A formal legal trust document with a seal and signature on a dark wooden desk next to a fountain pen and reading glasses

What Is a Trust Agreement in Estate Planning

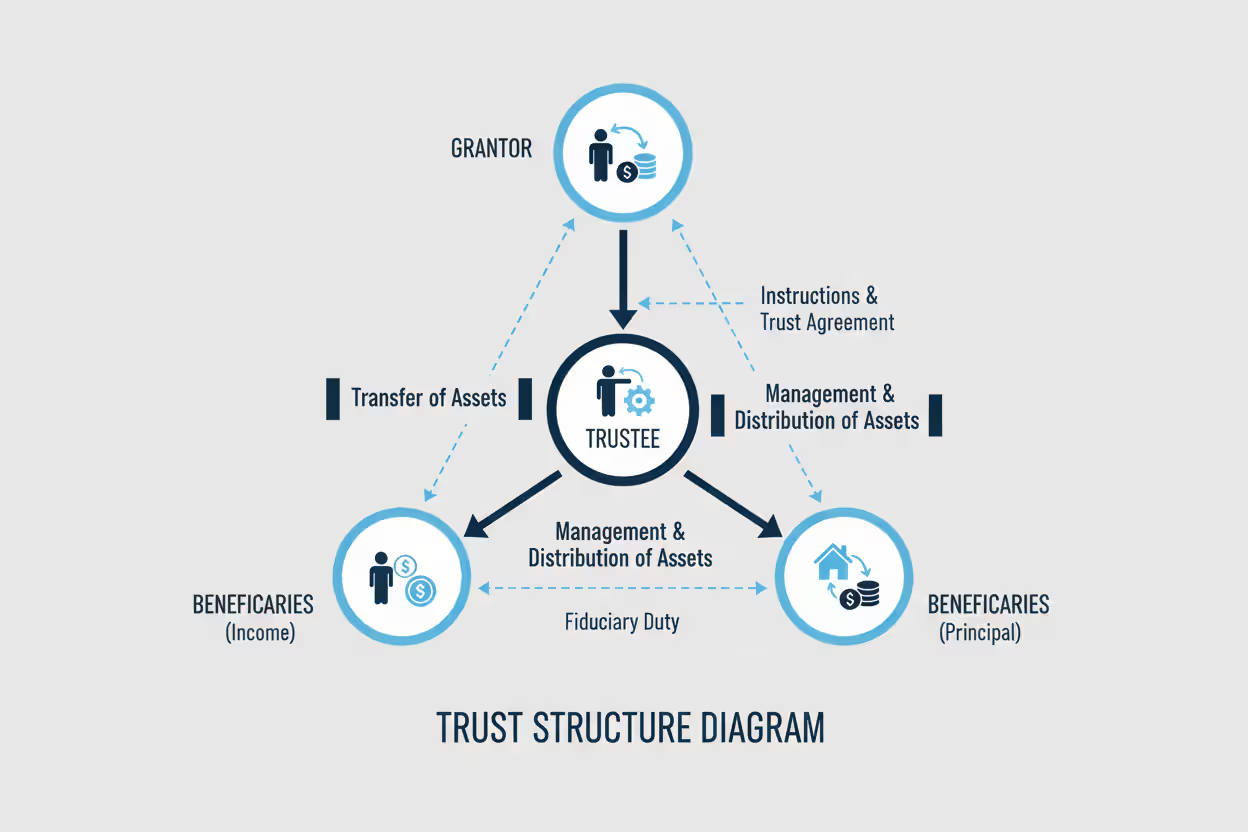

A trust agreement is a legally binding document that creates a fiduciary relationship between three parties: the person who funds the trust (grantor), the person who manages it (trustee), and the people who benefit from it (beneficiaries). This written instrument establishes how assets will be managed, protected, and distributed according to the grantor's wishes, often without the delays and expenses of probate court.

Unlike a simple will that only takes effect after death, a trust agreement can operate during your lifetime and continue working long after you're gone. The agreement spells out every detail—from which assets go into the trust to exactly when and how beneficiaries receive their inheritance. For many families, this document serves as the cornerstone of their estate plan, offering control, privacy, and flexibility that other planning tools can't match.

The trust agreement functions as both an instruction manual and a legal contract. It binds the trustee to follow specific rules when handling trust property, protects beneficiaries' interests, and creates a clear paper trail for accountability. Whether you're setting aside funds for a child's education, protecting a family business, or ensuring a loved one with special needs receives proper care, the trust agreement makes your intentions legally enforceable.

How a Trust Agreement Works

The mechanics of a trust agreement begin when the grantor transfers ownership of assets into the trust's name. This transfer isn't symbolic—it requires retitling bank accounts, real estate deeds, investment portfolios, and other property so the trust legally owns them. Once funded, the trust becomes a separate legal entity with its own tax identification number (for irrevocable trusts) or operates under the grantor's Social Security number (for revocable trusts).

The trustee then manages these assets according to the agreement's terms. If you create a revocable living trust, you typically serve as your own trustee during your lifetime, maintaining complete control over the assets. You can buy, sell, or reorganize trust property as freely as if you still owned it personally. The real power of the trust agreement emerges when you become incapacitated or die—your successor trustee steps in immediately, without court intervention, to manage or distribute assets exactly as you specified.

Author: Rebecca Langford;

Source: harbormall.net

What does a trust agreement do that makes it so valuable? It creates a legally recognized framework that survives your death or incapacity. Courts recognize the trustee's authority to act on behalf of the trust, banks honor the trustee's signature, and beneficiaries can enforce their rights if the trustee fails to follow the agreement's terms. This legal recognition means assets can transfer to heirs without probate, financial accounts remain accessible during emergencies, and your privacy stays intact since trust agreements typically don't become public record.

The agreement also establishes the trustee's fiduciary duty—a legal obligation to act in the beneficiaries' best interests, avoid conflicts of interest, keep accurate records, and follow the trust terms precisely. This duty carries real consequences. Trustees who breach their responsibilities can be sued, removed, and held personally liable for losses they cause through negligence or misconduct.

Key Components of a Trust Agreement

Every trust agreement contains several essential elements that give it legal force and practical utility. The document must clearly identify the grantor, trustee, and beneficiaries by full legal name. It must describe the trust property with enough specificity that anyone reading the agreement understands exactly what assets the trust holds—whether that's "all real property located at 456 Oak Street, Denver, Colorado" or "Account #12345 at First National Bank."

The agreement specifies the trust's purpose, which can range from broad ("to provide for the grantor's descendants") to highly specific ("to pay for of John Smith, who has cerebral palsy"). This purpose guides the trustee's decisions and helps courts interpret ambiguous provisions if disputes arise.

Distribution provisions form the heart of most trust agreements. These clauses explain when and how beneficiaries receive trust assets. Simple trusts might direct the trustee to distribute everything immediately upon the grantor's death. More sophisticated agreements create staggered distributions—perhaps one-third at age 25, another third at 30, and the remainder at 35. Others establish ongoing trusts that pay income to a surviving spouse for life, then distribute the principal to children after the spouse dies.

Amendment and revocation provisions determine whether the grantor can change the trust terms later. Revocable trusts include language preserving the grantor's right to modify or terminate the agreement at any time. Irrevocable trusts either prohibit changes entirely or allow limited modifications under specific circumstances, such as consent from all beneficiaries.

Author: Rebecca Langford;

Source: harbormall.net

Trustee Powers and Responsibilities

The trust agreement grants the trustee specific powers needed to manage trust assets effectively. Standard powers include the authority to invest trust funds, sell or lease real estate, operate a business, hire professionals like accountants or attorneys, and make distributions to beneficiaries. Many agreements incorporate state statutory trust powers by reference, then add custom provisions addressing the grantor's unique assets or family situation.

The trustee must maintain detailed records of every transaction, provide regular accountings to beneficiaries, file tax returns for the trust, and preserve trust assets against waste or loss. When making investment decisions, trustees must follow the "prudent investor rule"—a legal standard requiring them to invest as a careful, skilled person would when managing someone else's money. This doesn't mean avoiding all risk, but rather building a diversified portfolio appropriate for the trust's purposes and the beneficiaries' needs.

Compensation provisions explain how the trustee gets paid. Professional trustees typically charge annual fees based on a percentage of trust assets (often 1-2% for routine management). Family members serving as trustees might receive smaller fees or waive compensation entirely, though the agreement should still authorize reasonable payment for their time and effort.

Beneficiary Rights and Distribution Terms

Beneficiaries hold enforceable legal rights under the trust agreement. They can demand accountings, inspect trust records, and petition courts to remove trustees who breach their duties. The agreement defines these rights precisely—some trusts give beneficiaries broad access to information and liberal distribution rights, while others limit beneficiary involvement to receiving scheduled payments.

Distribution standards vary widely. "Mandatory" distributions require the trustee to pay out income or principal on a fixed schedule, leaving no discretion. "Discretionary" trusts give the trustee authority to decide whether, when, and how much to distribute based on factors like the beneficiary's needs, other resources, or behavior. "HEMS" provisions—allowing distributions for Health, Education, Maintenance, and Support—strike a middle ground, giving trustees flexibility within defined boundaries.

Spendthrift clauses protect beneficiaries from themselves and their creditors. These provisions prevent beneficiaries from selling or pledging their trust interests and shield trust assets from most creditors' claims. If your son struggles with debt or poor financial decisions, a spendthrift trust keeps his inheritance safe until the trustee distributes it according to your timeline.

Trust Agreement vs Trust Document

The terms "trust agreement" and "trust document" mean the same thing in practical usage. Both refer to the written instrument that creates and governs the trust. Some attorneys prefer "trust agreement" because it emphasizes the contractual nature of the arrangement between grantor, trustee, and beneficiaries. Others use "trust document" as a more neutral term that encompasses various trust types.

You might also encounter the phrase "declaration of trust," which technically describes a trust where the grantor and trustee are the same person—common with revocable living trusts. When you create a living trust and name yourself as initial trustee, you're "declaring" that you hold certain property in trust for your beneficiaries. Despite this technical distinction, most people use "trust agreement," "trust document," and "declaration of trust" interchangeably when discussing estate planning trusts.

The confusion often stems from related documents that serve different purposes. A "trust certificate" (also called a "memorandum of trust" or "abstract of trust") is a shortened document that proves the trust exists and identifies the trustee without revealing private details about beneficiaries or distributions. You might show a trust certificate to a bank or title company when conducting trust business, keeping the full trust agreement confidential.

The "trust instrument" is another synonym for the trust agreement—it's simply formal legal language referring to the document that creates the trust. When statutes or court cases mention the "trust instrument," they mean the same written agreement you signed with your attorney.

What matters more than terminology is ensuring your trust document is comprehensive, properly executed, and actually funded with your assets. A trust agreement sitting in a drawer with no assets titled in the trust's name accomplishes nothing.

Author: Rebecca Langford;

Source: harbormall.net

Types of Trust Agreements in Estate Planning

Trust agreements vary significantly based on the type of trust they create. A revocable living trust agreement includes provisions allowing the grantor to amend or revoke the trust at any time. These agreements typically name the grantor as initial trustee and beneficiary, with successor trustees and remainder beneficiaries taking over after the grantor's death or incapacity. The agreement's flexibility makes it popular for basic estate planning, though this same flexibility means the trust offers no asset protection or tax benefits during the grantor's lifetime.

Irrevocable trust agreements permanently transfer assets out of the grantor's control. Once signed and funded, the grantor cannot reclaim the property or change the trust terms without beneficiary consent (if at all). These agreements require more careful drafting because mistakes can't be easily corrected. The payoff comes through estate tax reduction, asset protection from lawsuits, and Medicaid planning benefits that revocable trusts can't provide.

Testamentary trust agreements appear within a will and only take effect after the grantor dies and the will goes through probate. The agreement might establish a trust for minor children, with assets distributing when they reach adulthood, or create a special needs trust for a disabled beneficiary. Because testamentary trusts are part of a will, they become public record during probate—sacrificing the privacy advantage of living trusts.

Special purpose trusts require customized agreement language addressing unique goals. A qualified terminable interest property (QTIP) trust agreement includes specific provisions allowing the estate to claim the marital deduction while controlling where assets go after the surviving spouse dies—essential for blended families. Charitable remainder trust agreements contain calculations ensuring the charity receives the required minimum percentage while paying income to the grantor for life. Special needs trust agreements carefully navigate Medicaid rules to supplement government benefits without disqualifying the beneficiary.

The type of trust you need determines what goes into your trust agreement. An experienced estate planning attorney tailors the document to your specific assets, family situation, and long-term goals rather than using generic forms.

Drafting a Trust Agreement

Creating an effective trust agreement requires more than filling in blanks on a template. The process starts with a detailed conversation about your assets, family dynamics, and estate planning objectives. Your attorney needs to know about your real estate holdings, retirement accounts, business interests, and personal property. They'll ask about your children's ages and maturity levels, any family members with special needs or substance abuse problems, and your concerns about creditors, divorce, or irresponsible spending.

This information shapes every provision in the agreement. If you own rental properties, the trustee powers section must authorize property management and maintenance decisions. If you have a special needs child, distribution provisions must comply with Medicaid rules. If you worry about a son-in-law's influence over your daughter, the agreement might include spendthrift protections and discretionary distribution standards.

Author: Rebecca Langford;

Source: harbormall.net

Experienced estate planning attorneys draft trust agreements from scratch or work from their own carefully refined templates, customizing each provision to fit your situation. They'll explain trade-offs—for example, giving your trustee broad discretion protects against unforeseen circumstances but might create uncertainty for beneficiaries. They'll flag potential problems, like naming co-trustees who might disagree or creating distribution schedules that trigger unnecessary tax consequences.

Common drafting mistakes include vague beneficiary descriptions ("my children" without naming them), insufficient trustee powers (forcing trustees to petition courts for authority to handle routine matters), and contradictory provisions (one section saying the trust is irrevocable, another reserving amendment rights). Poor drafting can also create unintended tax problems, disqualify beneficiaries from government benefits, or leave assets vulnerable to creditors.

Online trust-creation tools have improved significantly, but they work best for straightforward situations—a married couple with adult children, modest assets, and no complicated family dynamics. These platforms can't spot issues they're not programmed to recognize. If you own a business, have substantial wealth, face potential estate tax liability, or deal with blended family complications, the cost of attorney-drafted documents pays for itself through avoided problems.

The drafting process typically takes two to four weeks from initial consultation to signing. Your attorney prepares a draft, you review it and suggest changes, they revise the document, and you meet to sign the final version. Most states require your signature to be notarized, and some require witnesses who aren't beneficiaries. After signing, the critical step is funding the trust—retitling assets into the trust's name. An unfunded trust agreement is like an empty container; it can't accomplish anything until you put assets into it.

When You Need a Trust Agreement

The biggest mistake I see is people who create trust agreements but never fund them.They spend time and money drafting a comprehensive trust, then leave all their assets titled in their individual names. When they die, everything goes through probate anyway because the trust owns nothing. A trust agreement is only as good as the assets you put into it—funding is not optional, it's essential to making the plan work

— Margaret Chen

Trust agreements make sense when probate avoidance matters to you. Probate—the court process for administering estates—can take six months to two years, costs thousands of dollars in legal fees and court costs, and becomes part of public record. A properly funded trust bypasses probate entirely. Your successor trustee distributes assets to beneficiaries weeks after your death, not months or years, and the trust agreement remains private.

Privacy concerns drive many people toward trust-based estate plans. Wills filed with probate courts become public documents that anyone can read. Your nosy neighbor, estranged relatives, or identity thieves can discover exactly what you owned and who inherited it. Trust agreements typically stay private—only the parties involved see the terms.

Asset protection needs justify irrevocable trusts. If you face lawsuit risk from your profession, own rental properties with liability exposure, or want to shield assets from a beneficiary's creditors or divorcing spouse, certain irrevocable trusts place assets beyond creditors' reach. The trust agreement must be carefully drafted to satisfy legal requirements—poorly structured asset protection trusts can be set aside by courts.

Special needs planning requires trust agreements that preserve government benefits. If you have a child receiving Supplemental Security Income or Medicaid, leaving them an inheritance directly disqualifies them from benefits. A properly drafted special needs trust agreement allows the trustee to supplement government assistance with trust funds for quality-of-life expenses without jeopardizing eligibility.

Blended families benefit from trust agreements that balance competing interests. A QTIP trust lets you provide for your current spouse while ensuring your children from a previous marriage eventually inherit your assets. Without this structure, your spouse could disinherit your children after you die—a trust agreement makes your wishes legally enforceable.

Control over distribution timing makes trusts valuable for parents of young or financially immature children. Rather than giving an 18-year-old a $500,000 inheritance outright, your trust agreement can direct the trustee to pay for education and health needs immediately, distribute a third at age 25, another third at 30, and the balance at 35. This staged approach protects young beneficiaries from poor decisions while they develop financial maturity.

Business owners use trusts to ensure smooth succession. Your trust agreement can hold business interests, appoint a trustee with management experience to run the company temporarily, and provide for gradual transfer to children who work in the business while fairly compensating those who don't.

You might not need a trust agreement if your estate is simple and small. A single person with $200,000 in assets, no minor children, and one responsible adult heir might accomplish their goals with beneficiary designations and a simple will. But as assets grow, family situations become more complex, or special circumstances arise, trust agreements become increasingly valuable.

Trust Agreement vs Will vs Trust Certificate Comparison

| Feature | Trust Agreement | Will | Trust Certificate |

| Purpose | Creates and governs a trust; manages and distributes assets | Directs asset distribution after death; names guardians for minors | Proves trust exists and identifies trustee without revealing private terms |

| Privacy | Remains private; not filed with courts | Becomes public record during probate | Public document, but protects trust details |

| Probate Required | No (if trust is properly funded) | Yes, for assets in your individual name | N/A (not an estate planning document) |

| When It Takes Effect | Immediately upon signing and funding (for living trusts) | Only after death | When trust is created |

| Ease of Modification | Easy for revocable trusts; difficult or impossible for irrevocable trusts | Easy to change anytime before death | Cannot be modified (reflects current trust status) |

| Typical Use Cases | Probate avoidance, privacy, incapacity planning, controlled distributions | Simple estates, naming guardians, backup for unfunded assets | Proving trustee authority to banks, title companies, or other institutions |

Frequently Asked Questions About Trust Agreements

A trust agreement serves as the foundation of a comprehensive estate plan, creating a legal framework that protects your assets, provides for your loved ones, and ensures your wishes are carried out precisely as you intend. The document establishes a fiduciary relationship that survives your death or incapacity, allowing your trustee to manage and distribute property without court intervention, delays, or public exposure.

The value of a trust agreement extends beyond avoiding probate. It offers flexibility to address complex family situations, control over when and how beneficiaries receive inheritances, protection against creditors and irresponsible spending, and peace of mind that your affairs are in order. Whether you need a simple revocable living trust or a sophisticated irrevocable arrangement, the trust agreement makes your planning legally enforceable.

Creating an effective trust agreement requires careful thought about your assets, family dynamics, and long-term goals, combined with skilled legal drafting that anticipates problems and builds in solutions. The investment in professional guidance pays dividends through avoided probate costs, prevented family disputes, and the satisfaction of knowing your legacy is secure.

Remember that signing a trust agreement is only half the job—funding the trust by retitling assets into its name is what makes the plan work. An unfunded trust accomplishes nothing, no matter how brilliantly drafted. Work with your attorney to ensure every appropriate asset is properly transferred, review your trust periodically as circumstances change, and keep your documents safe and accessible to your successor trustee. With proper planning and execution, your trust agreement becomes one of the most valuable documents you'll ever create.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.