Wooden desk with legal documents, fountain pen, eyeglasses, and small house model in warm natural lighting

What Is Trust Estate Planning and How Does It Work

Content

Content

About 67% of Americans haven't created even basic estate planning documents. That's a problem. When someone dies without a plan, the state decides who gets what—and it's rarely what the deceased would have wanted.

Here's what makes trust estate planning different from just writing a will: you're setting up a legal structure that works for you right now, not just after you're gone. A will sits in a drawer until you die, then goes through months of court oversight. A trust? It can hold your house, your investment accounts, and your business interests starting today, managing everything smoothly when you're alive, if you become unable to handle your own affairs, and after you pass away.

Most people who plan ahead stop at drafting a will. They check the box, feel accomplished, and never realize they've left their family facing six to eighteen months of probate court, public records that show every asset they owned, and legal fees that could have been avoided entirely.

Learning exactly what trusts can and can't do helps you decide whether one belongs in your planning—and which type makes sense for your situation.

Understanding Trusts in Estate Planning

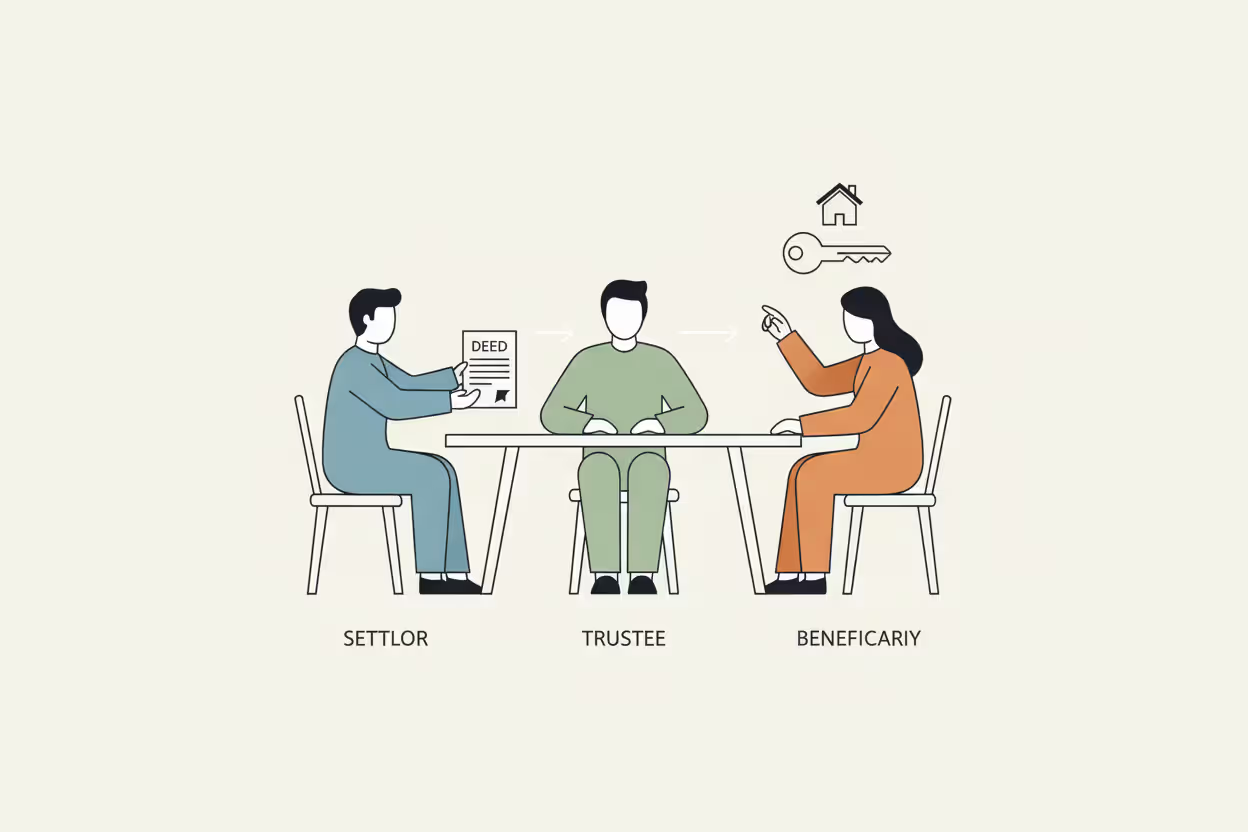

Picture three people sitting around a table. The first person (you, the grantor) owns a rental property worth $400,000. You sign papers transferring that property to the second person (the trustee), who now legally owns it but must manage it exactly according to your written instructions. The third person (your daughter, the beneficiary) will eventually receive the rental income or the property itself.

That's a trust in its simplest form—one person controls assets for another person's benefit, following specific rules the original owner set up.

When someone searches "what is a trust estate planning," they're usually asking whether they actually need one or if their will covers everything. The short answer: wills and trusts do different jobs. Your will tells the probate judge what you want to happen with your stuff. The judge reviews it, validates it, oversees the distribution, and keeps everything on public record. Trusts work privately, outside the courtroom entirely.

The trustee you appoint must follow something called fiduciary duty. In plain English, this means they legally have to put the beneficiaries' interests first—not their own. They can't use trust money to buy themselves a boat or make risky investments that benefit them personally. If they do, beneficiaries can sue them.

You might name yourself as the initial trustee of your own trust. Sounds circular, but it works perfectly. You maintain complete control while you're healthy and capable, then your chosen successor steps in if something happens to you. That successor could be your spouse, your adult child, your CPA, or a trust company—whoever you trust to follow your instructions.

Author: Jonathan Whitmore;

Source: harbormall.net

Every state has different rules about how trusts operate. Florida handles things differently than California. Texas has different requirements than New York. The core concept stays the same nationwide: assets move into the trust's legal ownership, the trustee manages them, and beneficiaries receive the benefits according to the trust document's terms.

Common Types of Trusts for Estate Planning

Walk into an estate attorney's office and mention you want a trust, and they'll ask you a dozen questions before recommending a specific type. Your age, your assets, your family situation, and your concerns all point toward different trust structures.

Revocable Living Trusts work for probably 80% of people reading this. You create it today, move your assets into it, and serve as your own trustee. Nothing changes in your daily life—you still control everything, make all the decisions, buy and sell assets freely. The magic happens later: when you die, your successor trustee immediately takes over and distributes everything according to your instructions. No probate judge. No six-month waiting period. No public filing showing what you owned. You can change this trust anytime you want, cancel it completely, or rewrite the whole thing.

The catch? Because you control everything, the IRS doesn't see this as separate from you. No tax benefits. Creditors can still reach these assets. But for basic planning—avoiding probate, handling incapacity, keeping things private—it's perfect.

Irrevocable Trusts require you to permanently give up ownership. Transfer your vacation home into one of these, and you can't just change your mind next year and take it back. Sounds terrible, right? But wealthy families use them constantly because assets genuinely leave your estate. Estate taxes can't touch them. Most creditors can't reach them. If you need Medicaid to pay for nursing home care in ten years, that vacation home won't count against you (if you set things up correctly).

Life insurance policies work brilliantly in irrevocable trusts. You transfer a $2 million policy into the trust, the trust owns it, and that $2 million doesn't get counted in your taxable estate when you die. For families worried about the estate tax threshold, that's gold.

Testamentary Trusts get created through your will, so they only spring into existence after you die. They don't help you avoid probate—everything still goes through court. But they're fantastic for controlling when and how your kids receive their inheritance.

Example: Your will creates a trust for your 16-year-old son. Instead of handing him $500,000 cash at 18, the trust pays for his college, gives him a monthly allowance, matches any income he earns from employment, and distributes the principal in three chunks—$100,000 at 25, $150,000 at 30, and the remainder at 35. You're parenting from beyond the grave.

Special Needs Trusts solve a specific problem. Your sister receives disability benefits and Medicaid. You want to leave her $200,000, but if she inherits it directly, she'll lose her benefits until the money runs out. A special needs trust holds that $200,000, pays for things government benefits don't cover (music lessons, vacations, a better wheelchair, a companion), and she keeps her benefits. It's the only way to leave money to someone on means-tested government assistance without hurting them.

Author: Jonathan Whitmore;

Source: harbormall.net

Dozens of other trust types exist—charitable remainder trusts that pay you income for life then donate the principal, spendthrift trusts that protect beneficiaries from their own poor financial decisions, dynasty trusts that last for generations. The trust type you need depends on what you're trying to accomplish.

Why People Use Trust and Estate Planning Together

Combining trusts with wills, powers of attorney, and healthcare directives creates overlapping protection. Each document handles something the others can't.

Avoiding probate saves money and time, period. Probate in California costs around 4% of the estate value in statutory attorney fees alone, plus court costs and delays. A million-dollar estate pays $23,000 to the attorney and another $23,000 to the executor just in statutory fees—before adding actual hourly work. In Texas, probate might cost much less but still takes eight months minimum. Assets in a properly funded trust skip all of this. Your trustee can write checks to beneficiaries the week after your funeral.

Privacy matters more in some families than others. When court files become public record, everyone sees what you owned, what you owed, and who got what. That public information attracts scammers who target grieving widows, salespeople who know someone just inherited money, and family members crawling out of the woodwork looking for a piece. Trust administration happens entirely in private. Only the people you choose to tell will know anything about your assets.

Protecting assets from lawsuits works through irrevocable structures. Doctors, real estate developers, business owners—anyone worried about being sued—often put assets into irrevocable trusts years before problems arise. Once assets are legitimately in the trust and enough time has passed, plaintiffs usually can't touch them. Timing matters enormously here. Transfer everything to a trust the day after someone sues you, and the court will reverse the transfer as fraudulent. Do it five years before any problems emerge, and you're generally protected.

Controlling distributions lets you parent adult children or protect vulnerable family members. Your 28-year-old son has struggled with addiction. Leaving him $300,000 cash could kill him. A trust managed by your daughter can pay for his rent, groceries, and rehab—but never give him direct access to large sums. Or your daughter married someone you don't trust. A trust can ensure your inheritance benefits her and your grandchildren without becoming marital property in a divorce.

Tax planning only kicks in for estates exceeding federal thresholds. The exemption for 2025 is $13.99 million per person, $27.98 million for married couples. Most families don't face federal estate taxes. But twelve states impose their own estate taxes, and some start at just $1 million (Oregon and Massachusetts). For families in those states or above federal limits, various irrevocable trust strategies can save hundreds of thousands in taxes.

Incapacity protection is underrated. Stroke, dementia, car accidents—any of these can leave you alive but unable to manage your finances. Without a trust, your family must petition the court to appoint a conservator, attend hearings, post bonds, and file annual accountings. With a trust, your successor trustee simply takes over based on doctor's letters confirming your incapacity. No court. No public proceeding. No delays.

Estate and trust planning work in tandem because documents serve different purposes. Your trust manages most assets. Your will names guardians for minor kids and catches anything not in the trust. Your power of attorney authorizes someone to handle non-trust matters. Your healthcare directive addresses medical decisions. Together, they cover all scenarios.

How to Set Up a Trust for Estate Planning

Creating an effective trust requires more than filling out forms. Rush it, and you'll miss critical details that cause problems later.

Identify exactly what concerns you. Write them down. "I don't want my ex-husband getting any inheritance meant for my daughter." "My son is terrible with money." "Probate tied up my mother's estate for fourteen months and I won't do that to my kids." "We own property in three states and I've heard probate in each state costs a fortune." These specific concerns guide every decision about trust structure and terms.

Pick the right trust structure based on those concerns. Most people default to a revocable living trust and stop there. Sometimes that's perfect. Sometimes you need additional specialized trusts for specific assets or purposes. An estate attorney can map your concerns to appropriate trust types, but you need to clearly communicate your situation. Don't leave out details about family dynamics, asset types, or future plans because you think they're not relevant—mention everything and let the attorney decide what matters.

Selecting a trustee deserves serious thought. Your oldest son loves you and means well, but if he's disorganized, late on his own bills, and has never managed investments, maybe he's not the right choice. Your daughter is financially savvy but lives overseas and travels constantly—can she handle the administrative work? Sometimes naming co-trustees makes sense: a responsible family member who knows your wishes paired with a professional who handles the technical and financial aspects.

Professional trustees (banks, trust companies) charge fees—typically 1% to 1.5% of assets annually—but they don't die, don't play favorites among beneficiaries, don't make emotional decisions, and know the legal requirements. For a $2 million trust lasting twenty years for minor children, that expertise might be worth the cost.

Author: Jonathan Whitmore;

Source: harbormall.net

Have an experienced estate attorney draft the document. Not a real estate lawyer who does estate planning on the side. Not online software. Not a paralegal service. Estate planning specialists stay current on tax law changes, state statute updates, and new case law affecting trusts. They ask questions that uncover issues you'd never consider.

The trust document needs precision. Vague language like "distribute fairly among my children" leads to sibling battles and litigation. Specific terms prevent problems: "divide the remaining trust assets into three equal shares, one for each of my children, with each child's share distributed to them outright upon reaching age 30."

Funding the trust is where most people fail. You sign the trust document, pay the attorney, and feel finished. You're not. The trust owns nothing until you transfer assets into it. An empty trust is worthless.

For your house, the attorney prepares a new deed showing the trust as owner. You sign it, get it notarized, and record it at the county recorder's office. Cost: usually $50 to $150 in recording fees. Time: one week.

For bank accounts, call the bank or visit a branch. They'll have forms to either retitle the account in the trust's name or make the trust the payable-on-death beneficiary (slightly different approaches; ask your attorney which they prefer). Time: could be same-day, could take two weeks depending on the institution.

Investment accounts follow similar processes, but brokerage firms each have their own procedures. Some make it easy with one form. Others require multiple signatures, medallion guarantees, and confusing bureaucracy. Start the process early and follow up regularly.

Business interests, vehicles, boats, artwork, patents—every asset type has its own transfer process. Create a spreadsheet listing everything you own and check items off as you complete transfers.

Coordinate with related documents. Your will should include "pour-over" language that catches any assets you forget and transfers them to the trust through probate (not ideal, but better than nothing). Update beneficiary designations on life insurance and retirement accounts—sometimes naming the trust works, sometimes naming individuals makes more sense depending on your goals and tax implications. Execute powers of attorney for finances and healthcare to handle situations the trust doesn't cover.

Plan to review every few years. Divorce, remarriage, births, deaths, cross-country moves, selling your business, acquiring rental properties—all these require trust updates. Set a calendar reminder for every three years to review with your attorney, and contact them immediately after major life changes.

Trust Estate Planning Costs and Timeline

Money and time—let's talk specifics.

Attorneys in small towns might charge $2,000 for a complete estate plan with a revocable living trust. Big-city attorneys in expensive markets charge $4,000 to $6,000 for the same work. Both include the trust, a will, healthcare power of attorney, and financial power of attorney.

Complex situations cost more. Multiple marriages? Add $1,500. Own three rental properties and a small business? Add another $2,000. Need tax planning for an $8 million estate? You're looking at $8,000 to $15,000 for sophisticated planning with irrevocable trusts and advanced tax strategies.

Some attorneys charge flat fees. You know upfront exactly what you'll pay. Others bill hourly—anywhere from $250 per hour in lower-cost areas to $600+ per hour in major metropolitan markets for experienced specialists. Get a written fee agreement before work begins. Ask about payment plans if the full amount upfront creates hardship.

Beyond attorney fees, expect $75 to $200 per property for deed recording. Each county charges different fees. Financial institutions rarely charge for retitling accounts, though a few still do—call ahead and ask. Notary fees run $10 to $25 per document (your attorney's office usually has a notary).

Ongoing costs for a revocable living trust you manage yourself: zero. You don't file separate tax returns. No annual fees. Nothing until you die or become incapacitated, when your successor trustee takes over and might charge fees (or serve for free if it's a family member).

Professional trustees charge annual fees—1% to 2% of trust assets is standard, with minimums around $3,000 to $5,000 annually. A $500,000 trust might cost $5,000 per year for professional management. A $5 million trust might cost $60,000 annually. Family members often serve without compensation, though they're entitled to reasonable fees under most trust documents.

Irrevocable trusts require annual tax filings if they earn more than $600 in income. Tax preparation for simple irrevocable trusts costs $500 to $1,000. Complex trusts with multiple assets and tax issues can run $2,000 to $5,000 annually for accounting and tax work.

Timeline from start to finish typically spans six to ten weeks for straightforward situations. Week one: initial consultation where you explain your situation and goals. Weeks two through four: attorney drafts documents, sends them to you for review, makes revisions based on your feedback. Week five: you sign everything, usually at the attorney's office with witnesses and notary present. Weeks six through ten: you work on funding the trust, retitling assets, changing beneficiary designations.

Author: Jonathan Whitmore;

Source: harbormall.net

Real estate transfers happen quickly—sign the deed, record it, done within a week. Financial accounts take longer. Some banks process trust retitling in three days. Others take four weeks. Brokerage firms average two weeks. Business interest transfers might need additional legal work, adding time.

The funding phase determines how quickly your trust actually protects you. An unfunded trust sitting in your drawer while you "get around to" transferring assets helps nobody.

Mistakes to Avoid in Estate and Trust Planning

People make predictable mistakes. Here's what to watch for.

Creating a trust but never funding it tops the list. Estate attorneys report that somewhere between 30% and 50% of the trusts they draft never get funded. Clients sign the papers, pay the bill, put the documents in a safe, and just... never transfer anything. They die five years later and everything goes through probate exactly as if the trust never existed. The trust owns nothing, so it does nothing.

Why does this happen? Life gets busy. The signing ceremony feels like completion. Retitling assets seems tedious. People procrastinate. Block out three full days within two weeks of signing to handle the funding process. Make it a priority, not something you'll "get to eventually."

Choosing a trustee based on fairness rather than capability creates disaster. "I named all three kids as co-trustees so nobody would feel left out." Now every decision requires three people to agree, one lives in Japan, one hates the other two, and nothing gets done for months at a time. Pick the most capable, responsible, organized person even if it upsets others. This isn't about feelings—it's about who can actually do the job.

Naming minor children as direct beneficiaries on life insurance or retirement accounts defeats your careful trust planning. Life insurance companies will gladly name "Billy Smith, age 6" as beneficiary. Then you die, Billy can't legally own $500,000, and the court appoints a conservator to manage it until he turns 18, at which point he gets the entire amount in cash. That's exactly what your trust was designed to prevent. Name the trust as beneficiary instead (or name the child but have the trust as contingent beneficiary—discuss with your attorney).

Ignoring the plan after creation means your trust reflects your life in 2025 but it's now 2040 and everything has changed. You got divorced and remarried—does your trust still leave everything to your ex? Your daughter gave you two grandchildren—shouldn't they be included? You moved from California to Florida—does your trust comply with Florida law? You sold your business and bought rental properties—are they in the trust? Review and update regularly or your plan becomes outdated and ineffective.

Using online forms or DIY software works for some simple situations and creates expensive problems in others. Generic forms don't know that your state requires specific language for durable powers of attorney. They can't ask whether your second marriage and kids from a previous relationship create planning issues. They don't warn you that naming your trust as IRA beneficiary might trigger income tax acceleration. A $3,000 DIY trust that creates $100,000 in tax problems or family litigation wasn't a bargain.

Forgetting to update beneficiary designations leaves assets passing to the wrong people. Your trust says everything goes to your current spouse, but your 401(k) still names your ex-husband from fifteen years ago. The 401(k) beneficiary designation wins—your ex gets the retirement account. Pull out every account statement you have, check every beneficiary designation, and update anything that doesn't align with your current wishes.

Mixing up retirement account rules causes unnecessary taxes. Retirement accounts follow special rules that changed significantly with the SECURE Act. Naming a trust as IRA beneficiary sometimes makes perfect sense (control, creditor protection) and sometimes triggers accelerated taxation (losing stretch IRA benefits). This requires coordination between your estate attorney and financial advisor—don't guess.

Overlooking digital assets leaves accounts, photos, cryptocurrency, and online businesses inaccessible. Your trustee needs to know about your Coinbase account, your profitable blog, your Etsy store, your digital photo library. Include a separate document (stored securely) with login credentials, account locations, and instructions for accessing everything digital.

I've watched families learn the hard way that signing trust documents and funding the trust are two completely different things. A client once paid $6,000 for sophisticated trust planning, then died three years later without transferring a single asset. His widow asked me why they'd wasted all that money. The trust could have saved them $40,000 in probate costs and eight months of delays—if he'd just spent two weeks retitling his accounts

— Robert Chen

Frequently Asked Questions About Trust Estate Planning

Trust estate planning gives you control over your legacy that simple wills can't match. Yes, it requires upfront investment—money to create it, time to fund it properly, attention to keep it updated. But families who've watched loved ones' estates stuck in probate for a year, seen private financial details become public record, or dealt with incapacitated parents without proper planning understand the value immediately.

Match your trust type to your specific situation. Young couples need different structures than retirees. Business owners face different concerns than employees. Blended families require different planning than first marriages. An experienced estate planning attorney spots issues you wouldn't know to consider and structures everything to accomplish your specific goals.

Start somewhere. Even basic planning beats no planning. Get a solid revocable living trust in place, fund it properly, and refine your approach as life changes. Your family will thank you for the clarity, the smooth transition, and the absence of court battles when something happens to you.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.