Multigenerational family sitting together at a table with estate planning documents in a bright modern home

How to Use a Family Trust for Estate Planning

Content

Content

Setting up a family trust without understanding its mechanics is like buying insurance without reading the policy—you might think you're protected, but surprises await. Many people sign trust documents their attorney prepared, nod along during explanations, then leave those documents in a drawer without taking the crucial steps that make them work.

The real value of family trusts and estate planning emerges when you match the right trust structure to your specific situation. Some families need simple probate avoidance. Others want to shield assets from future creditors, minimize estate taxes, or control how young beneficiaries receive their inheritance. Still others are planning wealth transfers spanning three or four generations. Each scenario demands different tools and strategies.

This guide walks through the practical aspects of using trusts in your estate plan—from understanding basic structures to implementing sophisticated multigenerational strategies. You'll learn not just what trusts can do, but when they make sense and how to avoid the costly mistakes that undermine even well-intentioned planning.

What Is a Family Trust in Estate Planning

When you establish a family trust, you're creating a separate legal entity that can own property. The person creating this entity (grantor or settlor) transfers assets to someone designated to manage them (trustee), who holds those assets for people specified to benefit from them (beneficiaries). In typical family scenarios, you serve in all three roles initially—creating the trust, managing it yourself, and benefiting from its assets during your lifetime.

Trusts split into two fundamental types based on whether you retain modification rights. With revocable structures (commonly called living trusts), you keep complete authority to alter terms, withdraw assets, or eliminate the entire arrangement while you're living and mentally capable. This flexibility comes with a trade-off: because you maintain control, these assets remain part of your taxable estate. Irrevocable structures work differently—you're making a permanent transfer that removes assets from your estate. Once you've signed an irrevocable trust, changing its terms typically requires beneficiary agreement or court intervention, though this rigidity delivers superior asset protection and tax advantages.

Wills and trusts serve different functions in estate planning. Your will expresses wishes that take effect only after death, and those wishes must be validated through probate—a public court process where anyone can review filings showing your assets, debts, and family disputes. Properly funded trusts skip this entirely, allowing immediate transfers according to instructions you've left. While drafting a will requires just one document and minimal ongoing work, a family trust estate plan demands continuous attention to how assets are titled.

Living trusts dominate family planning because you create them now, transfer your property into them, and typically manage them yourself. When you die or can no longer handle your affairs, the person you've designated as successor trustee steps in immediately—no court approval needed. Testamentary trusts take a different path: they're established through provisions in your will and only spring into existence after your death. They can't avoid probate since they're part of the will itself, but they serve useful purposes for managing inheritances left to minors or beneficiaries requiring long-term structured distributions.

Why Families Choose Trusts for Estate Planning

Avoiding probate court drives most families to explore trusts initially. Probate can consume 3% to 7% of everything you own, and the timeline stretches from six months to over two years depending on estate complexity and state procedures. Every detail becomes public record—your assets, their values, who receives them, and any arguments among heirs. Courts publish this information, searchable by anyone with internet access.

Keeping financial matters private extends beyond general discomfort with public disclosure. Business owners don't want competitors knowing company valuations. Wealthy families prefer not advertising their holdings to potential scammers or frivolous lawsuit filers. When real estate ownership changes through probate, it's permanently recorded in public documents that generate solicitation letters to heirs for months afterward. Estate planning with a family trust keeps these transfers between you, your trustee, and your beneficiaries.

Controlling how and when beneficiaries receive money represents trusts' greatest advantage over simple inheritance. Perhaps your son just graduated college and isn't ready to manage a large sum responsibly—you can specify he receives one-third at 25, another third at 30, and the remainder at 35. Your daughter with special needs might require lifetime support, but receiving assets directly could disqualify her from Medicaid or SSI benefits. Trust provisions allow you to set conditions: matching educational expenses, funding home purchases, or even incentive clauses that multiply distributions based on earned income from employment.

Author: Caroline Ellsworth;

Source: harbormall.net

Shielding assets from creditors depends heavily on trust structure and timing. Revocable living trusts provide essentially zero protection from your creditors while you're alive—you control the assets, so courts can reach them. Irrevocable trusts deliver genuine protection by permanently transferring ownership beyond your control, making those assets unavailable to future creditors, lawsuits, or divorce settlements (assuming you established the trust before any legal problems emerged). Beneficiaries gain protection too: carefully drafted spendthrift clauses prevent their creditors and divorcing spouses from seizing inherited assets held in trust.

Tax advantages vary based on estate size and chosen structure. The 2026 federal estate tax exemption sits around $13.99 million per person, placing most families below the threshold. However, twelve states and the District of Columbia impose state-level estate or inheritance taxes with far lower exemptions—Massachusetts starts at $2 million, Oregon at $1 million. Irrevocable trusts permanently remove assets from your taxable estate, and specialized structures can leverage generation-skipping transfer tax exemptions for wealthy families building multi-generational wealth.

How to Set Up a Family Trust Estate Plan

Deciding whether trusts fit your circumstances requires examining your asset profile, family relationships, and long-term objectives. Real estate in multiple states makes trusts almost essential—without one, heirs face separate probate proceedings in each state where you owned property. Families with young children, blended marriages, or members with disabilities almost universally benefit from trust planning for families. Conversely, if your estate totals under $200,000, your family relationships are straightforward with no special needs, and your state offers simplified probate procedures, a simple will might adequately serve your needs.

Selecting revocable versus irrevocable structures involves weighing flexibility against protection. Revocable arrangements let you adapt to changing circumstances—adding new beneficiaries after grandchildren are born, adjusting distribution percentages, or canceling everything if your situation changes dramatically. You'll report trust income on your personal tax return as if you owned everything directly, and creditors can still reach these assets. Irrevocable structures lock in decisions that become nearly impossible to reverse, but deliver genuine asset protection and remove property from your taxable estate. Most families begin with revocable trusts for their flexibility, sometimes later converting them or creating separate irrevocable trusts for specific purposes like life insurance or Medicaid eligibility planning.

Naming trustees and beneficiaries demands careful attention to both capability and family politics. You'll likely serve as trustee of your revocable trust during your lifetime, maintaining complete authority. The crucial choice involves your successor trustee—who takes charge when you die or become incapacitated. Adult children seem like natural choices, but appointing one sibling to control distributions to others can breed resentment. Professional trustees (banks or trust companies) charge ongoing fees of 0.5% to 1.5% of assets annually but bring impartiality and financial expertise. Co-trustee arrangements pairing a family member with a professional can balance personal knowledge against institutional experience.

Transferring assets into the trust represents where most family trust estate plans succeed or fail. The trust document itself creates the entity, but that entity owns nothing until you change how your assets are titled. Real estate requires recording new deeds showing the trust as owner. Financial institutions need documentation transferring bank accounts and investment holdings into trust ownership. Business interests transfer through formal assignment documents. Personal property like vehicles and valuable collections should transfer via bills of sale. Life insurance and retirement accounts follow special rules—usually you shouldn't make the trust the owner, though naming it as beneficiary works in specific circumstances. A trust holding no assets accomplishes nothing—everything titled in your personal name will enter probate regardless of your trust document.

Author: Caroline Ellsworth;

Source: harbormall.net

Engaging an estate planning attorney proves worthwhile except in the simplest situations. Online template services offer basic trusts for a few hundred dollars, but they can't account for your state's unique requirements, your particular family complications, or potential tax consequences. Qualified attorneys coordinate your trust with complementary planning documents, supervise proper asset funding, and help you sidestep expensive mistakes. Budget $1,500 to $3,500 for straightforward revocable trust packages covering simple assets, or $3,000 to $10,000+ for sophisticated planning involving irrevocable structures, business succession planning, or multi-generational wealth transfer strategies.

Documents Needed to Establish a Trust

Your trust agreement forms the foundation—this document formally creates the trust, identifies the trustee and beneficiaries, and spells out distribution instructions. Expect 20 to 50 pages depending on how complex your situation is and how detailed your instructions are.

A pour-over will works alongside your trust as a safety net, capturing any assets still in your individual name at death and directing them into the trust. These assets must go through probate, but they ultimately distribute according to trust terms rather than state intestacy laws.

Durable financial powers of attorney authorize someone to handle matters outside the trust if you become incapacitated. Even comprehensive trusts don't capture everything—income streams or accounts might remain in your personal name.

Healthcare directives and medical powers of attorney address treatment decisions and aren't technically part of the trust structure, but they complete a comprehensive estate plan.

Property transfers require new deeds for real estate holdings. Financial institutions typically insist on their proprietary forms rather than accepting your complete trust document. Your attorney should prepare a certificate of trust—an abbreviated document proving the trust exists and identifying the trustee without revealing private distribution details.

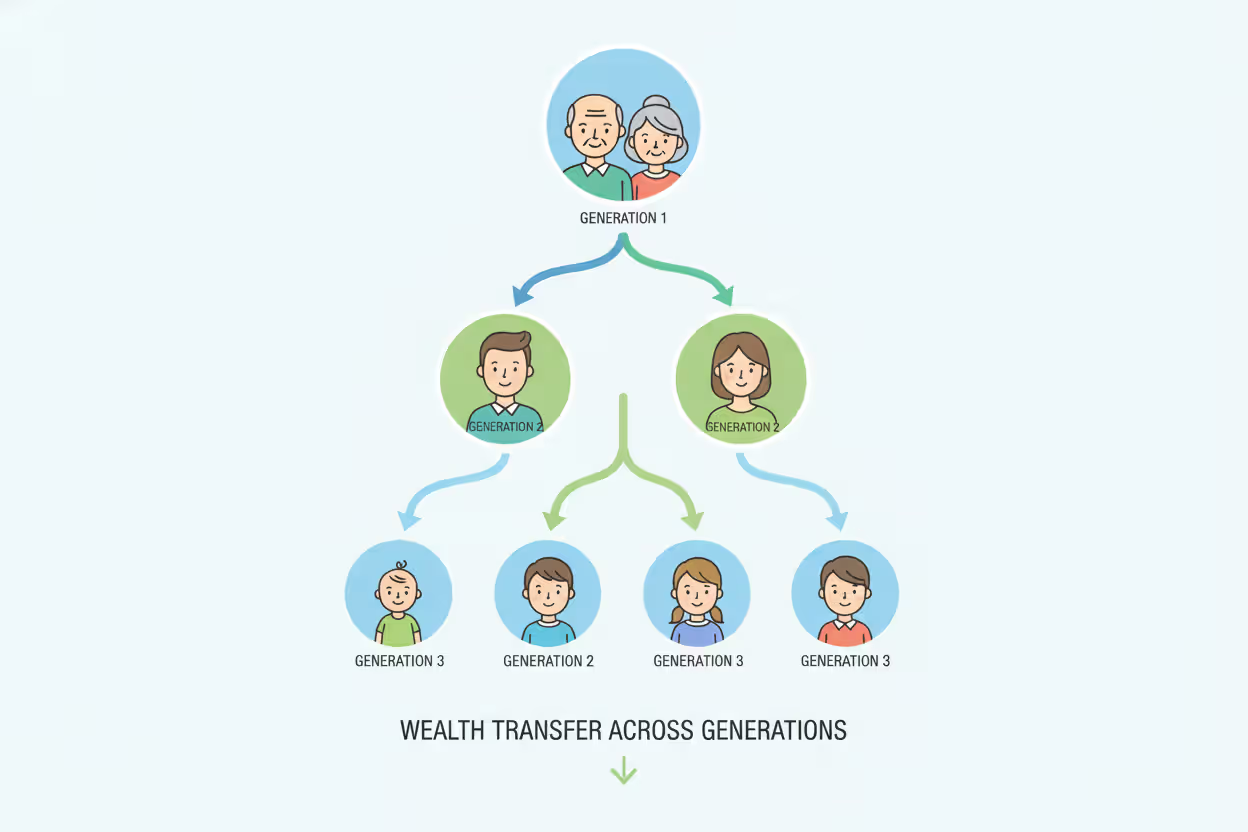

Multigenerational Trust Planning Strategies

Dynasty trusts represent advanced planning for families focused on building lasting legacies. These irrevocable structures are designed to persist across generations—potentially forever in states that eliminated perpetuity restrictions. Assets deposited into dynasty trusts can appreciate and support children, grandchildren, great-grandchildren and beyond while remaining insulated from estate taxes, divorces, and creditors at each generation level. The cost is complexity and permanent loss of access—once you fund these trusts, you cannot reclaim assets regardless of changed circumstances.

Generation-skipping transfer tax considerations arise when you want assets flowing directly to grandchildren or more distant descendants. Federal law imposes a 40% GST tax on wealth transfers bypassing a generation, but you receive a GST exemption matching your estate tax exemption (approximately $13.99 million individually in 2026). Strategically designed trusts can leverage this exemption to move substantial wealth down multiple generations without triggering additional estate or GST taxes. This area demands sophisticated planning—misapplying the exemption creates unexpected tax obligations that can devastate your intended legacy.

Author: Caroline Ellsworth;

Source: harbormall.net

Protecting inheritances for grandchildren and future generations often incorporates incentive language and age-based distribution schedules. Rather than handing a 21-year-old grandchild millions immediately, you might structure releases tied to education completion, first home purchase, or business formation, with complete access delayed until age 35 or 40. Some families write matching formulas encouraging entrepreneurship—the trust contributes dollar-for-dollar with the beneficiary's earned income up to specified limits. Others authorize trustees to provide for "health, education, maintenance, and support" while granting discretion to withhold funds from beneficiaries struggling with substance abuse or making repeatedly poor financial choices.

Reviewing and updating trusts as circumstances evolve proves essential for multigenerational family trust planning. New births, unexpected deaths, marriages ending in divorce, and changes in beneficiary life situations all warrant trust examination. If your daughter's marriage fails, you'll want to restructure her inheritance to keep it from her ex-spouse. When a grandchild develops disabilities, you'll need distributions structured to preserve government benefit eligibility. Tax legislation shifts periodically too—estate tax exemptions rise and fall with political changes, and state laws evolve constantly. Schedule trust reviews every three to five years minimum, or immediately after major family events.

Common Mistakes in Trust Planning for Families

Neglecting to transfer assets into the trust represents the most frequent and damaging error. Families invest thousands in comprehensive trust creation, then never change how their home, accounts, or investments are titled. Years pass, and when death occurs, families discover the trust holds nothing—everything enters probate exactly as if no planning had occurred. Create calendar reminders for annual trust funding reviews, and establish procedures with your attorney ensuring new assets get titled properly as you acquire them.

Overlooking beneficiary designation updates creates conflicts between your trust terms and actual asset distribution. Your trust might divide everything equally among three children, but if your IRA beneficiary form still names only your oldest child (perhaps designated before the younger two were born), that retirement account bypasses the trust entirely. Retirement accounts, life insurance policies, and transfer-on-death accounts all skip trust provisions unless the trust itself is named beneficiary. Audit all beneficiary designations whenever you modify your trust.

Selecting an inappropriate trustee can sabotage even brilliantly designed trusts. Your financially responsible daughter appears perfect until you consider she lives across the country, works demanding hours while raising young children, and struggles saying no when siblings ask for early distributions. Naming all your children as co-trustees hoping to avoid hurt feelings often produces gridlock when they disagree on decisions. Consider whether professional trustees or trust protectors (individuals authorized to remove and replace trustees) might better serve your family long-term.

Author: Caroline Ellsworth;

Source: harbormall.net

Disregarding tax consequences produces expensive surprises. Transferring your primary residence into an irrevocable trust might seem like smart asset protection, but you could forfeit the capital gains tax exclusion on future sales. Moving highly appreciated assets into certain irrevocable trusts can trigger immediate capital gains taxes. Life insurance trusts require navigating the three-year rule—dying within three years of transferring a policy pulls it back into your taxable estate. Engage both estate planning attorneys and tax professionals to model consequences before implementing complex strategies.

Using do-it-yourself trust templates without professional review saves pennies while risking pounds. Online forms can't account for your state's specific legal requirements, which vary dramatically across jurisdictions. Standard language typically fails addressing unique family situations—special needs children, family business ownership, or properties in multiple states. The few hundred dollars saved on templates can cost your family tens of thousands resolving problems that emerge later when problems surface.

Costs and Timeline for Creating a Family Trust

The most damaging error I encounter involves families who create trusts but never properly transfer assets into them. I call these 'empty boxes'—elegant legal structures accomplishing nothing because properties remain titled in personal names. The second most common problem is appointing trustees based on avoiding hurt feelings rather than genuine suitability for the role. Your estate plan isn't the appropriate place for making everyone feel included regardless of capability

— Margaret Chen

Legal fees fluctuate based on complexity, geography, and attorney experience levels. Basic revocable living trusts for single individuals with straightforward assets typically cost $1,500 to $2,500. Married couples generally pay $2,000 to $3,500 for coordinated joint trusts with complementary estate documents. Complex circumstances involving business ownership, multiple properties, or irrevocable structures can range from $5,000 to $15,000 or higher. Major metropolitan areas and high-cost states see elevated fees. Some attorneys quote flat fees for standardized trust packages while others bill hourly at $250 to $600 depending on experience and location.

Administrative expenses after creation depend on whether you manage your own trust or hire professionals. While you're living and serving as your own trustee of a revocable trust, ongoing costs stay minimal—perhaps a few hundred dollars periodically for legal updates. When successor trustees take over, professional management typically costs 0.5% to 1.5% of trust assets annually. A $1 million trust generates $5,000 to $15,000 in annual trustee fees. Family members serving as trustees often waive fees or charge reduced amounts, though they may need to engage attorneys or CPAs for tax filings and complicated decisions, costing $1,000 to $5,000 yearly.

Establishment timelines from initial consultation through complete funding usually span four to eight weeks for uncomplicated situations. Your first attorney meeting covers assets, family dynamics, and planning goals. Draft documents take one to three weeks to prepare. You'll review drafts, request revisions, and schedule a signing appointment. Following signing, several weeks of asset transfer work begins—recording property deeds, retitling financial accounts, updating beneficiary forms. Complex trusts involving business valuations, sophisticated tax planning, or numerous properties can require three to six months for proper implementation.

Ongoing maintenance responsibilities include verifying trust funding remains current as you acquire new assets, confirming beneficiary designations stay aligned with trust terms, and evaluating whether the trust still reflects your wishes. Plan formal attorney reviews every three to five years, or sooner after major life changes like births, deaths, divorces, or significant asset value shifts. Some families schedule annual estate planning team check-ins to stay current with tax law changes and ensure optimal plan structure.

Comparison: Revocable vs Irrevocable Family Trusts

| Feature | Revocable Trust | Irrevocable Trust |

| Authority During Your Lifetime | Complete authority; modify or cancel anytime | Minimal or no authority; amendments require court approval |

| Bypassing Probate | Yes, when properly funded | Yes, when properly funded |

| Protection from Creditors | No shielding from your creditors | Strong shielding from creditors and legal judgments |

| Estate Tax Advantages | No reduction in taxable estate; assets remain yours for tax purposes | Removes assets from your taxable estate; potential significant tax savings |

| Ability to Make Changes | Total flexibility changing terms or beneficiaries | Extremely limited; often requires beneficiary agreement or court order |

| Qualifying for Medicaid | Assets counted toward eligibility thresholds | Assets may be excluded if trust created 5+ years before applying |

Frequently Asked Questions

Establishing a family trust demands real commitment to protecting assets and providing for future generations, but the process need not overwhelm you. Begin by inventorying your assets, thinking honestly about family relationships and potential conflicts, and clarifying your wealth transfer objectives. Schedule consultations with two or three estate planning attorneys to identify someone whose philosophy and communication approach match your preferences.

Recognize that trusts aren't one-time projects you can complete and forget. Life brings constant change—children are born, family members die, you acquire or sell assets, tax laws shift with political cycles. Families gaining maximum benefit from trust planning for families treat their estate plans as evolving documents, examining them every few years and updating when circumstances change significantly.

The expense and complexity of creating a family trust estate plan might seem daunting initially, but consider alternatives: your family navigating probate courts, enduring public examination of your finances, potentially facing estate taxes that proper planning would have avoided, or watching inheritances vanish to creditors or divorces. Time and money invested now in careful planning can save your heirs substantial expense, emotional stress, and family conflicts when they're mourning your death.

Whether you need straightforward revocable trusts for probate avoidance or sophisticated multigenerational planning preserving wealth for decades, success begins with that first step. Your legacy extends beyond assets you leave—it encompasses the clarity, protection, and peace of mind you provide people you love most.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to estate planning, wills, trusts, tax strategies, and financial legacy planning.

All information on this website, including articles, guides, worksheets, and planning examples, is presented for general educational purposes. Estate planning situations may vary depending on personal circumstances, financial structures, legal regulations, and jurisdiction.

This website does not provide legal, financial, or tax advice, and the information presented should not be used as a substitute for consultation with qualified legal, tax, or financial professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.