Lawyer desk with legal trust documents, wax seal, fountain pen, and blurred bookshelves with law books in the background

Different Types of Trusts for Estate Planning

Content

Content

A will alone won't cut it when you're planning what happens to your assets. Many families discover—often too late—that trusts provide layers of protection and flexibility that basic wills can't match. The right trust setup can slash your family's tax bill by hundreds of thousands while keeping your affairs out of public court records.

What Is a Trust and How Does It Work in Estate Planning

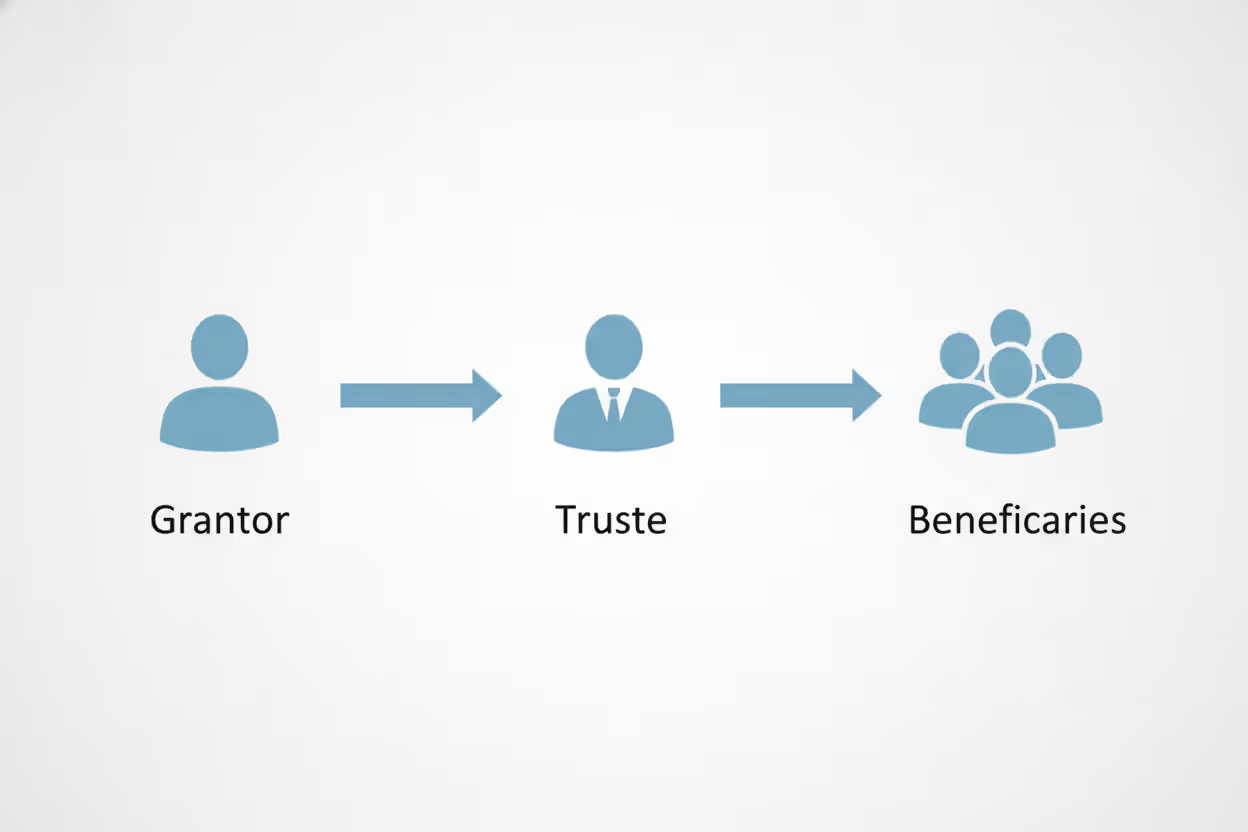

Here's how trusts work: you (the person setting things up, called the grantor) hand over control of certain assets to someone you trust (the trustee). That trustee then manages everything according to rules you've laid out, eventually passing benefits to the people or organizations you've named (your beneficiaries).

Picture a specialized financial container. You place real estate deeds, investment accounts, business ownership stakes, or bank balances inside it. The container comes with an instruction manual you've written, specifying exactly when and how the contents get distributed.

Three parties make the system function. You create it and write the rules. Your chosen trustee handles day-to-day management—everything from investment decisions to paying property taxes. The beneficiaries you've designated receive distributions based on your timeline and conditions.

Author: Michael Stratford;

Source: harbormall.net

Why bother? Trusts accomplish things wills simply cannot. They keep your financial affairs private rather than exposed in public probate filings. They can shelter assets from creditors hunting for deep pockets. They ensure someone you trust manages your money if you're incapacitated by illness or injury. For families with disabled members, trusts protect government benefit eligibility while still providing financial support.

The landscape of estate planning trust types stretches from basic structures activated after death to sophisticated multi-generational vehicles designed to compound family wealth across decades. Your income level, family complexity, and specific worries determine which approach makes sense.

Revocable vs Irrevocable Trusts

One characteristic separates all trusts into two camps: can you change your mind later? This single factor ripples through everything else—your tax situation, asset safety, and freedom to adjust course.

Revocable Living Trusts

With a revocable trust, you retain full control. Decide you want different beneficiaries next year? Change them. Want to swap out your trustee? Done. Need to pull assets back out? No problem. Most people name themselves as the first trustee, managing their own property exactly as they did before—just with better legal structure underneath.

Probate avoidance ranks as the biggest practical win. When you die, assets inside the trust transfer directly to beneficiaries without any court process. California and Florida residents understand this viscerally—probate in those states can devour 3-5% of everything you own, plus drag on for 12-18 months. A properly funded revocable trust sidesteps that entire nightmare.

The incapacity angle matters just as much. Stroke, dementia, serious accident—any of these can leave you unable to handle financial decisions. Your backup trustee steps into your shoes immediately, paying bills and managing investments without any court appointments or family squabbles. Compare that to the chaos of emergency conservatorship proceedings while you're hospitalized.

What's the catch? Revocable trusts don't reduce taxes or protect assets from lawsuits. The IRS sees right through them—since you control everything, you still own it for tax purposes. Creditors can still reach those assets. You're trading control and flexibility for convenience and privacy, not tax breaks or bulletproofing.

Author: Michael Stratford;

Source: harbormall.net

Irrevocable Trusts

Once you sign an irrevocable trust and fund it, you've generally burned the bridge. No take-backs, no modifications, no changing your mind. That permanence feels scary, but it creates genuine legal and financial separation.

Your taxable estate shrinks the moment assets move into an irrevocable trust. For 2026, federal estate tax kicks in above $13.99 million per person. Wealthy families moving assets into irrevocable structures can dodge millions in eventual estate taxes. The trust files its own tax returns and operates as a separate entity, creating opportunities for strategic tax planning impossible with personal ownership.

Lawsuit protection represents the other major benefit. When you genuinely no longer own assets—when they're locked in an irrevocable trust—plaintiffs and creditors can't touch them. Doctors, business owners, real estate investors, or anyone facing meaningful liability risk often shield wealth this way.

The revocable vs irrevocable trust estate planning decision boils down to your age and priorities. Younger families value flexibility—they choose revocable structures they can adjust as kids grow and circumstances shift. Older individuals with substantial assets or serious liability exposure lean irrevocable. Sophisticated plans often include both types working in tandem.

Common Trust Structures for Estates

Beyond the revocable-irrevocable split, specific trust designs solve particular problems. Knowing these common trust structures for estates helps you recognize tools that fit your situation.

Testamentary trusts spring into existence only after you die, created by instructions in your will. They don't help you avoid probate—your will still goes through court before the trust gets funded. But they cost less upfront and work well when you only need trust features posthumously. Parents of young children often use testamentary trusts to manage inheritances until kids reach 25 or 30, preventing teenagers from blowing college funds on sports cars.

Special needs trusts solve a heartbreaking problem: how do you leave money to a disabled child without destroying their Medicaid or SSI benefits? These trusts hold assets for disabled beneficiaries while preserving government assistance eligibility. The trust pays for things government programs won't—specialized therapy, recreation, education, quality-of-life improvements—while keeping those crucial health benefits intact. Families with disabled members can't afford to skip this planning.

Author: Michael Stratford;

Source: harbormall.net

Charitable trusts blend giving with tax strategy. A charitable remainder trust pays you (or other beneficiaries) income for a set period or your lifetime, then sends whatever's left to charities you've chosen. You get an immediate tax deduction, avoid capital gains on appreciated assets you contribute, and support causes that matter to you. Charitable lead trusts flip the order—charities get income first, then remaining assets pass to your heirs, often with dramatically reduced estate taxes.

Spendthrift trusts protect people from themselves and from predators. The trustee controls when and how much beneficiaries receive, preventing impulsive spending or pledging future distributions as loan collateral. Got a son with gambling problems? A daughter in a rocky marriage? Someone who just can't hold onto money? Spendthrift provisions prevent rapid wealth evaporation and keep creditors at bay.

Generation-skipping trusts leapfrog wealth past your kids directly to grandchildren or even great-grandchildren. This minimizes taxes across multiple generations—the estate would otherwise get taxed when you die, then taxed again when your kids die. With the 2026 generation-skipping exemption at $13.99 million per person, wealthy families can move substantial assets beyond multiple estate tax events.

Most well-designed plans combine several of these estate planning types of trusts. You might establish a revocable living trust for probate avoidance that splits into multiple trusts at your death—a special needs trust for one child, a spendthrift trust for another, and a standard inheritance trust for the responsible kid.

Trust Options Based on Your Estate Planning Goals

Different objectives require different tools. Matching trust options for estate plans to your specific goals requires clarity about what you're actually trying to accomplish.

To skip probate: Revocable living trusts remain the gold standard. Retitle your house, brokerage accounts, and business interests into the trust while you're alive. When you die, your successor trustee distributes everything per your instructions—no probate court, no delays, no public records. This becomes absolutely critical if you own property in multiple states, because otherwise your family faces separate probate proceedings in each state. That's expensive and maddening.

Author: Michael Stratford;

Source: harbormall.net

To cut taxes: High-net-worth individuals need irrevocable structures, period. An irrevocable life insurance trust (ILIT) keeps policy death benefits outside your taxable estate—that's millions in tax-free wealth transfer for business owners with large policies. Grantor retained annuity trusts (GRATs) move appreciating assets to heirs while using favorable IRS calculations to minimize gift taxes. Qualified personal residence trusts (QPRTs) transfer your home's future appreciation out of your estate while letting you keep living there for years. Each technique requires precise drafting and professional guidance.

To protect assets: Irrevocable trusts provide real protection, but only for assets you move into them before problems arise. You can't outrun existing creditors or pending lawsuits—courts see through those last-minute transfers. Certain states (Nevada, Delaware, South Dakota, Alaska) allow domestic asset protection trusts where you remain a beneficiary of your own irrevocable trust while maintaining some protection from future creditors. These remain somewhat controversial and aren't bulletproof, but they're better than nothing.

To manage inheritances for young beneficiaries: You can create testamentary trusts through your will or build sub-trusts into your revocable living trust. Either way, you control the distribution schedule. Instead of your 18-year-old inheriting $500,000 outright (and predictably blowing it), you might specify one-third at 25, half the remainder at 30, and the balance at 35. Meanwhile, the trustee can distribute money for college, medical needs, or a first home purchase.

To handle incapacity: Revocable living trusts with detailed successor trustee provisions beat powers of attorney hands-down. Banks and brokerage firms routinely refuse to honor powers of attorney, especially if they're more than a few years old. A properly funded trust gives your successor trustee immediate, unquestionable authority over trust assets. No arguments, no hassles, no gaps in bill-paying or investment management.

Effective estate plans rarely rely on a single trust type. A business owner might establish a revocable living trust for probate avoidance, an ILIT for estate tax planning, and a special needs trust for a disabled grandchild—three separate structures working as an integrated system.

How to Choose the Right Trust for Your Situation

Picking from the different types of trusts for estate planning means honestly evaluating several practical factors.

Estate size determines tax planning urgency. If your total estate sits comfortably below $13.99 million (or $27.98 million for married couples), federal estate taxes aren't your problem. Focus on probate avoidance, incapacity planning, and protecting beneficiaries from themselves. But once you cross those thresholds, sophisticated irrevocable planning becomes financially essential—the difference between keeping millions in the family versus sending it to Washington.

Family complexity drives trust design. First marriage, stable relationship, responsible adult kids with no special needs? You can probably use straightforward revocable structures. Blended families with children from previous marriages? You need careful balancing between supporting a surviving spouse and preserving assets for your biological kids. Members struggling with addiction, disability, or chronic financial chaos? Build in protective restrictions that prevent rapid asset depletion.

State law creates the playing field. Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin operate under community property rules that affect how trusts work and how they're taxed—different from the common law rules in other states. Some states hammer trusts with state income tax; others (Florida, Nevada, Texas, Washington) impose no income tax at all. Asset protection trust laws vary wildly by state. Where you live shapes what's possible and what's advisable.

Costs matter, especially ongoing ones. A simple revocable living trust for a married couple runs $2,000-$5,000 with minimal ongoing costs if you're your own trustee. Complex irrevocable structures can cost $5,000-$15,000 just to establish, then require annual tax returns and trustee fees forever. For assets above $10 million, those costs easily justify themselves. For smaller estates, maybe not.

Professional help becomes non-negotiable above certain complexity thresholds. Estate planning attorneys know state-specific rules and have seen what works and what blows up. CPAs understand tax implications that aren't obvious to laypeople. Financial advisors coordinate trusts with retirement plans and investment strategies. For estates above $5 million, or involving business interests, special needs beneficiaries, or serious asset protection concerns, professional fees aren't an expense—they're cheap insurance against expensive disasters.

The worst trust decisions I see come from people copying a friend's plan. Your brother-in-law's trust setup might be completely wrong for you—different assets, different family situation, different state, different goals. What saved him money could cost you a fortune. Every family needs tailored planning based on their specific circumstances and objectives, not cookie-cutter templates or hand-me-down strategies

— Margaret Chen

Mistakes to Avoid When Setting Up a Trust

Even brilliantly designed trusts fail when implementation falls apart. Watch for these common errors that sabotage otherwise solid plans.

Creating but never funding the trust tops every attorney's horror story list. You pay thousands for trust documents, sign everything, then never actually transfer assets into it. Real estate still shows your individual name on the deed. Bank accounts were never retitled. Investment accounts stayed in your personal name. When you die, all those "protected" assets go through probate anyway because technically they were never in the trust. The trust document becomes an expensive paperweight that accomplished exactly nothing.

Picking the wrong person as trustee creates years of misery. Your college buddy might seem "good with money," but does he have time to file trust tax returns, communicate with beneficiaries, and make quarterly distributions? Family members bring personal knowledge but often lack financial sophistication or have conflicts of interest. Professional trustees (trust companies, banks) charge 1-2% annually but provide real expertise and objectivity. The right answer depends on trust complexity and family dynamics—sometimes co-trustees work best, pairing family knowledge with professional competence.

Letting trust documents gather dust for a decade ignores reality. Estate tax laws have changed radically since 2010. Your daughter got divorced. Your son died. The nephew you named as backup trustee moved to Thailand. Tax provisions that made perfect sense in 2012 create problems under current law. Review everything every three to five years minimum, and always after major life changes—births, deaths, marriages, divorces, major wealth changes, or moves to different states.

Going the DIY route for complicated situations saves money upfront, costs a fortune later. Online forms and software can handle simple scenarios—young, healthy individual, modest assets, straightforward family. They fall apart with blended families, business ownership, special needs kids, or substantial wealth. They can't explain state-specific quirks or warn about tax traps. The legal fees you skip often come back to haunt you as litigation costs or tax penalties that dwarf what proper planning would have cost.

Ignoring ongoing trust administration kills irrevocable trusts. These need separate tax ID numbers (not your Social Security number). They must file their own tax returns every year. Trustees have legal duties—fiduciary obligations requiring meticulous records, regular beneficiary updates, prudent investment decisions, and proper asset protection. Screw this up and trustees face personal liability while beneficiaries face tax problems. It's not set-it-and-forget-it.

Forgetting to coordinate beneficiary designations undermines your entire plan. Retirement accounts and life insurance transfer via beneficiary forms, not through trusts or wills. Name your estate as beneficiary and you've forced those assets through probate despite your trust. Name individuals directly and you've bypassed protections you carefully built into the trust. Every beneficiary designation must align with your overall trust strategy.

Frequently Asked Questions About Estate Planning Trusts

Trusts work when properly chosen, carefully drafted, and correctly funded. The range of available structures means virtually every family can find solutions matching their needs—whether that's straightforward probate avoidance or intricate tax planning spanning multiple generations.

Start by getting clear on what you're trying to fix. Probate expenses and delays eating into your estate? Estate taxes threatening to consume 40% of everything you've built? Protecting assets from lawsuits? Supporting a disabled family member? Your specific problems determine which trust structures make sense.

Then assess your actual situation honestly. How much are you worth? What's your family like—simple or complicated? Which state do you live in? A trust that's perfect for one family might be completely wrong for another facing different circumstances.

After that, hire qualified professionals. Estate planning attorneys, tax advisors, and financial planners bring expertise that prevents expensive mistakes. Money spent on professional guidance is an investment protecting your family's financial future, not an expense to minimize.

Finally, follow through completely. Fund your trust properly by actually retitling assets. Choose trustees thoughtfully, not impulsively. Review your plan regularly—at least every few years and always after major life changes. Estate planning isn't something you do once and forget about. It's an ongoing process adapting as your life and the law evolve.

The right trust structure, implemented correctly, delivers peace of mind. Your assets get managed and distributed according to your wishes, protected from unnecessary costs and delays, and preserved for the people and causes mattering most to you.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.