Mature married couple consulting with an estate planning attorney in a modern office with documents on the desk

QTIP Estate Planning Guide for Married Couples

Content

Content

When you've worked decades to build wealth, you want to ensure your spouse is cared for after you're gone—but you also want control over where your assets ultimately land. A qualified terminable interest property trust offers married couples a powerful tool to accomplish both goals while deferring significant estate tax liability.

QTIP trusts have become essential planning vehicles for second marriages, blended families, and estates large enough to trigger federal or state estate taxes. Understanding how these trusts work, when they make sense, and how to implement them properly can save your heirs hundreds of thousands of dollars while preventing family conflicts over inheritance.

What Is a QTIP Trust and How Does It Work?

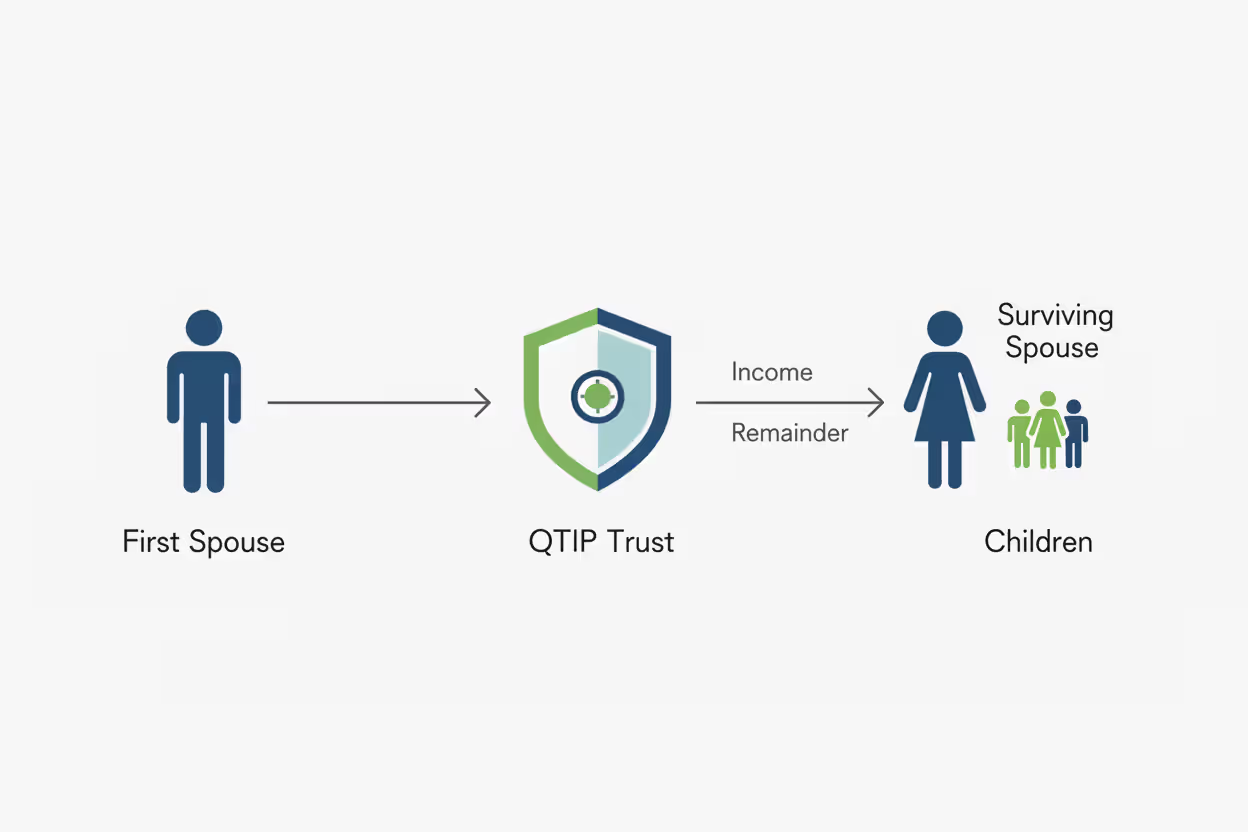

A qualified terminable interest property trust is an irrevocable trust that provides income to a surviving spouse for life while allowing the first spouse to die to control who receives the remaining assets after the survivor's death. The trust qualifies for the unlimited marital deduction, meaning assets transferred into it aren't subject to estate tax when the first spouse dies.

Here's the basic mechanic: Your will or revocable living trust creates the QTIP trust upon your death. The trust must pay all income to your surviving spouse at least annually. Your spouse cannot change the final beneficiaries you've named—typically children from a prior marriage or other family members. When your spouse dies, the remaining trust assets pass to those predetermined beneficiaries and are included in your spouse's taxable estate.

The qualified terminable interest property trust serves spouses who want to provide financial security for their husband or wife without giving up control over the ultimate disposition of their wealth. Your surviving spouse receives steady income and may receive principal distributions if you've authorized the trustee to make them, but cannot redirect your assets to new beneficiaries through their own estate plan.

Consider a remarried widow with adult children from her first marriage and a new husband. Without a QTIP trust, she faces an uncomfortable choice: leave everything to her children and potentially leave her husband without support, or leave assets outright to her husband who might eventually leave everything to his own children. A qtip trust for spouses solves this dilemma by supporting the husband during his lifetime while guaranteeing the widow's children ultimately inherit.

Author: Caroline Ellsworth;

Source: harbormall.net

When QTIP Trusts Make Sense in Your Estate Plan

QTIP trusts aren't necessary for every married couple. They add complexity and ongoing administrative costs, so you need specific circumstances to justify the structure.

Blended families represent the most common scenario. When you have children from a previous relationship, an outright inheritance to your current spouse creates risk. Your spouse could remarry, change their will, or face pressure from their own children. A qtip strategy estate plan ensures your biological children eventually receive your assets while your spouse enjoys financial security.

Significant estate tax exposure makes QTIP trusts valuable even in first marriages. The federal estate tax exemption stands at $13.99 million per person in 2026, but several states impose estate taxes at much lower thresholds. Massachusetts, for example, begins taxing estates above $2 million. A QTIP trust defers federal estate tax until the second spouse dies, potentially allowing both spouses' exemptions to shelter wealth if properly coordinated with other planning techniques.

Asset protection concerns justify marital trust qtip planning when your spouse has creditor risks. If your husband or wife faces potential lawsuits, has guaranteed debts, or works in a high-liability profession, holding assets in a properly structured QTIP trust provides some protection. The trust assets aren't directly owned by your spouse, making them harder for creditors to reach, though protection varies significantly by state law.

Control over generational wealth transfer drives QTIP use among high-net-worth families. When you've built a family business or accumulated substantial investment portfolios, you may want to ensure assets remain in your bloodline or support specific charitable goals. Your spouse receives support, but your vision for the family's financial legacy remains intact.

QTIP trusts generally don't make sense for couples in first marriages with modest estates who trust each other to provide for their mutual children. The administrative burden and professional fees outweigh the benefits when simpler planning achieves your goals.

QTIP Trust Requirements and Tax Benefits

The IRS imposes strict requirements for a trust to qualify as a QTIP and receive marital deduction treatment. Your estate planning attorney must draft the trust carefully to meet these standards.

The trust must pay all income to your surviving spouse at least annually. This is non-negotiable. The trust can pay out more frequently, and the trustee may distribute principal if you've authorized it, but your spouse must receive 100% of trust income. "Income" follows state law definitions and trust accounting principles—typically interest, dividends, and rents, but not capital gains.

No one else can receive distributions during your spouse's lifetime. Your children or other remainder beneficiaries cannot access trust assets until your spouse dies. This requirement ensures the trust genuinely benefits your surviving spouse.

Your executor must make a QTIP election on your estate tax return. Even if the trust document meets all requirements, it doesn't automatically qualify. Your executor files Form 706 and affirmatively elects QTIP treatment for some or all of the trust assets. This flexibility allows partial QTIP elections to optimize tax planning based on your estate's specific circumstances.

The marital deduction eliminates estate tax when the first spouse dies. Assets transferred to a properly elected QTIP trust qualify for the unlimited marital deduction, meaning they pass to the trust estate-tax-free regardless of value. This defers tax until the surviving spouse's death.

Federal Estate Tax Implications

The QTIP trust defers federal estate tax but doesn't eliminate it. When your surviving spouse dies, the full value of the QTIP trust assets—as of their date of death—is included in their taxable estate. If markets have performed well, the tax bill could be substantial.

One significant advantage: your spouse's estate receives a step-up in basis for QTIP trust assets. If you funded the trust with stock purchased at $50 per share that's worth $200 when your spouse dies, the beneficiaries' basis becomes $200. They can sell immediately without capital gains tax.

The QTIP trust's inclusion in your spouse's estate allows their personal exemption to shelter some or all of the trust value. In 2026, each person can pass $13.99 million estate-tax-free. If your spouse has minimal personal assets, their exemption might cover the entire QTIP trust, resulting in zero estate tax at the second death.

State-Level Considerations

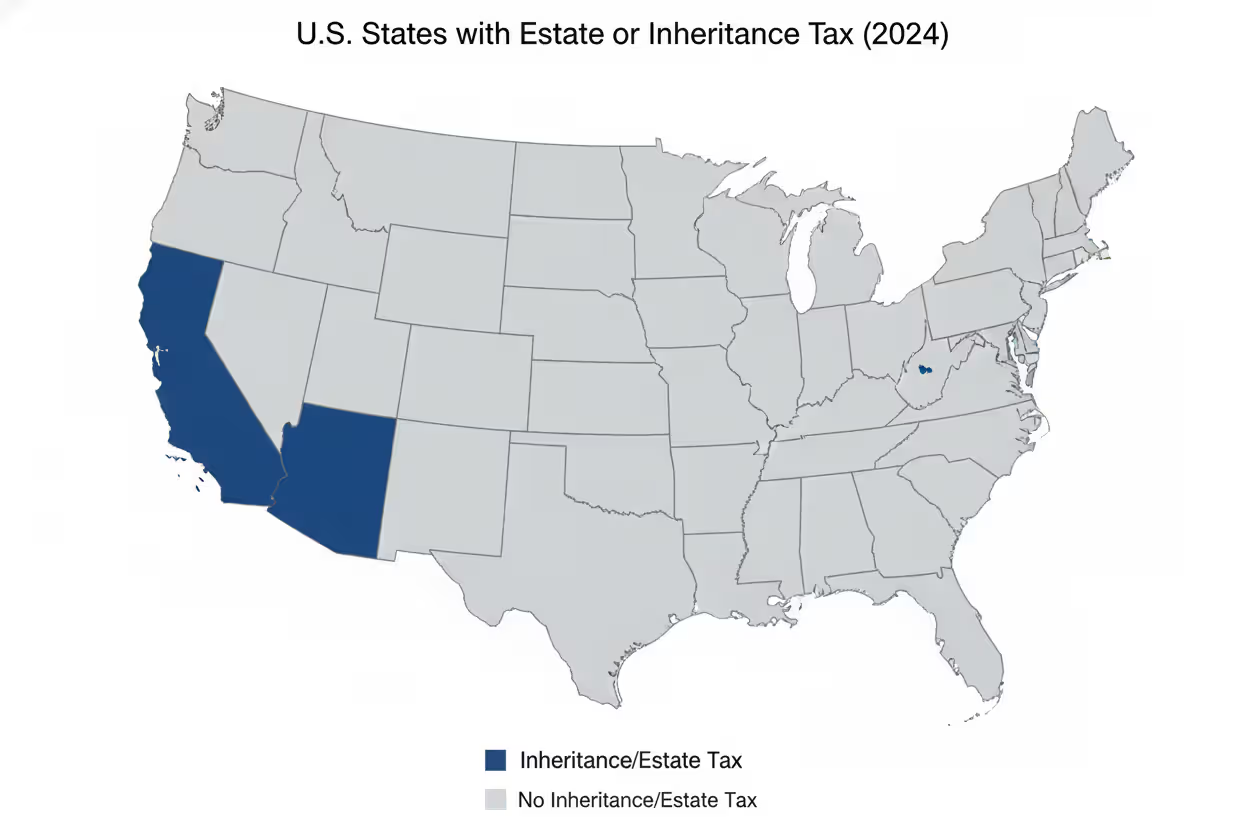

Seventeen states and the District of Columbia impose their own estate or inheritance taxes in 2026, many with exemptions far below the federal level. Connecticut, Maine, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, and others tax estates starting between $1 million and $5.9 million.

QTIP trusts receive the marital deduction for state estate tax purposes in most states, but you need to verify local law. Some states impose inheritance taxes on transfers to beneficiaries based on their relationship to the deceased—QTIP trust distributions to stepchildren might face higher tax rates than distributions to biological children in these jurisdictions.

If you and your spouse live in different states or own property in multiple states, situs rules become complex. Where the trust is administered, where the trustee resides, and where assets are located all affect state tax treatment. Professional guidance is essential for multi-state situations.

Author: Caroline Ellsworth;

Source: harbormall.net

How to Set Up a QTIP Trust

Creating a qtip trust estate planning structure requires careful coordination among several moving parts.

Selecting the right trustee is your first critical decision. Many people name their surviving spouse as co-trustee alongside an adult child or professional trustee. This gives your spouse some control while ensuring an independent party protects the remainder beneficiaries' interests. Naming your spouse as sole trustee can work but creates potential conflicts when distribution decisions affect how much remains for the children.

Corporate trustees—banks or trust companies—provide professional management and impartiality but charge annual fees typically ranging from 0.5% to 1.5% of trust assets. Individual trustees work for smaller fees or free if they're family members, but may lack investment expertise or time to manage the trust properly.

Drafting precise trust language determines how much flexibility your spouse and trustee will have. You must decide whether the trustee can distribute principal to your spouse, and if so, under what standards. Common approaches include:

- Income only (trustee cannot touch principal under any circumstances)

- Principal for health, education, maintenance, and support (HEMS standard)

- Principal for comfort and welfare (broader discretion)

- Specific purposes like medical emergencies or home maintenance

Broader standards give your spouse more financial security but leave less certainty for remainder beneficiaries. You're balancing competing interests of people you care about.

Funding the trust happens automatically at your death if you've structured your estate plan correctly. Your will or revocable trust includes a "QTIP funding formula" that directs your executor to allocate specific assets to the QTIP trust. You might fund it with your investment portfolio, business interests, real estate, or a combination.

Life insurance creates efficient QTIP trust funding. A $2 million policy on your life can fund the trust with liquid assets, avoiding the need to sell real estate or business interests to provide your spouse with income-producing property.

Author: Caroline Ellsworth;

Source: harbormall.net

Coordination with your overall estate plan prevents gaps and conflicts. Your QTIP trust doesn't exist in isolation. You need to consider how it interacts with:

- Retirement account beneficiary designations (IRAs and 401(k)s have special rules for trust beneficiaries)

- Life insurance beneficiaries

- Joint property with rights of survivorship

- Assets with transfer-on-death designations

- Any bypass or credit shelter trusts you're creating

Many people inadvertently undermine their QTIP trust by leaving major assets directly to their spouse through beneficiary designations, defeating the purpose of the trust.

QTIP Trust vs. Other Marital Trust Options

Married couples have several options for structuring inheritance. Understanding the differences helps you choose the right approach.

| Feature | QTIP Trust | Bypass Trust | Outright Inheritance | General Marital Trust |

| Tax Treatment | Marital deduction at first death; included in surviving spouse's estate | Uses first spouse's exemption; not in surviving spouse's estate | Marital deduction; surviving spouse owns assets outright | Marital deduction; included in surviving spouse's estate |

| Control Over Final Beneficiaries | First spouse controls | First spouse controls | Surviving spouse controls completely | Surviving spouse typically controls |

| Income Rights | Surviving spouse must receive all income | Trustee discretion (spouse may or may not receive income) | Spouse receives everything | Spouse usually receives income |

| Flexibility | Low (irrevocable at first death) | Low (irrevocable at first death) | High (spouse can do anything) | Medium (depends on trust terms) |

| Best For | Blended families; estate tax deferral with control | Using first spouse's exemption; asset protection | First marriages; simple estates; complete trust | Providing management for spouse who doesn't want financial responsibility |

Bypass trusts (also called credit shelter trusts) use the first spouse's estate tax exemption to shelter assets from tax at both deaths. If you die in 2026 with a $14 million estate, a bypass trust can hold $13.99 million outside your spouse's taxable estate while a QTIP trust holds the remainder. This "AB trust" planning maximizes tax savings for wealthy couples.

Outright inheritance offers maximum simplicity and flexibility. Your spouse inherits everything, owns it completely, and can spend, invest, or give it away as they choose. This works well when you're confident your spouse will provide for your mutual children and you don't have estate tax concerns.

General marital trusts provide management assistance without the control features of a QTIP. Your spouse might be the beneficiary of a discretionary trust that doesn't require income distributions and doesn't qualify for the marital deduction. These trusts use your estate tax exemption like a bypass trust but focus on benefiting your spouse.

Common QTIP Trust Mistakes to Avoid

Even well-intentioned QTIP planning can fail due to technical errors or poor execution.

Author: Caroline Ellsworth;

Source: harbormall.net

Failing to make the QTIP election on the estate tax return is surprisingly common. Your executor must file Form 706 and explicitly elect QTIP treatment, even if your estate is below the filing threshold. Missing this election means the trust doesn't qualify for the marital deduction, potentially triggering unnecessary estate tax. The IRS rarely grants relief for missed elections, so this mistake can cost hundreds of thousands of dollars.

Improper income distributions violate QTIP requirements. The trustee must distribute all trust income at least annually. Some trustees mistakenly accumulate income in the trust or distribute only what the spouse requests. Either approach disqualifies the trust. The trust document should require mandatory annual distributions and the trustee must follow through.

Trustee conflicts of interest create ongoing problems. Naming your children from a first marriage as trustees puts them in direct conflict with your current spouse. They benefit when trust assets are preserved; your spouse benefits when more is distributed. This tension leads to disputes, litigation, and family estrangement. An independent trustee or corporate fiduciary reduces conflict even though it adds cost.

Poor investment allocation reduces income for your spouse. QTIP trusts must generate income, but modern portfolio theory emphasizes total return (growth plus income) over income alone. A portfolio of 100% dividend stocks produces income but may underperform a balanced portfolio. Trustees should consider "unitrust" provisions that redefine income as a percentage of trust value, allowing more flexible investment management.

Ignoring retirement account rules creates tax disasters. Naming a QTIP trust as beneficiary of your IRA triggers complex rules. The trust must be a "see-through" trust meeting specific IRS requirements, or your IRA must be distributed within five years, accelerating income tax. Most QTIP trusts can qualify, but your attorney must draft carefully and coordinate with your IRA custodian.

Failing to coordinate beneficiary designations undermines the entire plan. If your QTIP trust is supposed to hold $3 million but you've named your spouse as direct beneficiary of a $2 million IRA and $500,000 life insurance policy, only $500,000 actually funds the trust. Your children receive far less than you intended. Every beneficiary designation must align with your overall estate plan.

The biggest misconception about QTIP trusts is that they're only for the ultra-wealthy. I see middle-income couples with $2-3 million in assets who desperately need QTIP planning because of blended family situations, but they assume trusts are only for the rich. Meanwhile, some $20 million estates use QTIP trusts unnecessarily when the spouses completely trust each other and have only mutual children. The decision should be driven by family dynamics and control objectives, not just net worth

— Margaret Chen

Frequently Asked Questions About QTIP Estate Planning

QTIP estate planning offers married couples a sophisticated tool to balance competing priorities: providing financial security for a surviving spouse while maintaining control over ultimate asset distribution. For blended families, the qualified terminable interest property trust solves the seemingly impossible challenge of supporting your current spouse without disinheriting children from a prior relationship.

The tax benefits—deferring federal estate tax until the second death while qualifying for the unlimited marital deduction—can save families hundreds of thousands of dollars when estates exceed exemption thresholds. Combined with bypass trusts and other advanced techniques, marital trust qtip planning maximizes the use of both spouses' estate tax exemptions.

Success requires meticulous execution. Your attorney must draft trust language that meets strict IRS requirements, your executor must make the QTIP election on your estate tax return, and your trustee must distribute all income annually while managing investments prudently. Coordination with beneficiary designations, retirement accounts, and your overall estate plan prevents gaps that undermine your intentions.

QTIP trusts aren't appropriate for everyone. The administrative burden, ongoing costs, and inflexibility make them unnecessary for many couples. But when family dynamics demand that you provide for your spouse while protecting your children's inheritance, or when estate tax deferral offers significant savings, a well-designed qtip strategy estate plan delivers peace of mind that your wealth will support the people you love in the order and manner you've chosen.

Working with an experienced estate planning attorney who understands both the technical tax requirements and the family dynamics at play ensures your QTIP trust accomplishes your goals without creating unintended consequences. The investment in proper planning pays dividends for generations.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.