Legal trust documents in a folder on a wooden desk next to a pen and a small house model in a bright home office

Advantages of a Trust in Estate Planning

Content

Content

Most people think estate planning means writing a will and calling it done. Then their family discovers that will triggers a nine-month probate process, costs $8,000 in attorney fees, and becomes public record for anyone to read. Trusts solve these problems—and several others you probably haven't considered. They're not just for millionaires, either. If you own a house and want to spare your family unnecessary headaches, understanding trust benefits matters.

What Is a Trust and How Does It Work in Estate Planning

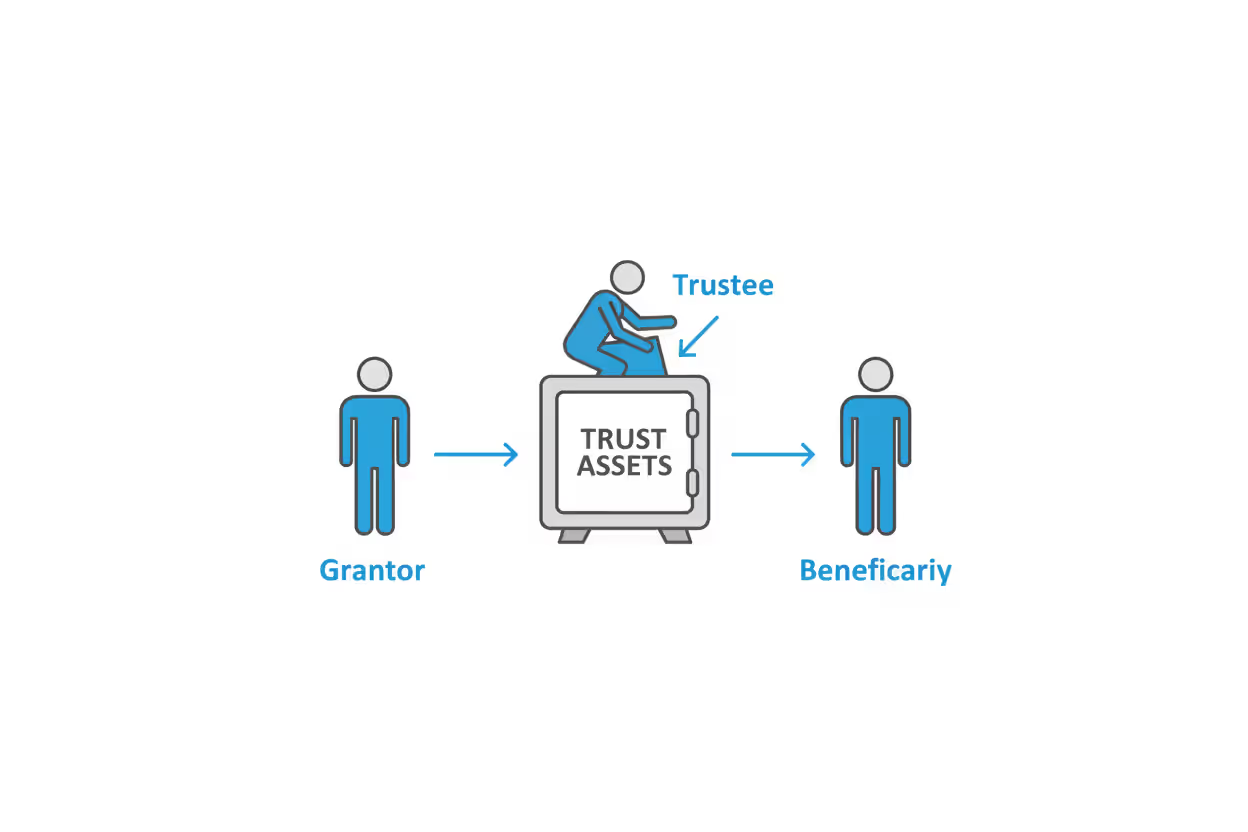

Think of trusts as customized financial containers. You (the grantor) place property into this container. Someone you select (the trustee) follows your written rules about managing what's inside. Specific people you name (beneficiaries) eventually receive the benefits.

What is the purpose of a trust in estate planning? It creates a management system for your wealth that operates both while you're alive and after you're gone—something wills can't do.

Every trust involves three roles. The grantor creates the arrangement and contributes property. The trustee handles day-to-day management and follows the instructions you've written down. Beneficiaries receive distributions according to the schedule and conditions you've established. Often, one person wears multiple hats—you might be grantor, trustee, and beneficiary simultaneously.

Author: Jonathan Whitmore;

Source: harbormall.net

Most families use revocable living trusts. Picture having complete flexibility: you're in charge, you can add your new rental property next month, remove cash if you need it, change beneficiaries after a family dispute, or tear up the whole thing if you change your mind. When you die or become incapacitated, the person you've designated as successor trustee steps in. No court approval needed.

Irrevocable trusts work differently. You give up control permanently. Can't change your mind next year. Can't take the assets back if you run short on cash. Sounds terrible, right? Here's the trade-off: this loss of control creates powerful asset protection and tax benefits that flexible trusts simply cannot deliver.

Your trust document works like a detailed instruction manual. It tells your trustee exactly who gets what, when distributions happen, what conditions beneficiaries must meet, and how to invest the money meanwhile. This level of detailed control distinguishes trusts from wills, which basically say "give my stuff to these people" without much nuance.

Privacy Protection and Probate Avoidance

Probate court proceedings become permanent public records. Last year, I searched my county's online probate database and found a neighbor's entire estate inventory—bank account balances, stock portfolios, even the appraised value of his mother's jewelry. His family's financial details were available to anyone with internet access.

One of the key benefits of trusts in estate planning is keeping your business private. Trust administration happens completely outside the court system. No public filings. No courthouse documents anyone can request. Only the people directly involved—your trustee, your beneficiaries, and their lawyers—see the details. Families dealing with estranged relatives, complicated relationships, or substantial wealth particularly value this confidentiality.

Beyond privacy, probate devours time and money. Most estates spend eight to eighteen months stuck in the process, assuming everything goes smoothly. Legal fees, executor compensation, court filing costs, property appraisals—all these expenses chip away at what beneficiaries ultimately receive. California's statutory fees illustrate the problem: a $500,000 estate pays $13,000 in basic fees before adding extra attorney charges for complications.

Assets titled in your living trust skip probate completely. When you die, your successor trustee immediately takes over. They access accounts that same week, keep paying the mortgage, and distribute property according to your instructions. No judge needs to approve anything. Your daughter might receive her inheritance three weeks after your funeral instead of thirteen months later.

Author: Jonathan Whitmore;

Source: harbormall.net

The multiple-property problem gets expensive fast. Own a winter place in Florida and a cabin in Colorado while living in Michigan? Without a trust, your estate goes through probate in all three states. Three sets of attorney fees. Three court processes running simultaneously. Transfer all these properties into your trust, and this multiplied complexity vanishes entirely.

These advantages of trusts in estate planning become extremely concrete when your widow needs grocery money. Probate freezes bank accounts until the court says otherwise. Bills pile up. Financial stress compounds grief. Your trust lets her continue accessing accounts without interruption—she's already the successor trustee, so nothing changes operationally.

Control Over Asset Distribution and Timing

Wills operate like sledgehammers: "Split everything equally between my three kids." Real life requires more precision.

Your 26-year-old nephew just received $300,000 from his grandmother's will. Six months later? Broke. The money disappeared on a Tesla, cryptocurrency day-trading losses, and a "business idea" his sketchy friend pitched. Why use a trust for estate planning? Because you can prevent exactly this scenario.

Staggered distribution schedules protect beneficiaries from themselves. Your instructions might say: distribute one-quarter at age 25, another quarter at 30, half the remainder at 35, and the rest at 40. Or tie releases to meaningful achievements—finishing college, maintaining steady employment for two years, or completing addiction treatment successfully.

This timing control shields inheritances from predators who specifically target people receiving sudden windfalls. Your trustee acts as gatekeeper, making sure the money actually benefits your beneficiary long-term instead of vanishing in weeks.

Incentive conditions add another layer. Match earned income dollar-for-dollar up to $50,000 annually—your beneficiary receives inheritance distributions equal to what they earn working. Or fund specific purposes only: graduate school tuition, down payments on primary residences, or startup capital for legitimate businesses. These conditions align inheritances with your values and encourage responsible behavior.

Beneficiaries with disabilities face a cruel dilemma. Direct inheritances above $2,000 disqualify them from Supplemental Security Income and Medicaid. They must spend down the inheritance before regaining crucial government assistance. Properly drafted special needs trusts solve this problem—the inheritance supplements government benefits without jeopardizing eligibility, paying for quality-of-life improvements that programs don't cover.

Spendthrift clauses protect inheritances from your beneficiaries' creditors. Your son can't borrow against future trust distributions or sell his inheritance interest to settle debts. When he faces a lawsuit, gets divorced, or owes money, the trust shields these assets from claims. Trust benefits for estate plans include keeping family wealth in the family despite external threats.

Discretionary trusts give your trustee judgment authority. Instead of automatic distributions, they evaluate each request considering the beneficiary's current circumstances, behavior, and needs. This flexibility helps when beneficiaries struggle with addiction, demonstrate financial recklessness, or face manipulation from problematic relationships.

Protection from Creditors and Legal Claims

Irrevocable trusts create legal separation between you and your assets. Once you transfer property into one, you no longer own it—the trust entity does. This distinction creates powerful advantages of trusts in estate planning that extend well beyond death planning.

Author: Jonathan Whitmore;

Source: harbormall.net

Doctors, lawyers, and architects face constant malpractice exposure. Business owners worry about liability claims. Irrevocable trusts established before problems arise place assets beyond creditors' reach. Properly structured and funded years before any claim surfaces, these trusts protect family wealth even when personal assets face judgment liens.

Timing is absolutely critical here. Courts void transfers made to dodge existing or imminent creditor claims under fraudulent conveyance laws. Depending on your state, judges examine transfers made two to four years back, searching for fraud indicators. Asset protection demands advance planning, not panic moves after receiving a lawsuit.

Medicaid planning shows another protection angle. Nursing facilities charge $8,000 to $12,000 monthly in many regions. Medicaid only pays after you've depleted assets to roughly $2,000. Irrevocable Medicaid trusts protect home equity and savings from this spend-down mandate, preserving wealth for spouses and children while securing government assistance. You'll need to plan five years ahead—Medicaid's look-back period examines all recent transfers.

Divorce protection helps children from prior marriages. Correctly structured trusts ensure assets meant for your kids don't become marital property when they divorce. The inheritance stays trust property, completely outside divorce court jurisdiction. This protection proves especially valuable in blended families where you want to provide for your biological children without accidentally enriching a future ex-spouse.

About twenty states permit domestic asset protection trusts (DAPTs). You establish an irrevocable trust, transfer assets into it, yet remain a potential beneficiary yourself. State statutes shield these assets from future creditors—with exceptions for existing debts, alimony, child support, and certain tort judgments. Nevada, Delaware, and South Dakota have particularly protective DAPT laws.

Offshore trusts provide even stronger protection but involve substantial complexity, significant cost, and detailed reporting requirements. Jurisdictions like Cook Islands and Nevis make creditors jump through extraordinary hoops to reach trust assets—often requiring them to refile their entire case under foreign law, with no contingency-fee attorneys available.

Tax Planning Advantages and Cost Savings

Federal estate tax exemption currently sits at $13.99 million per person in 2026, inflation-adjusted annually. Married couples effectively shield $27.98 million using portability rules. Most American families never touch federal estate taxes. But several states impose estate or inheritance taxes with far lower thresholds—Massachusetts starts taxing estates above $2 million, Oregon begins at $1 million.

For estates approaching or exceeding these limits, irrevocable life insurance trusts (ILITs) remove policy death benefits from taxable calculations. Life insurance proceeds normally count toward your taxable estate. An ILIT owns the policy instead, keeping proceeds outside estate tax calculations while providing cash to pay taxes, equalize inheritances among children, or fund business succession agreements.

Credit shelter trusts (sometimes called bypass or family trusts) help married couples use both exemptions fully. When the first spouse dies, assets up to the exemption amount fund a trust benefiting children or other heirs, while potentially allowing the surviving spouse to receive income. This approach "uses" the deceased spouse's exemption instead of wasting it, potentially saving millions in eventual taxes.

Generation-skipping transfer (GST) trusts benefit grandchildren while avoiding taxes on the middle generation. Transferring assets directly to grandchildren triggers the 40% GST tax above exemption limits. Dynasty trusts properly using GST exemptions create multi-generational wealth vehicles potentially lasting centuries in states without perpetuities restrictions.

Qualified personal residence trusts (QPRTs) freeze your home's value for tax purposes. You transfer your residence to an irrevocable trust while keeping the right to live there for a set period—say, ten years. The transfer's gift tax value gets discounted based on your retained living rights. Survive the term, and the home passes to beneficiaries at that original discounted value regardless of how much it's appreciated.

Charitable remainder trusts deliver income during your lifetime, with whatever remains going to charity afterward. You get immediate income tax deductions, avoid capital gains on appreciated assets you contribute, receive income for life or a specified term, and support causes you care about. Benefits of trusts in estate planning include this combination of tax efficiency and charitable giving.

Grantor retained annuity trusts (GRATs) move appreciating assets to beneficiaries while minimizing gift taxes. You receive fixed annuity payments for a term, with leftover assets passing to beneficiaries. If assets appreciate faster than the IRS's assumed rate (currently around 5.6%), that excess growth passes tax-free. Short-term GRATs funded with rapidly appreciating assets—stock options, startup equity—work particularly well.

Special Circumstances Where Trusts Provide Unique Benefits

Blended families create competing interests that wills handle badly. You want to support your current spouse financially but ensure children from your first marriage ultimately inherit family assets. A QTIP (qualified terminable interest property) trust accomplishes both objectives. Your spouse receives income throughout their life, with the principal passing to your children after your spouse dies. This arrangement prevents your spouse from disinheriting your kids or mixing your assets with theirs.

Minor children legally cannot own substantial property. Without planning, courts appoint property guardians to manage inheritances until kids reach 18 or 21—then the full amount transfers to a teenager with zero restrictions. How many parents think that's ideal? Trusts extend your control into beneficiaries' 20s, 30s, or longer, releasing funds as maturity develops rather than hitting arbitrary age triggers.

Author: Jonathan Whitmore;

Source: harbormall.net

Special needs planning demands technical precision. Direct inheritances disqualify disabled beneficiaries from means-tested benefits. First-party special needs trusts (funded with the beneficiary's own settlement or inheritance money) must include Medicaid payback clauses. Third-party special needs trusts (funded by parents or others) avoid payback requirements while preserving benefit eligibility. Trust benefits for estate plans include maintaining quality of life without sacrificing essential government support.

Business owners rely on trusts for succession planning. Voting and non-voting stock classes combined with trusts let you transfer business value while keeping control. GRATs move appreciating business interests to the next generation at reduced gift tax costs. Buy-sell agreements funded by insurance trusts provide cash for ownership transitions.

Pet trusts address animal care after you're gone. Until recently, these weren't legally enforceable in most states. Statutory pet trusts now let you set aside funds and name a trustee ensuring your animals receive proper care. You specify care standards, veterinary treatment parameters, and who gets remaining funds after your pet dies.

Gun trusts solve firearms transfer headaches. National Firearms Act weapons—suppressors, short-barreled rifles, machine guns—require extensive ATF approval for transfers, including inheritance. A gun trust allows multiple trustees to lawfully possess NFA items without individual transfers, simplifies compliance paperwork, and provides succession planning for valuable collections.

Real estate portfolios benefit from land trusts providing privacy (property records show the trust name rather than yours), facilitating estate planning, and potentially simplifying financing. Combined with LLCs for liability protection, these structures create robust asset management frameworks.

Most families obsess over who gets what and completely overlook the how and when.A trust transforms your estate plan from a simple asset list into a comprehensive protection and management system serving your family for generations

— Jennifer Martinez

Common Questions About Trust Benefits

The advantages of a trust in estate planning reach far beyond simply transferring assets to the next generation. Privacy protection keeps your family's financial affairs away from public scrutiny and opportunistic claims. Probate avoidance saves substantial time, money, and stress during periods already filled with grief. Control features ensure inheritances help rather than harm beneficiaries, with distributions timed to maturity and circumstances instead of arbitrary birthdays. Asset protection mechanisms guard family wealth from creditors, lawsuits, and poor judgment. Tax planning strategies preserve more for heirs and reduce government taxes.

Trusts don't solve every problem. Simple estates with minimal assets, no complications, and comfort with probate's public process might work fine with just a will. But the threshold for trust benefits sits much lower than most people assume. Homeownership, minor children, blended families, privacy concerns, or beneficiaries needing protection—any of these justify exploring trusts regardless of overall wealth.

Success lies in matching trust structures to your specific situation. Revocable living trusts handle most families' basic requirements. Irrevocable trusts address asset protection and tax planning for larger estates or particular risks. Special needs trusts protect vulnerable beneficiaries. Testamentary trusts created through wills offer some control benefits while accepting probate as a trade-off.

Starting a conversation with an experienced estate planning attorney costs nothing and provides clarity. Many offer free initial consultations to evaluate whether trust planning makes sense for your circumstances. The investment in proper planning—both time and money—pays dividends in family harmony, asset preservation, and peace of mind knowing you've protected what matters most.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.