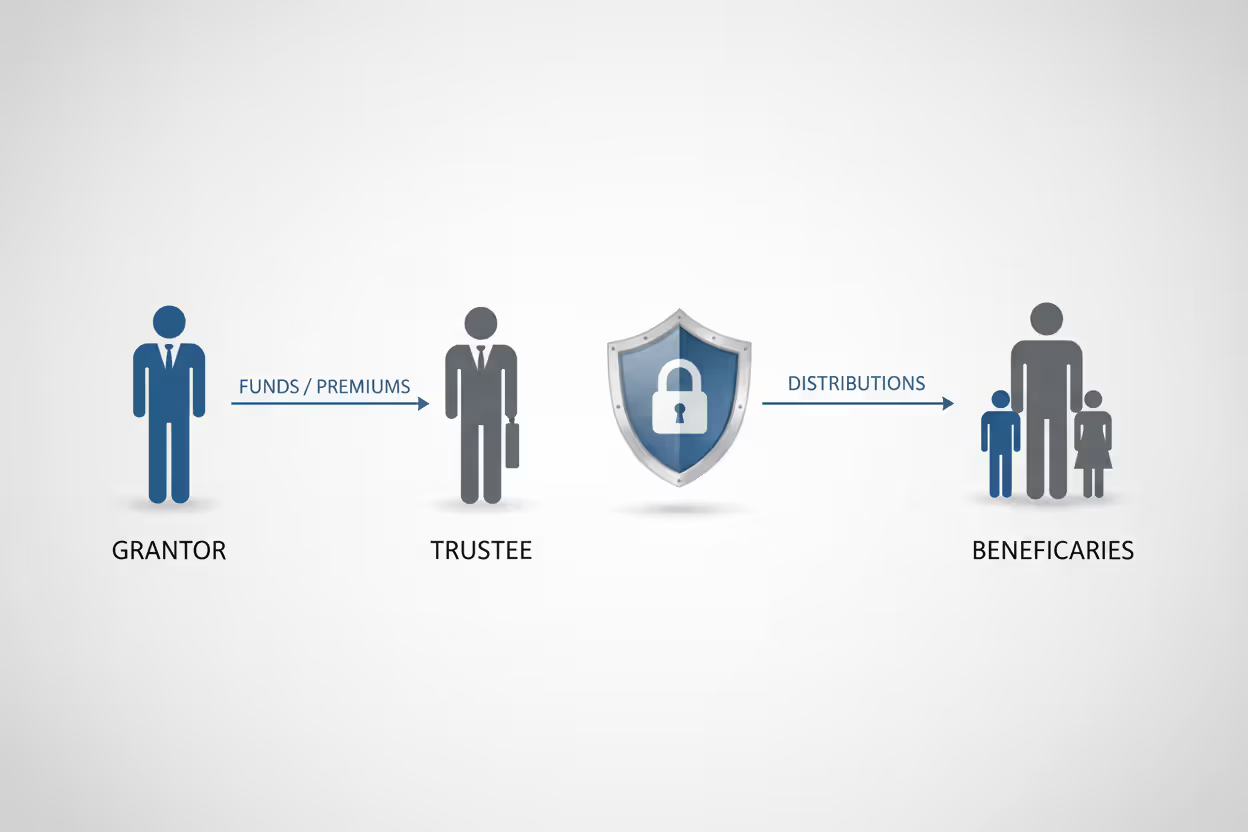

Every ILIT involves three distinct roles:

The grantor establishes the trust and provides cash annually for premium payments. Your life is insured under the policy, but you cannot maintain any ownership interest or policy rights whatsoever.

The trustee handles day-to-day management: paying premiums from gifted funds, sending mandatory notices to beneficiaries, maintaining detailed records, and eventually distributing proceeds according to the trust terms. This must be someone other than yourself—an independent party with no conflicts.

The beneficiaries ultimately receive the insurance proceeds after your death. They also receive temporary withdrawal rights—known as Crummey powers—each time you contribute money, which transforms your contributions into present-interest gifts eligible for annual gift tax exclusions.

The fundamental difference from revocable structures comes down to control. With revocable trusts, you retain power to modify beneficiaries, adjust terms, or terminate the arrangement entirely. That flexibility feels comfortable but delivers zero estate tax advantages because the IRS treats assets you control as owned by you. IRC Section 2042 excludes life insurance from your taxable estate only when you possess no ownership incidents—a requirement that irrevocability satisfies.

Author: Michael Stratford;

Source: harbormall.net

How ILITs Work in Estate Planning

The operational cycle follows a predictable annual rhythm. You transfer cash to the trust as a gift. Your trustee immediately notifies beneficiaries that they may withdraw the gifted amount, typically within a 30-day window. Beneficiaries refrain from withdrawing—they understand the money needs to pay insurance premiums—but their legal right to access the funds converts your gift from a future interest to a present interest, qualifying it for the annual gift tax exclusion. After the withdrawal period expires, your trustee remits payment to the insurance carrier.

Upon your death, the insurance carrier sends the death benefit directly to the trust rather than your estate. Since the trust owned the policy throughout, those proceeds escape federal estate taxation entirely under current law. Your trustee then follows the distribution instructions you embedded in the trust document—perhaps paying out immediately to adult children, holding funds in sub-trusts for minors, or providing strategic liquidity to cover estate taxes on illiquid assets like real estate or business interests.

Two technical rules require careful navigation.

The Three-Year Lookback Rule

IRC Section 2035(a) creates a trap for transferred policies. Should you move an existing life insurance policy into an ILIT and die within the subsequent 36 months, the IRS includes the full death benefit in your taxable estate as though the transfer never occurred.

Consider this scenario: You transfer a $2 million policy to your newly created ILIT in March 2026. Unfortunately, you pass away in November 2028—just 32 months later. The IRS adds the entire $2 million back into your estate for tax calculations, eliminating the intended benefit. But surviving past March 2029 means the policy permanently resides outside your taxable estate.

The cleaner approach: have the ILIT apply for and purchase coverage directly as the original owner. Policies the trust owns from inception never trigger the three-year rule because you never possessed ownership rights to transfer.

Crummey Withdrawal Rights Explained

Contributions to an ILIT technically represent future-interest gifts—beneficiaries cannot immediately use the money since it's designated for insurance premiums. Unfortunately, future-interest gifts don't qualify for the annual exclusion (which sits at $19,000 per beneficiary in 2026, adjusted periodically for inflation).

Crummey powers—named after a landmark 1968 tax case—solve this dilemma by granting beneficiaries a temporary window to withdraw each gift. Your trustee must provide written notification every single time, and beneficiaries typically receive 30 to 60 days to exercise their rights.

Practically speaking, beneficiaries never actually withdraw the funds. They recognize that taking the money would cause the insurance policy to lapse and destroy the family's estate plan. Yet having the legal authority—regardless of whether they use it—reclassifies the gift as a present interest, unlocking your annual exclusion.

Here's a typical structure: You contribute $57,000 to your ILIT, and your three adult children each receive notice of a $19,000 withdrawal right. All three allow the deadline to pass without withdrawing. The trustee pays the annual premium, and you've completed a gift-tax-free transfer.

Author: Michael Stratford;

Source: harbormall.net

Key Benefits of Using an ILIT

The strategic advantages of life insurance trust estate planning reach beyond straightforward tax reduction.

Estate tax exclusion drives most planning decisions. Federal estate tax exemptions for 2026 hover around $13.99 million per individual—approximately $28 million for married couples using portability. These elevated thresholds sunset at year-end 2025, likely reverting to roughly $7 million per person adjusted for inflation. Estates crossing these lines face a punishing 40% federal rate. Removing a $5 million death benefit from your estate through an ILIT saves $2 million in taxes for families in the highest bracket—enough to justify considerable setup and maintenance expenses.

Creditor protection strengthens significantly when policies sit inside properly drafted trusts rather than under direct ownership. State laws vary, but ILIT-held insurance generally remains beyond the reach of your creditors. Spendthrift provisions can similarly shield beneficiaries from their own creditors, lawsuits, or bankruptcy proceedings. A child facing a divorce or business failure cannot see trust assets seized to satisfy judgments.

Distribution control lets you dictate exactly when and how beneficiaries receive proceeds rather than handing over millions in a single lump sum. Perhaps your 28-year-old daughter receives income distributions but doesn't access principal until age 40. Maybe your son with substance abuse issues receives funds only for health, education, and basic support—supervised by an independent trustee. For second marriages, you might provide lifetime income to your surviving spouse while ensuring your children from a first marriage ultimately receive the remaining principal.

Probate avoidance happens automatically. Death benefits transfer directly to the trust without court supervision, public filing, or the delays that plague probate estates. Beneficiaries typically receive funds within weeks rather than months or years, and the entire process remains confidential.

Premium financing strategies become viable for ultra-wealthy families purchasing policies with death benefits exceeding $10 million. The trust borrows funds to pay premiums, using the policy's cash value as loan collateral. Upon death, the death benefit repays the loan with interest, and remaining proceeds still generate substantial net estate tax savings compared to traditional ownership.

Author: Michael Stratford;

Source: harbormall.net

When to Consider an ILIT Strategy

An ILIT strategy estate plan makes sense only in specific circumstances. The costs and complexity outweigh benefits for many families.

High net worth estates confronting current or anticipated federal estate tax liability represent the core audience. If your assets will exceed exemption amounts and you're purchasing substantial life insurance coverage anyway, structuring that insurance through an ILIT deserves serious consideration. Tax savings frequently dwarf all setup and administration costs combined.

Estate tax exposure thresholds are shifting dramatically. The current historically high exemptions expire December 31, 2025. Beginning January 1, 2026, exemptions drop to approximately $7 million per person adjusted for inflation—roughly half the current levels. Families comfortably within safe territory today may suddenly face exposure. Establishing an ILIT now locks in estate tax benefits before the reversion occurs.

Business succession planning frequently involves life insurance funding buy-sell agreements between partners or shareholders. A $10 million business with insurance-funded buyout agreements adds $10 million to your taxable estate under traditional ownership. Holding those same policies in an ILIT removes that entire amount from estate tax calculations while still providing the liquidity your business partners need.

Special needs beneficiaries require extraordinary care in planning to preserve eligibility for means-tested government benefits like Supplemental Security Income or Medicaid. Direct inheritance can disqualify beneficiaries from crucial support programs. An ILIT can hold proceeds in a supplemental needs trust structure, providing quality-of-life enhancements without jeopardizing benefit eligibility.

Second marriages create natural tension between providing for a surviving spouse and protecting inheritances for children from prior relationships. Without careful planning, your second spouse might inherit everything and eventually leave it all to their own children, completely disinheriting yours. An ILIT can fund a lifetime income stream for your spouse while guaranteeing principal eventually transfers to your biological children.

Setting Up an Irrevocable Life Insurance Trust

Establishing an ILIT properly requires moving through specific steps in sequence, with attention to technical details.

Draft comprehensive trust documents working with an attorney who regularly handles insurance trusts, not just general estate planning. The documents must address beneficiary designations, distribution schedules, trustee authority, Crummey withdrawal mechanics, and contingency provisions for changed circumstances. Off-the-shelf templates miss crucial provisions specific to your family dynamics and financial situation. Quality drafting typically costs $2,500 to $7,500 depending on complexity, trust size, and geographic location.

Select an appropriate trustee who understands the significant responsibilities involved and will remain committed for decades. Adult children frequently serve in this role, though they must demonstrate enough responsibility and organizational skill to handle annual Crummey notices, premium payments, and detailed recordkeeping. Trusted friends sometimes serve effectively. Corporate trustees—banks or trust companies—charge higher fees (commonly 0.5% to 1.5% of trust assets annually) but provide institutional continuity, professional expertise, and eliminate family conflicts of interest.

Acquire insurance coverage through the trust as original owner when possible. The trustee applies for coverage in the trust's name, completes underwriting requirements, and the policy issues with the trust listed as owner and beneficiary from day one. For existing policies you want to transfer, you execute an absolute assignment to the trustee, but remember this triggers the three-year lookback period.

Fund the trust each year by making gifts that match premium obligations. You write checks payable to the ILIT—never directly to the insurance company. The trustee deposits your gift into the trust's bank account, waits for the Crummey notice period to expire, then remits premium payment to the carrier.

Distribute annual Crummey notices without fail every single year you make contributions. Missing even one notice can cause the IRS to disqualify your annual exclusion, triggering gift tax consequences or reducing your lifetime exemption. Trustees should establish tickler systems, calendar reminders, and retain proof of delivery through certified mail or email read receipts.

Author: Michael Stratford;

Source: harbormall.net

Common ILIT Mistakes to Avoid

Even sophisticated planners sometimes stumble into these pitfalls.

Retaining ownership incidents represents the most catastrophic error. Serving as your own trustee, naming your estate as beneficiary, or preserving rights to borrow against cash value causes the IRS to include death benefits in your taxable estate under Section 2042. Complete separation between you and policy ownership is non-negotiable.

ILIT vs. Other Estate Planning Tools

Selecting the optimal wealth transfer strategy requires understanding how different tools compare:

| Strategy | Estate Tax Treatment | Control After Setup | Creditor Protection | Probate Avoidance | Complexity/Cost |

| ILIT | Death benefits completely excluded | Zero control; permanent | Excellent in most jurisdictions | Yes, bypasses entirely | High; $3K–$7K drafting plus ongoing trustee expenses |

| Revocable Living Trust | All assets included in taxable estate | Complete control; modify anytime | Minimal to none | Yes, avoids probate | Moderate; $1K–$3K setup |

| Direct Life Insurance Ownership | Full death benefit in taxable estate | Total control over policy | Limited; state-dependent | Avoids probate with named beneficiary | Minimal; no trust expenses |

| Family Limited Partnership | Gifted interests included at discounted value | General partner maintains management control | Strong asset protection | No, interests pass through probate | High; $5K–$15K setup plus annual filings |

Improper premium payments occur when grantors send checks directly to insurance carriers rather than gifting cash to the trust first. This shortcut bypasses required Crummey notices and disqualifies the annual exclusion. The correct sequence always runs: gift to trust, Crummey notices sent, waiting period expires, trustee pays premium.

Poor trustee selection creates administrative disasters. Choosing someone who lives across the country, doesn't understand fiduciary duties, or has contentious relationships with beneficiaries leads to missed deadlines, lost paperwork, and family conflicts. Corporate trustees cost more but eliminate these risks entirely.

Insufficient liquidity planning happens when families commit excessive resources to ILIT funding without ensuring the grantor retains adequate assets for their own needs. Money gifted to an ILIT cannot be retrieved if you face unexpected expenses or market downturns. Never fund an ILIT so aggressively that you compromise your own financial security.

Missed annual notices plague even well-intentioned trustees. Life intervenes, reminders get ignored, and suddenly you've made a $50,000 gift that doesn't qualify for exclusions. The IRS shows no sympathy for forgotten deadlines. Automated reminder systems or professional trustee services prevent this expensive oversight.

This comparison highlights the fundamental ILIT tradeoff: you sacrifice flexibility and simplicity in exchange for superior estate tax treatment and asset protection. Families needing ongoing control or facing minimal estate tax exposure often find revocable trusts or direct ownership more appropriate. But when estate tax liability is certain and wealth preservation is paramount, ILIT trust benefits typically outweigh alternatives.

When clients bring estates exceeding $15 million, I don't present ILITs as optional—they're foundational. The convergence of estate tax savings, creditor protection, and controlled distributions creates wealth preservation that no single alternative can replicate. Success hinges on precise implementation and maintaining disciplined annual compliance with Crummey notices and proper funding protocols

— Michael Chen

Frequently Asked Questions About Insurance Trust Planning

Committing to irrevocable life insurance trust planning represents a significant decision involving substantial money, ongoing time investments, and permanent restrictions on your flexibility. The irrevocable structure means you're making binding decisions about significant assets, and the administrative requirements persist for decades without interruption. Yet families confronting meaningful estate tax exposure often find the financial analysis strongly favors this approach.

Work with your estate planning attorney and financial advisor to model specific scenarios. Calculate potential estate tax liability with your current structure versus implementing an ILIT. Include all setup costs and projected maintenance expenses over your expected lifetime. Test different assumptions: What happens if exemptions drop as currently scheduled? How do results change if you live another 30 years compared to 15? What if insurance premiums increase significantly due to health changes or carrier adjustments?

Families extracting maximum value from ILITs share common characteristics: they plan early rather than waiting until health issues complicate underwriting, they fund consistently without skipping years, and they partner with advisors who understand both technical requirements and family dynamics. When you're purchasing substantial life insurance coverage regardless, structuring it through an ILIT from inception adds minimal cost compared to direct ownership but can preserve millions in estate taxes.

Don't allow complexity to deter you from a strategy that might perfectly fit your family's needs. Simultaneously, avoid rushing into an irrevocable commitment without thoroughly understanding the decades-long obligations you're accepting. A properly implemented and maintained ILIT becomes one of the most valuable elements in a comprehensive estate plan—delivering liquidity when your family needs it most, generating substantial tax savings, and providing confidence that your wealth will transfer efficiently to the people and causes you care about most deeply.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.